Submitted July 18, 2012

(Reflects court ordered changes.)

Proposition 38

Tax for Education and Early Childhood Programs. Initiative Statute.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact

-

Fiscal Impact: Increased state tax revenues for 12 years—roughly $10 billion annually in initial years, tending to grow over time. Funds used for schools, child care, and preschool, as well as providing savings on state debt payments.

Yes/No Statement

A YES vote on this measure means: State personal income tax rates would increase for 12 years. The additional revenues would be used for schools, child care, preschool, and state debt payments.

A NO vote on this measure means: State personal income tax rates would remain at their current levels. No additional funding would be available for schools, child care, preschool, and state debt payments.

|

Overview

This measure raises personal income taxes on most California taxpayers from 2013 through 2024. The revenues raised by this tax increase would be spent on public schools, child care and preschool programs, and state debt payments. Each of the measure’s key provisions is discussed in more detail below.

State Taxes and Revenues

Background

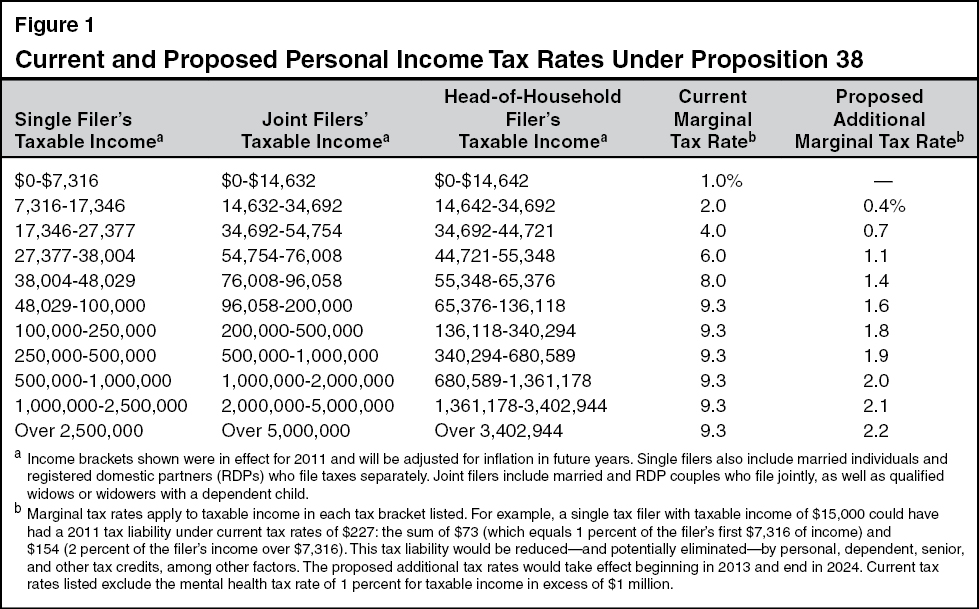

Personal Income Tax (PIT). The PIT is a tax on wage, business, investment, and other income of individuals and families. State PIT rates range from 1 percent to 9.3 percent on the portions of a taxpayer’s income in each of several income brackets. (These are referred to as marginal tax rates.) Higher marginal tax rates are charged as income increases. The tax revenue generated from this tax—totaling $49.4 billion for the 2010-11 fiscal year—is deposited into the state’s General Fund. In addition, an extra 1 percent tax applies to annual income over $1 million (with the associated revenue dedicated to mental health services).

