Submitted July 18, 2012

Proposition 39

Tax Treatment for Multistate Businesses. Clean Energy and Energy Efficiency Funding. Initiative Statue.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact

-

Fiscal Impact: Increased state revenues of $1 billion annually, with half of the revenues over the next five years spent on energy efficiency projects. Of the remaining revenues, a significant portion likely would be spent on schools.

Yes/No Statement

A YES vote on this measure means: Multistate businesses would no longer be able to choose the method for determining their state taxable income that is most advantageous for them. Some multistate businesses would have to pay more corporate income taxes due to this change. About half of this increased tax revenue over the next five years would be used to support energy efficiency and alternative energy projects.

A NO vote on this measure means: Most multistate businesses would continue to be able to choose one of two methods to determine their California taxable income.

|

Background

State Corporate Income Taxes. The amount of money a business owes the state in corporate income taxes each year is based on the business’ taxable income. For a business that operates both in California and in other states or countries (a multistate business), the state taxes only the part of its income that was associated with California. While only a small portion of corporations are multistate in nature, multistate corporations pay the vast majority of the state’s corporate income taxes. This tax is the state’s third largest General Fund revenue source, raising $9.6 billion in 2010-11.

Multistate Businesses Choose How Their Taxable Income Is Determined. Currently, state law allows most multistate businesses to pick one of two methods to determine the amount of their income associated with California and taxable by the state:

-

“Three-Factor Method” of Determining Taxable Income. One method uses the location of the company’s sales, property, and employees. When using this method, the more sales, property, or employees the multistate business has in California, the more of the business’ income is subject to state tax.

-

“Single Sales Factor Method” of Determining Taxable Income. The other method uses only the location of the company’s sales. When using this method, the more sales the multistate business has in California, the more of the business’ income is taxed. (For example, if one-fourth of a company’s product was sold in California and the remainder in other states, one-fourth of the company’s total profits would be subject to California taxation.)

Multistate businesses generally are allowed to choose the method that is most advantageous to them for tax purposes.

Energy Efficiency Programs. There are currently numerous state programs established to reduce energy consumption. These efforts are intended to reduce the need to build new energy infrastructure (such as power plants and transmission lines) and help meet environmental quality standards. For example, the California Public Utilities Commission (CPUC) oversees various types of energy efficiency upgrade and appliance rebate programs that are funded by monies collected from utility ratepayers. In addition, the California Energy Commission (CEC) develops building and appliance standards that are intended to reduce energy consumption in the state.

School Funding Formula. Proposition 98, passed by voters in 1988 and modified in 1990, requires a minimum level of state and local funding each year for public schools and community colleges (hereafter referred to as schools). This funding level is commonly known as the Proposition 98 minimum guarantee. Though the Legislature can suspend the guarantee and fund at a lower level, it typically decides to provide funding equal to or greater than the guarantee. The Proposition 98 guarantee can grow with increases in state General Fund revenues (including those collected from state corporate income taxes). Accordingly, a measure—such as this one—that results in higher revenues also can result in a higher school funding guarantee. Proposition 98 expenditures are the largest category of spending in the state’s budget—totaling roughly 40 percent of state General Fund expenditures.

Proposal

Eliminates Ability of Multistate Businesses to Choose How Taxable Income Is Determined. Under this measure, starting in 2013, multistate businesses would no longer be allowed to choose the method for determining their state taxable income that is most advantageous for them. Instead, most multistate businesses would have to determine their California taxable income using the single sales factor method. Businesses that operate only in California would be unaffected by this measure.

This measure also includes rules regarding how all multistate businesses calculate the portion of some sales that are allocated to California for state tax purposes. These include a set of specific rules for certain large cable companies.

Provides Funding for Energy Efficiency and Alternative Energy Projects. This measure establishes a new state fund, the Clean Energy Job Creation Fund, to support projects intended to improve energy efficiency and expand the use of alternative energy. The measure states that the fund could be used to support: (1) energy efficiency retrofits and alternative energy projects in public schools, colleges, universities, and other public facilities; (2) financial and technical assistance for energy retrofits; and (3) job training and workforce development programs related to energy efficiency and alternative energy. The Legislature would determine spending from the fund and be required to use the monies for cost-effective projects run by agencies with expertise in managing energy projects. The measure also (1) specifies that all funded projects must be coordinated with CEC and CPUC and (2) creates a new nine-member oversight board to annually review and evaluate spending from the fund.

The Clean Energy Job Creation Fund would be supported by some of the new revenue raised by moving to a mandatory single sales factor. Specifically, half of the revenues so raised—up to a maximum of $550 million—would be transferred annually to the Clean Energy Job Creation Fund. These transfers would occur for only five fiscal years—2013-14 through 2017-18.

Fiscal Effects

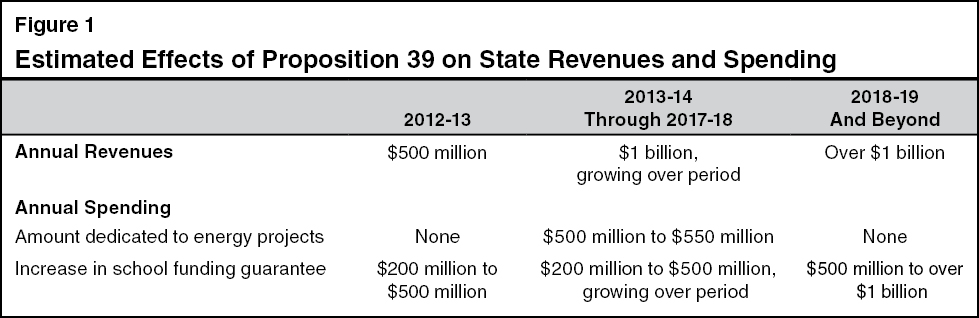

Increase in State Revenues. As shown in the top line in Figure 1, this measure would increase state revenues by around $1 billion annually starting in 2013-14. (There would be a roughly half-year impact in 2012-13.) The increased revenues would come from some multistate businesses paying more taxes. The amounts generated by this measure would tend to grow over time.

Some Revenues Used for Energy Projects. For a five-year period (2013-14 through 2017-18), about half of the additional revenues—$500 million to $550 million annually—would be transferred to the Clean Energy Job Creation Fund to support energy efficiency and alternative energy projects.

School Funding Likely to Rise Due to Additional Revenues. Generally, the revenue raised by the measure would be considered in calculating the state’s annual Proposition 98 minimum guarantee. The funds transferred to the Clean Energy Job Creation Fund, however, would not be used in this calculation. As shown in the bottom part of Figure 1, the higher revenues likely would increase the minimum guarantee by at least $200 million for the 2012-13 through 2017-18 period. In some years during this period, however, the minimum guarantee could be significantly higher. For 2018-19 and beyond, the guarantee likely would be higher by at least $500 million. As during the initial period, the guarantee in some years could be significantly higher. The exact portion of the revenue raised that would go to schools in any particular year would depend upon various factors, including the overall growth in state revenues and the size of outstanding school funding obligations.

Return to Propositions

Return to Legislative Analyst's Office Home Page