Intern Nancy Stetson was a principal contributor to this post and its infographic.

This blog post explains reassessment requirements for real property, focusing on the reassessment requirements for properties owned by legal entities.

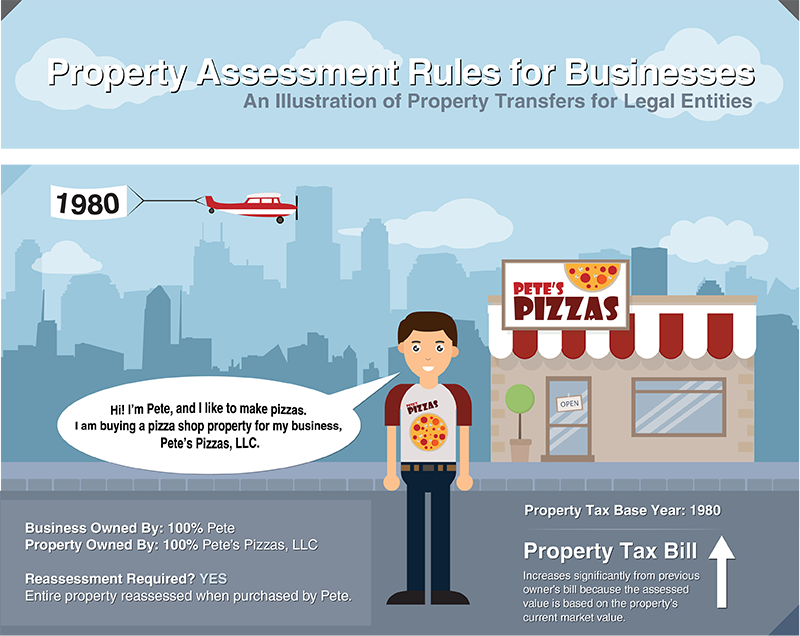

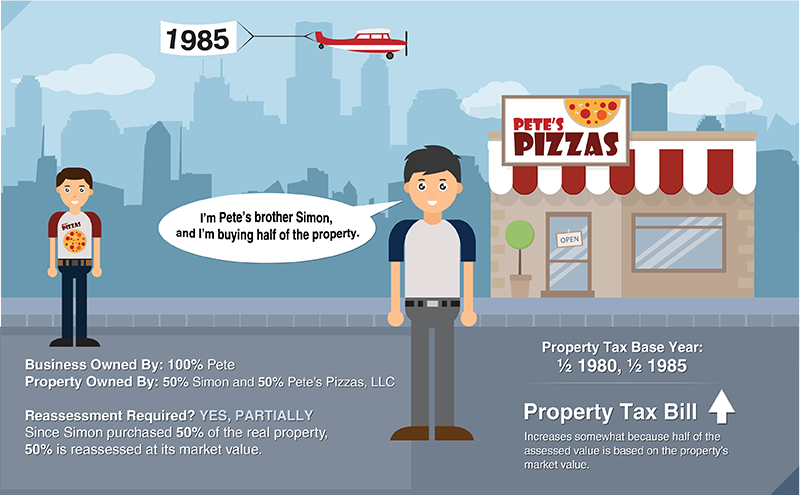

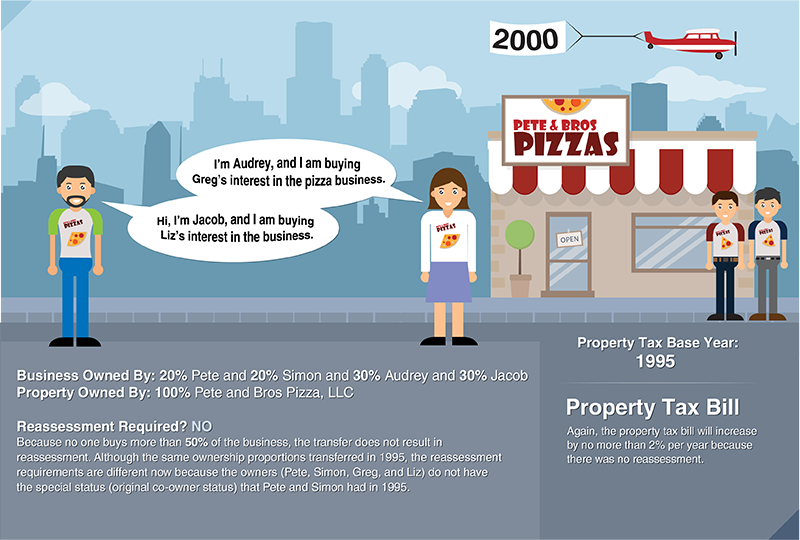

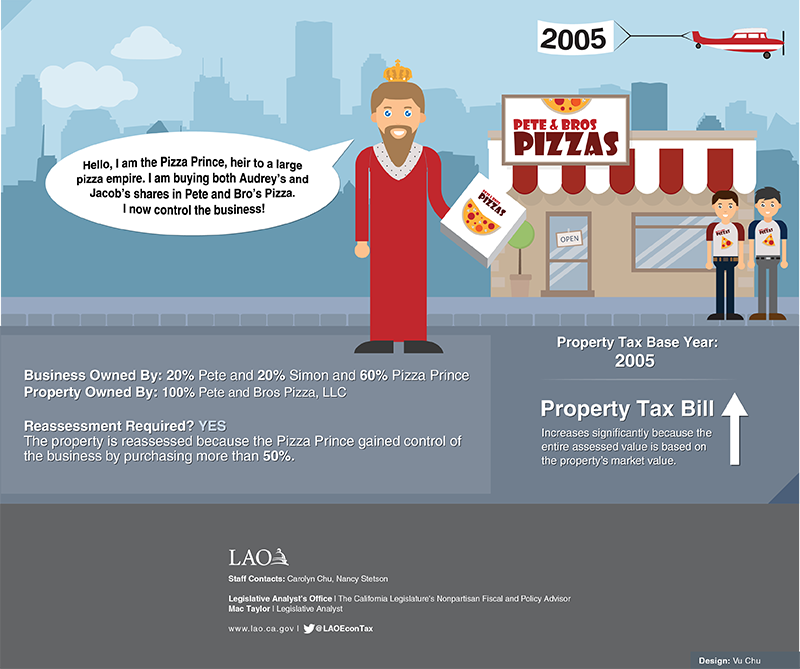

Property Taxes Based on Assessed Value. Under Proposition 13, property taxes are limited to 1 percent of the assessed value of land and buildings. County assessors determine the assessed value of property, which reflects the “full cash value” when there is a change in ownership. Once the county assessor sets the assessed value of a property, that value cannot grow by more than 2 percent per year unless there is a “change in ownership.” At that time, the county assessor reassesses the property. (In some cases, the value of the property can decline. For information about reduced assessments, see our report here.) In most cases, when a property is reassessed due to a change in ownership the property tax bill for that property increases because the market value of property typically grows faster than the assessed value of property.

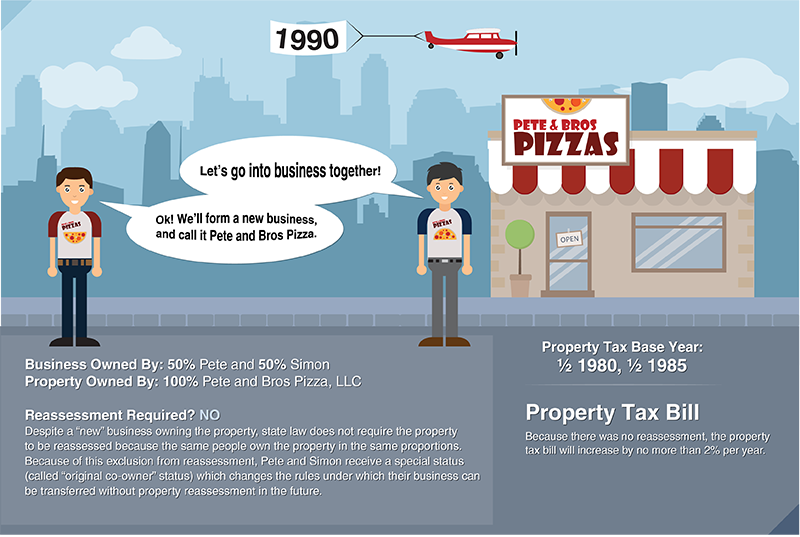

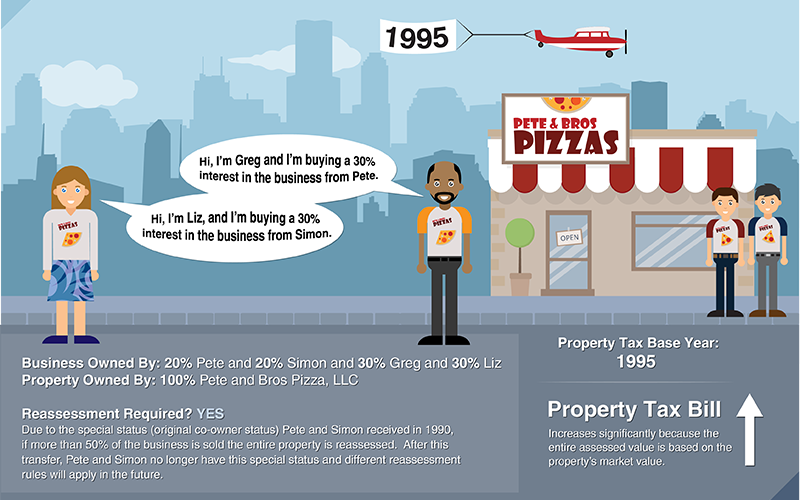

