LAO Contact: Ryan Miller

February 2, 2016

A Review of the CalSTRS Funding Plan

Treatment of Teacher Contributions Also Increase District Unfunded Liabilities

This post is the fourth in a series looking at the implementation of the CalSTRS funding plan. Our third post explained how theoretical asset gains have increased the school and community college district share of CalSTRS’ unfunded liabilities. Below, we continue this discussion by describing how CalSTRS’ treatment of teacher contributions has also increased the district share. We note that district contributions are fixed in law through 2020-21, making this a longer-term issue for districts.

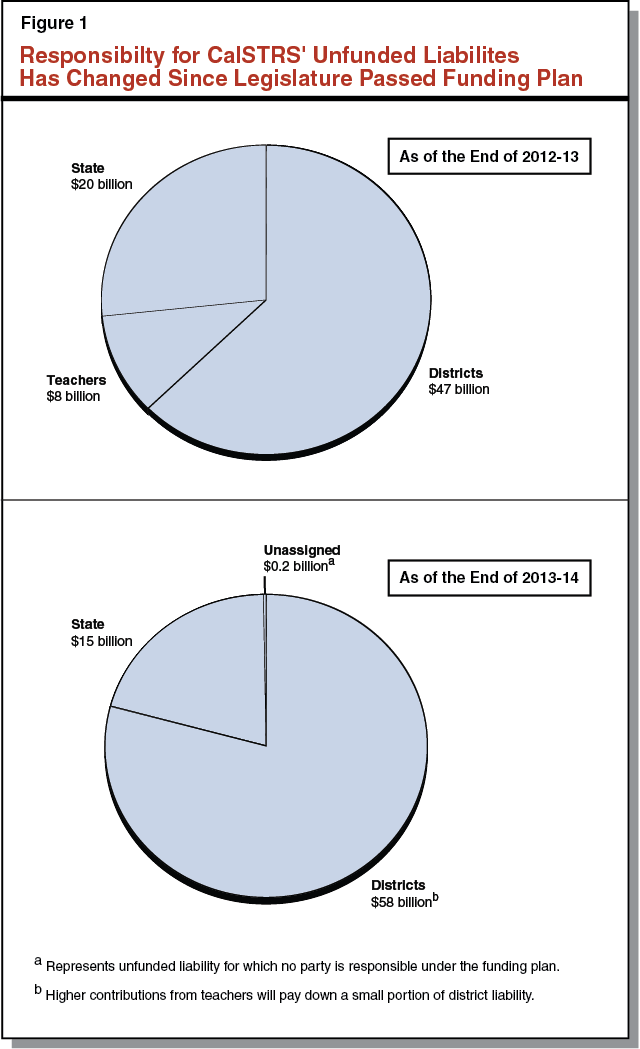

District Share of Unfunded Liability Has Increased From $47B to $58B. When the Legislature passed the CalSTRS funding plan, administration documents characterized the cost sharing as follows: districts would pay $47 billion, the state would pay $20 billion, and teachers would pay $8 billion. As of the most recent actuarial valuation, the district share has increased by about $11 billion from that initial estimate. In our earlier post, we described how the abstract calculation upon which the funding plan is based has increased the district share of CalSTRS’ unfunded liabilities by $4 billion. The remaining roughly $8 billion increase is explained by CalSTRS’ treatment of the higher teacher contributions that were required by the funding plan.

Part of Higher Teacher Contributions Will Not Be Applied to District Share. As implemented, the funding plan uses higher contributions from teachers (1) first to cover the annual cost of pension benefits (known as the “normal cost”) and (2) second to cover the district share of past unfunded liabilities. In general, when investments exceed CalSTRS’ 7.5 percent assumption and higher teacher contributions are not needed to pay for the cost of that year’s pension benefits, those contributions will be applied toward the district share of the unfunded liability. When investments underperform the 7.5 percent assumption, however, higher teacher contributions will be first used to cover the that year’s shortfall with the remainder, if any, applied to the district share. In other words, higher teacher contributions will only partially be used to pay down the district share of CalSTRS’ unfunded liabilities.

Implementation May Differ From Legislative Intent. As described above, administration documents characterized higher teacher contributions as paying for $8 billion of the $74 billion unfunded liability that existed when the funding plan was placed into law. To us, the funding law did not appear to intend for districts to pay for part of that $8 billion share. CalSTRS’ policy implementing the funding plan instead uses higher teacher contributions to pay for a part of future funding shortfalls when investments underperform assumptions. Changes to the funding plan might be necessary to ensure teacher contributions are used as the Legislature intended.