This post discusses the near-term state General Fund revenue outlooks of both the administration and our office.

Administration and LAO Outlooks: Similar Through 2016-17

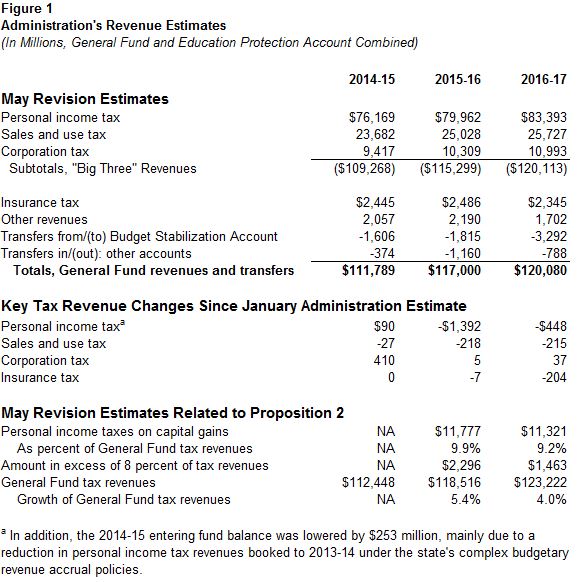

Figure 1 summarizes the administration’s May Revision revenue estimates through 2016-17. As discussed below, these estimates reflect the administration’s lowering of its near-term revenue estimates since the initial Governor’s budget proposal in January.

Administration Lowers Revenue Estimates. In January, the administration increased its 2015-16 and 2016-17 General Fund revenue estimates. (The administration’s revised January estimates were similar to those we released in November 2015.) The stock market tumbled in January, and tax revenue collections through April 2016 reflected a slightly slower rate of year-over-year growth than previously anticipated. Partly as a result of these developments, the administration lowered its revenue estimates in the May Revision by a net amount of $2.2 billion across four fiscal years: 2013-14, 2014-15, 2015-16, and 2016-17. (The $2.2 billion figure considers changes since January in the administration’s revenue projections only, excluding changes in transfer estimates sometimes lumped in with revenues, such as estimates of transfers to the state’s rainy day fund.) The primary changes to the administration’s estimates were a reduction in personal income tax (PIT) estimates of $1.8 billion in 2015-16 and 2016-17 combined.

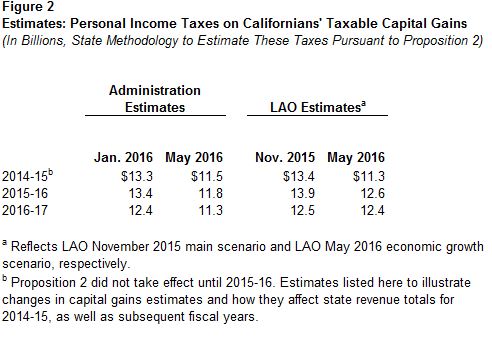

Lower Capital Gains Estimates. A key reason for the lower revenue estimates is that the administration lowered its estimates of personal income taxes on Californians’ taxable capital gains. The first solid data from tax agencies on 2014 returns—received a few weeks ago—showed that taxable capital gains in that year were substantially less than either we or the administration thought previously. The administration also reduced its estimates of taxable capital gains for 2015 through 2017. As shown in Figure 2, these changes helped lower the administration's overall revenue estimates, given that its estimates of taxes on capital gains (developed for use in Proposition 2 rainy day fund estimates) have fallen by $1.8 billion for 2014-15, $1.6 billion for 2015-16, and $1.1 billion for 2016-17. In the May Revision summary, the administration notes that “the decreases in capital gains and changes in income concentration [which causes a reduction in effective tax rates] were offset by higher levels of business income and a stronger wage growth forecast.” As shown in Figure 2, our office’s estimates of taxes on capital gains also have fallen over the last few months, but (under our office’s May 2016 economic growth scenario) they have not fallen nearly as much as the administration’s estimates for the 2016-17 fiscal year.

Nevertheless, Tax Revenues Still Growing. While the administration lowered its tax revenue estimates since January, the state’s overall General Fund tax revenues (administration estimates for which are listed in Figure 1) still are estimated to grow each year during the state “budget window”: up 5.4 percent in 2015-16 and another 4.0 percent in 2016-17. (Sales taxes grow at a slower rate in 2016-17 as Proposition 30 tax increases start to expire.)