Proposal

Increases PIT Rates. This measure increases state PIT rates on all but the lowest income bracket, effective over the 12-year period from 2013 through 2024. As shown in Figure 1, the additional marginal tax rates would increase with each higher tax bracket. For example, for joint filers, an additional 0.7 percent marginal tax rate would be imposed on income between $34,692 and $54,754, increasing the total rate to 4.7 percent. Similarly, an additional 1.1 percent marginal tax rate would be imposed on income between $54,754 and $76,008, increasing the total rate to 7.1 percent. These higher tax rates would result in higher tax liabilities on roughly 60 percent of state PIT returns. (Personal, dependent, senior, and other tax credits, among other factors, would continue to eliminate all tax liabilities for many lower-income tax filers even if they have income in a bracket affected by the measure’s rate increases.) The additional 1 percent rate for mental health services would still apply to income in excess of $1 million. This measure’s rate changes, therefore, would increase these taxpayers’ marginal PIT rates from 10.3 percent to as much as 12.5 percent. Proposition 30 on this ballot also would increase PIT rates. The nearby box describes what would happen if both measures are approved.

What Happens if Voters Approve Both

Proposition 30 and Proposition 38?

State Constitution Specifies What Happens if Two Measures Conflict. If provisions of two measures approved on the same statewide ballot conflict, the Constitution specifies that the provisions of the measure receiving more “yes” votes prevail. Proposition 30 and Proposition 38 on this statewide ballot both increase personal income tax (PIT) rates and, as such, could be viewed as conflicting.

Measures State That Only One Set of Tax Increases Goes Into Effect. Proposition 30 and Proposition 38 both contain sections intended to clarify which provisions are to become effective if both measures pass:

-

If Proposition 30 Receives More Yes Votes. Proposition 30 contains a section indicating that its provisions would prevail in their entirety and none of the provisions of any other measure increasing PIT rates—in this case Proposition 38—would go into effect.

-

If Proposition 38 Receives More Yes Votes. Proposition 38 contains a section indicating that its provisions would prevail and the tax rate provisions of any other measure affecting sales or PIT rates—in this case Proposition 30—would not go into effect. Under this scenario, the spending reductions known as the “trigger cuts” would take effect as a result of Proposition 30’s tax increases not going into effect. (See the analysis of Proposition 30 for more information on the trigger cuts.)

|

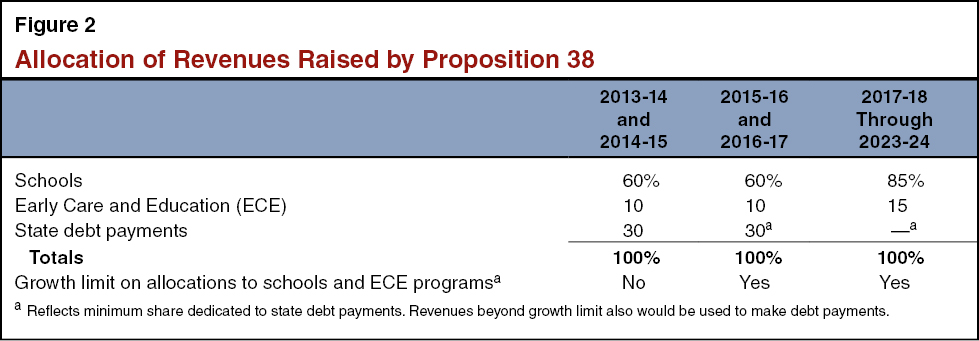

Provides Funds for Public Schools, Early Care and Education (ECE), and Debt Service. The revenues raised by the measure would be deposited into a newly created California Education Trust Fund (CETF). These funds would be dedicated exclusively to three purposes. As shown in Figure 2, in 2013-14 and 2014-15, the measure allocates 60 percent of CETF funds to schools, 10 percent of funds to ECE programs, and 30 percent of funds to make state debt payments. In 2015-16 and 2016-17, the same general allocations are authorized but a somewhat higher share could be used for state debt payments. This is because beginning in 2015-16, the measure: (1) limits the growth in total allocations to schools and ECE programs based on the average growth in California per capita personal income over the previous five years and

(2) dedicates the funds collected above the growth rate to state debt payments. From 2017-18 through 2023-24, up to 85 percent of CETF funds would go to schools and up to 15 percent would go to ECE programs, with revenues in excess of the growth rate continuing to be used for state debt payments.

Cannot Be Amended by the Legislature. If adopted by voters, this measure could be amended only by a future ballot measure. The Legislature would be prohibited from making any modifications to the measure without voter approval.