Change in Ownership Differs for Individuals and Legal Entities. Generally, real property—like land and buildings—can be owned by individuals or legal entities. Legal entities include sole proprietorships, limited liability companies, corporations, trusts, and the like. While property transfers between individuals usually trigger reassessment, properties owned by a legal entity are not necessarily reassessed when ownership of the legal entity changes. In these cases, the owners of the legal entity change, but the legal entity remains the owner of the property. As a result, only some changes in legal entity ownership result in reassessment. The infographic below explains some of the ways reassessment requirements vary based on the parties involved and the amount of property transferred.

Legal Entity Changes in Ownership Are A Fraction of Overall Property Transfers. As seen in the infographic, only some transfers of ownership result in reassessment of a property. Statewide, the properties reassessed due to changes in ownership of legal entities (like those in 1995 and 2005 in the infographic) are between 1 and 2 percent of all property transfers each year. The share of properties not reassessed despite some ownership change (like those in 1990 and 2000 in the infographic) is unknown because there is no requirement to report these changes to county assessors or the state.

Disclaimer: This infographic and blog post are not exhaustive reviews of property reassessment requirements for legal entities. For more information, please see the Legal Entity Ownership Program at the State Board of Equalization and/or consult experts in this area of tax law.

Follow @LAOEconTax on Twitter for regular California economy and tax updates.