The administration’s revenue estimates reflect the effects of the managed care organization (MCO) tax package passed earlier this year, which lowers insurance and corporation tax payments for some taxpayers by $300 million in 2016-17 (and higher amounts in the two fiscal years thereafter).

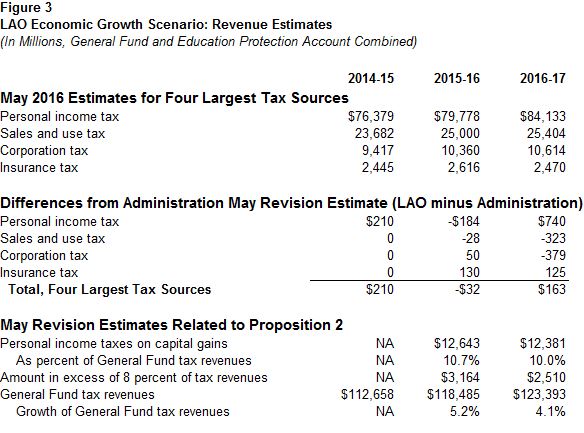

LAO Economic Growth Scenario: Revenues Similar to Administration Through 2016-17. As described in earlier posts, we base our May Revision budget estimates on a scenario that assumes continuing economic growth over the next several years. (This is not a prediction that such growth will occur during the entire period, as we discuss here.) Based on the assumptions in the LAO May 2016 economic growth scenario, we estimate the following:

- 2014-15. For 2014-15, we estimate that the combined revenues of the General Fund’s four largest tax sources (PIT, sales taxes, corporation taxes, and insurance taxes) are $210 million more than the administration currently estimates for 2014-15. The difference results from our higher estimates for Proposition 30 revenues, which are booked (accrued) to fiscal years in a very complex way.

- 2015-16. Under our economic scenario, we assume the four largest tax revenues will be a combined $32 million less than the administration now projects for 2015-16.

- 2016-17. For 2016-17, under our economic scenario, we estimate that these four taxes would total $163 million more than the administration now projects.

These differences, summarized in Figure 3, are minor, given the size of the state’s $120 billion General Fund budget.

Overall, for PIT, our office’s estimates of California taxable income appear to be quite similar to the administration’s—with a less than 1 percent difference in 2015, 2016, and 2017—despite our office’s higher estimates of taxable capital gains income. Thereafter, in our respective multiyear revenue scenarios, our office’s taxable income estimates are 2 percent to 3 percent above the administration’s annually through 2020, resulting in our tax revenue numbers being $2 billion to $4 billion higher than the administration’s estimates annually in 2017-18, 2018-19, and 2019-20. (For more information on those future years' revenue figures, see here.)

Corporate Tax Refund Uncertainties. In November and again in January, we discussed this fiscal year’s elevated level of corporation tax refunds. While corporation tax estimates have changed somewhat since January, both our office and the administration continue to assume that there will be an elevated level of refunds in May and/or June 2016. Based on guidance from tax agency staff, we believe this is a reasonable assumption, but neither the timing nor the amount of the refunds reflected in our estimates is certain. If the assumed level of corporate tax refunds this month and next month do not materialize—or they materialize after June 30—revenues booked to 2014-15 and 2015-16 could change by hundreds of millions of dollars. (Please see our prior analyses for more information.)

LAO Perspective

2016-17 Budget Act Estimates. Under the Constitution, the Legislature must include an estimate of available General Fund resources—principally 2016-17 tax revenues—in the annual budget act it passes next month. As we have noted, no one can predict the course of the economy or the stock market (and volatile capital gains) with precision. By one year from now, revenue estimates will be different from what they are now—up or down by perhaps hundreds of millions or even a few billion dollars. That being said, given that the administration’s May Revision estimate of total General Fund revenues and our revenue estimate are so similar, we believe that either would be a reasonable estimate to include in the 2016-17 budget act.

More to Come: Later This Week. Later this week, we expect to release a summary of our combined multiyear revenue and expenditure estimates, illustrating the overall condition of the General Fund—including required Proposition 2 reserves—if the Legislature were to use our revenue, property tax, and other estimates.

Follow @LAOEconTax on Twitter for regular California economy and tax updates.