Fiscal Effect

Around $10 Billion of Additional Annual State Revenues. In the initial years—beginning in 2013-14—the annual amount of additional state revenues raised would be around $10 billion. (In 2012-13, the measure would result in additional state revenues of about half this amount.) The total revenues generated would tend to grow over time. Revenues generated in any particular year, however, could be much higher or lower than the prior year. This is mainly because the measure increases tax rates more for upper-income taxpayers. The income of these individuals tends to swing more significantly because it is affected to a much greater extent by changes in the stock market, housing prices, and other investments. Due to the swings in the income of these taxpayers and the uncertainty of their responses to the rate increases, the revenues raised by this measure are difficult to estimate.

Schools

Background

Most Public School Funding Tied to State Funding Formula. California provides educational services to about 6 million public school students. These students are served through more than 1,000 local educational agencies—primarily school districts. Most school funding is provided through the state’s school funding formula—commonly called the Proposition 98 minimum guarantee. (Community college funding also applies toward meeting the minimum guarantee.) The minimum guarantee is funded through a combination of state General Fund and local property tax revenues. In 2010-11, schools received $43 billion from the school funding formula.

Most School Spending Decisions Are Made by Local Governing Boards. Roughly 70 percent of state-related school funding can be used for any educational purpose. In most cases, the school district governing board decides how the funds should be spent. The governing board typically will determine the specific activities for which the funds will be used, as well as how the funds will be distributed among the district’s school sites. The remaining 30 percent of funds must be used for specified purposes, such as serving school meals or transporting students to and from school. School districts typically have little flexibility in how to use these restricted funds.

Proposal

Under this measure, schools will receive roughly 60 percent of the revenues raised by the PIT rate increases through 2016-17 and roughly 85 percent annually thereafter. These CETF funds would be in addition to Proposition 98 General Fund support for schools. The funds support three grant programs. The measure also creates spending restrictions and reporting requirements related to these funds. These major provisions are discussed in more detail below.

Distributes School Funds Through Three Grant Programs. Proposition 38 requires that CETF school funds be allocated as follows:

-

Educational Program Grants (70 Percent of Funds).The largest share of funds—70 percent of all CETF school funding—would be distributed based on the number of students at each school. The specific per-student grant, however, would depend on the grade of each student, with schools receiving more funds for students in higher grades. Educational program grants could be spent on a broad range of activities, including instruction, school support staff (such as counselors and librarians), and parent engagement.

-

Low-Income Student Grants (18 Percent of Funds). The measure requires that 18 percent of CETF school funds to be allocated at one statewide rate based on the number of low-income students (defined as the number of students eligible for free school meals) enrolled in each school. As with the educational program grants, low-income student grants could be spent on a broad range of educational activities.

-

Training, Technology, and Teaching Materials Grants (12 Percent of Funds). The remaining 12 percent of funds would be allocated at one statewide rate based on the number of students at each school. The funds could be used only for training school staff and purchasing up-to-date technology and teaching materials.

Requires Funds Be Spent at Corresponding School Sites. Funds received by school districts from this measure must be spent at the specific school whose students generated the funds. In the case of low-income student grants, for example, if 100 percent of low-income students in a school district were located in one particular school, all low-income grant funds would need to be spent at that specific school. As with most other school funding, however, the local governing board would determine how CETF funds are spent at each school site. To ensure that Proposition 38 funds would result in a net increase in funding for all schools, the measure also would require school districts to make reasonable efforts to avoid reducing per-student funding from non-CETF sources at each school site below 2012-13 levels. If a school district reduces the per-student funding for any school site below the 2012-13 level, it must explain the reasons for the reduction in a public meeting held at or near the school.

Requires School Districts to Seek Public Input Prior to Making Spending Decisions. Proposition 38 also requires school district governing boards at an open public hearing to seek input from students, parents, teachers, administrators, and other school staff on how to spend CETF school funds. When the governing board decides how to spend the funds, it must explain—publicly and online—how CETF school expenditures will improve educational outcomes and how those improved outcomes will be measured.

