California New Car Registrations: July 2025 September 9, 2025

Seasonally adjusted new car registrations grew 1.5 percent in June and 1 percent in July but remain 8 percent lower than three months prior. This moderate growth stands in contrast to the substantial volatility we had observed in the prior six months. Sales remained slightly lower than the average level over the last couple of years.

Firearms and Ammunition Revenue Update (2025 Q2) August 18, 2025

Beginning July 2024, Chapter 231 of 2023 (AB 28, Gabriel) imposed an 11 percent excise tax on retail sales of firearms, firearm precursor parts, and ammunition, with some exemptions. For firearm and ammunition excise tax returns filed for 2024-25, the total amount of tax due is $58 million—a bit lower than the budget package revenue assumption.

California New Car Registrations: June 2025 July 29, 2025

Seasonally adjusted new car registrations grew 1.5 percent from May to June. This moderate growth stands in contrast to the substantial volatility we had observed in the prior six months. Due to the sharp decline in May, however, sales remained somewhat lower than the average level over the last couple of years.

California New Car Registrations: May 2025 July 9, 2025

Seasonally adjusted new car registrations dropped 10 percent from April to May. As result, May’s monthly total was the lowest since June 2024.

Early Data Revision Shows No Job Creation During 2024 Q4 June 24, 2025

Since mid-2022, the state's monthly jobs survey has tended to overestimate actual employment growth. The newest incoming data (from the fourth quarter of 2024) show the monthly survey again overstating employment. Specifically, the most recent match to administrative records shows the survey overestimated job creation from last September through December by roughly 100,000 jobs (preliminary survey gain of 102,000 relative to net loss of 1,000 jobs).

California New Car Registrations: April 2025 June 10, 2025

Seasonally adjusted new car registrations grew 5 percent from February to March, then another 4 percent from March to April. With this strong growth, registrations reached their highest level in nearly three years. Although tariffs on imported vehicles went into effect in early April, seasonally adjusted new vehicle prices did not rise substantially.

Cannabis Tax Revenue Update (2025 Q1) June 3, 2025

For cannabis excise tax returns filed for the first quarter of 2025, the total amount of tax due is $141 million. With this latest data, we currently project cannabis tax revenues of $594 million in 2024-25 and $732 million in 2025-26. Both of these estimates are within $5 million of the administration's May Revision forecast.

Firearms and Ammunition Revenue Update (2025 Q1) May 21, 2025

Beginning July 2024, Chapter 231 of 2023 (AB 28, Gabriel) imposed an 11 percent excise tax on retail sales of firearms, firearm precursor parts, and ammunition, with some exemptions. For firearm and ammunition excise tax returns filed for the first three quarters of 2024-25, the total amount of tax due is $44 million. Based on this data, the administration's estimate of $65 million for 2024-25 appears reasonable.

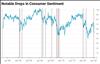

Assessing The Recent Drop in Consumer Sentiment May 9, 2025

Real-time economic indicators such as consumer sentiment have declined rapidly in early 2025. A similar decline in consumer sentiment has occurred only nine other times since 1983. These declines usually precede a period of below average growth but also sometimes precede periods of growth that exceed historical averages. Given that concrete measures of economic activity that reflect the current moment will not be available for a few months, we urge policymakers to weigh the risk of both a further downturn and of better than expected growth when making budget decisions.

Five Guidelines for Using Revenue Forecasts May 9, 2025

As part of building the state budget each year, the Legislature and Governor must make an assumption about how much revenue the state will collect. Because no one knows how much revenue the state will collect next year, leaders must rely on revenue forecasts. Both our office and the Department of Finance (DOF) provide periodic revenue forecasts that can be used for this purpose. These forecasts use the best available data to provide informed estimates of future revenue collections. Although they have limitations, they are important to the state budget process because they offer an objective foundation on which the budget can be built. In this post, we offer guidelines to help make the best use of these revenue forecasts—that is, to help them focus on the right questions, avoid overreactions, and be better positioned for the unexpected.

California New Car Registrations: March 2025 May 9, 2025

Seasonally adjusted new car registrations grew 5 percent from February to March. With this strong growth, March was the fourth highest monthly count of registrations in the last two years. As we track data for the next few months, we will see if this growth continues or if it was a transitory bump in anticipation of tariffs.

California New Car Registrations: February 2025 April 8, 2025

Starting with this post, we plan to publish monthly updates on new car registrations in California, which can be a useful, timely economic indicator. From December 2024 to February 2025, seasonally adjusted new car registrations declined by 8 percent. December registrations, however, had been the highest since mid-2022. As a result, February registrations still were around the average level over the last couple of years.

Annual Revision to Monthly Jobs Survey Shows Far Fewer Job Gains in 2024 March 21, 2025

Each year, the U.S. Bureau of Labor Statistics revises the state's jobs numbers to match actual payroll records from businesses. The latest revisions updates the survey data through September 2024 and lowered California job gains from 260k to 60k over the year. The corrected data show the state's labor market grew just 0.3 percent between September 2023 and September 2024, while the preliminary monthly reports had showed the labor market roughly in line with the rest of the country (about 1.5 percent) over that period.

Cannabis Tax Revenue Update (2024 Q4) March 6, 2025

Our new cannabis tax revenue estimates are very similar to the revenues anticipated by the Governor's Budget.

Firearms and Ammunition Revenue Update February 21, 2025

In the first half of 2024-25, preliminary revenue for the firearms and ammunition excise tax was $29 million.