Creates Budget Reporting Requirements for Each School. The measure also includes several reporting requirements for school districts. Most notably, beginning in 2012-13, the measure requires all school districts to create and publish an online budget for each of their schools. The budget must show funding and expenditures at each school from all funding sources, broken down by various spending categories. The state Superintendent of Public Instruction must provide a uniform format for budgets to be reported and must make all school budgets available to the public, including data from previous years. In addition, school districts must provide a report on how CETF funds were spent at each of their schools within 60 days after the close of the school year.

Other Allowances and Prohibitions. The measure allows up to 1 percent of a school district’s allocation to be spent on budgeting, reporting, and audit requirements. The measure prohibits CETF school funds from being used to provide salary or benefit increases unless the increases are provided to other like employees that are funded with non-CETF dollars. The measure also has a provision that prohibits CETF school monies from being used to replace state, local, or federal funding provided as of November 1, 2012.

Fiscal Effect

Provides Additional Funding for Schools. In the initial years, schools would receive roughly $6 billion annually, or $1,000 per student, from the measure. Of that amount, $4.2 billion would be provided for education program grants, $1.1 billion for low-income student grants, and $700 million for training, technology, and teaching materials grants. (The 2013-14 amounts would be higher because the funds raised in 2012-13 also would be available for distribution.) The amounts available in future years would tend to grow over time. Beginning in 2017-18, the amount spent on schools would increase further as the amount required to be used for state debt payments decreases significantly.

Early Care and Education

Background

ECE Programs Serve Children Ages Five and Younger. Prior to attending kindergarten—which usually starts at age five—most California children attend some type of ECE program. Families participate in these programs for a variety of reasons, including supervision of children while parents are working and development of a child’s social and cognitive skills. Programs serving children ages birth to three typically are referred to as infant and toddler care. Programs serving three to five year-old children often are referred to as preschool and typically have an explicit focus on helping prepare children for kindergarten. Whereas all programs must meet basic health and safety standards to be licensed by the state, the specific characteristics of programs—including staff qualifications, adult-to-child ratios, curriculum, family fees, and cost of care—vary.

Some Children Are Eligible for Subsidized ECE Services. While many families pay to participate in ECE programs, public funds also subsidize services for some children. These subsidies generally are reserved for families that are low income, participate in welfare-to-work programs or other work or training activities, and/or have children with special needs. Generally, eligibility for ECE subsidies is limited to families that earn 70 percent or less than the state median income level (for example, currently the limit is $3,518 per month for a family of three). The state pays a set per-child rate to providers for subsidized ECE “slots.” The payment rate varies by region of the state and care setting. It typically is about $1,000 per month for full-time infant/toddler care and $700 per month for full-time preschool.

Current Funding Levels Do Not Subsidize ECE Programs for All Eligible Children. In 2010-11, state and federal funds provided roughly $2.6 billion to offer a variety of child care and preschool programs for approximately 500,000, or about 15 percent, of California children ages five and younger. Roughly half of all California children, however, meet income eligibility criteria for subsidized programs. Because state and federal ECE funding is not sufficient to provide subsidized services for all eligible children, waiting lists are common in most counties.

Proposal

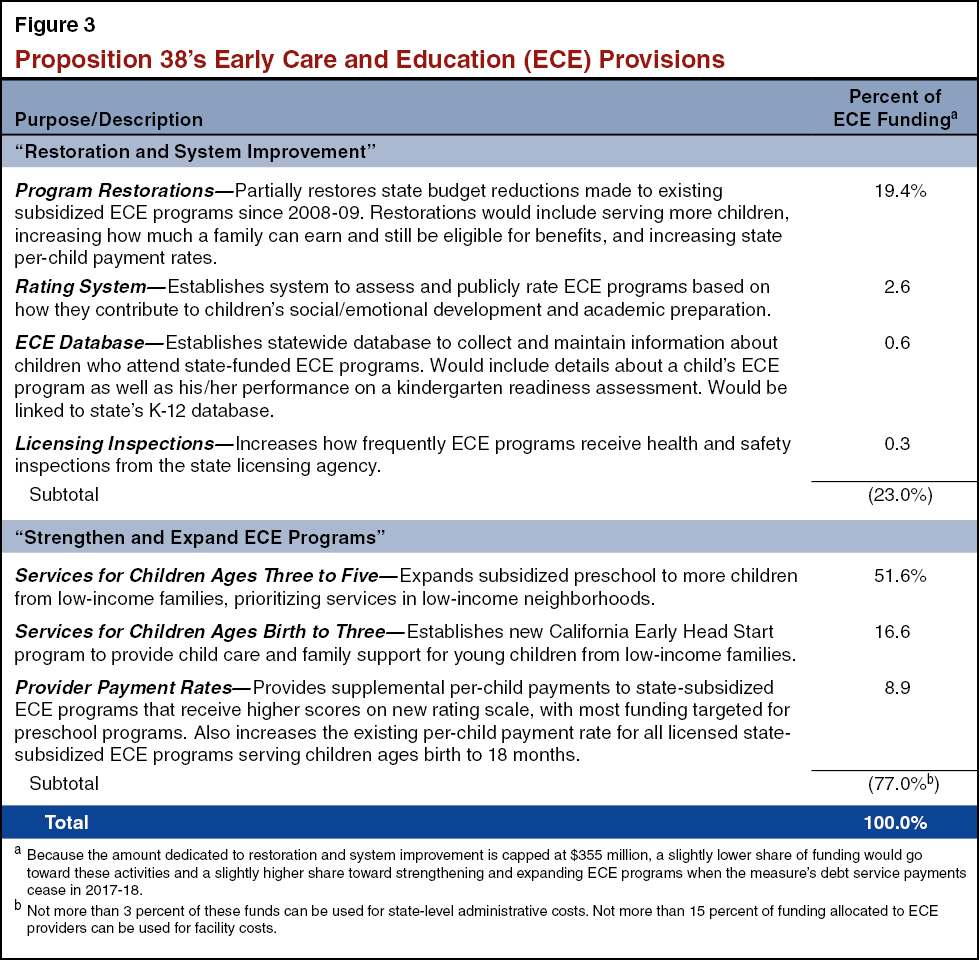

As noted earlier, ECE programs will receive roughly 10 percent of the revenues raised by the PIT rate increases through 2016-17 and roughly 15 percent annually thereafter. The measure provides specific allocations of these funds, as summarized in Figure 3. As shown in the top part of the figure, up to 23 percent of the funds raised for ECE programs would be dedicated to restoring recent state budget reductions to child care slots and provider payment rates as well as implementing certain statewide activities designed to support the state’s ECE system. The remaining ECE funds, shown in the bottom part of the figure, would expand child care and preschool programs to serve more children from low-income families and increase payment rates for certain ECE providers. The measure also prohibits the state from reducing existing support for ECE programs. Specifically, the state would be required to spend the same proportion of state General Fund revenues for ECE programs in future years as it is spending in 2012-13 (roughly 1 percent). As described in more detail below, the measure includes extensive provisions relating to: (1) a rating system for evaluating ECE programs, (2) preschool, and (3) infant and toddler care.

Establishes Statewide Rating System to Assess the Quality of Individual ECE Programs. The measure requires the state to implement an “Early Learning Quality Rating and Improvement System” (QRIS) to assess the effectiveness of individual ECE programs. Building on initial work the state already has undertaken, the state would have until January 2014 to develop a scale to evaluate how well programs contribute to children’s social and emotional development and academic preparation. All ECE programs could choose to be rated on this scale, and ratings would be available to the public. The state also would develop a training program to help providers improve their services and increase their ratings. Additionally, Proposition 38 would provide supplemental payments—on top of existing per-child subsidy rates—to child care and preschool programs that achieve higher scores on the QRIS scale.

Provides Preschool to More Children from Low-Income Families. Proposition 38 expands the number of slots available in state-subsidized preschool programs located in neighborhoods with high concentrations of low-income families. Funding to offer these new slots would only be available to preschool providers with higher quality ratings. Funding would be allocated to providers based on the estimated number of eligible children living in the targeted neighborhoods who do not currently attend preschool. (At least 65 percent of these new slots must be in programs that offer full-day, full-year services.) Program participation would be limited to children meeting existing family income eligibility criteria or living in the target neighborhoods regardless of family income, with highest priority given to certain at-risk children (including those in foster care).

Establishes New Program for Infants and Toddlers from Low-Income Families. Proposition 38 establishes the California Early Head Start (EHS) Program, modeled after the federal program of the same name. Up to 65 percent of funding for this program would offer both child care and family support services to low-income families with children ages birth to three. (At least 75 percent of these new slots must be for full-day, full-year care.) At least 35 percent of EHS funding would provide support services for families and caregivers not participating in the child care component of the program. In both cases, family support services could include home visits from program staff, assessments of child development, family literacy programs, and parent and caregiver training.

Fiscal Effect

Provides Additional Funding to Support and Expand ECE Programs. In the initial years, roughly $1 billion annually from the measure would be used for the state’s ECE system. (The 2013-14 amount would be higher because the funds raised in 2012-13 also would be available for distribution.) The majority of funding would be dedicated to expanding child care and preschool—serving roughly an additional 10,000 infants/toddlers and 90,000 preschoolers in the initial years of implementation. The amount available in future years would tend to grow over time. Beginning in 2017-18, the amount spent on ECE programs would increase further as the amount required to be used for state debt payments decreases significantly.

State Debt Payments

Background

General Obligation Bond Debt Payments. Bond financing is a type of long-term borrowing that the state uses to raise money, primarily for long-lived infrastructure (including school and university buildings, highways, streets and roads, land and wildlife conservation, and water-related facilities). The state obtains this money by selling bonds to investors. In exchange, the state promises to repay this money, with interest, according to a specified schedule. The majority of the state’s bonds are general obligation bonds, which must be approved by the voters and are guaranteed by the state’s general taxing power. General obligation bonds are typically paid off with annual debt-service payments from the General Fund. In 2010-11, the state made $4.7 billion in general obligation bond debt-service payments. Of that amount, $3.2 billion was to pay for debt service on school and university facilities.

Proposal

At Least 30 Percent of Revenues for Debt-Service Relief Through 2016-17. Until the end of 2016-17, at least 30 percent of Proposition 38 revenues would be used by the state to pay debt-service costs. The measure requires that these funds first be used to pay education debt-service costs (pre-kindergarten through university school facilities). If, however, funds remain after paying annual education debt-service costs, the funds can be used to pay other state general obligation bond debt-service costs.

Limits Growth of School and ECE Allocations Beginning 2015-16, Uses Excess Funds for Debt-Service Payments. Beginning in 2015-16, total CETF allocations to schools and ECE programs could not increase at a rate greater than the average growth in California per capita personal income over the previous five years. The CETF monies collected in excess of this growth rate also would be used for state debt payments. (The measure provides an exception for 2017-18, given the changes in the revenue allocations.)

Fiscal Effect

General Fund Savings of Roughly $3 Billion Annually Through 2016-17. Until the end of 2016-17, at least 30 percent of the revenue raised by the measure—roughly $3 billion annually—would be used to pay general obligation debt-service costs and provide state General Fund savings. This would free up General Fund revenues for other public programs and make it easier to balance the budget in these years.

Potential Additional General Fund Savings Beginning in 2015-16. The measure’s growth limit provisions also would provide General Fund savings in certain years. The amount of any savings would vary from year to year depending on the growth of PIT revenue and per capita personal income but could be several hundred million dollars annually.

Return to Propositions

Return to Legislative Analyst's Office Home Page