(Adobe Acrobat-- print version.)

Submitted August 29, 2008

An Overview of State Bond Debt

This section provides an overview of the state’s current

situation involving bond debt. It also discusses the impact that the bond

measures on this ballot, if approved, would have on the state’s debt level and

the costs of paying off such debt over time.

Background

What Is Bond Financing? Bond financing is a

type of long-term borrowing that the state uses to raise money for various

purposes. The state obtains this money by selling bonds to investors. In

exchange, it agrees to repay this money, with interest, according to a specified

schedule.

Why Are Bonds Used? The state has

traditionally used bonds to finance major capital outlay projects such as roads,

educational facilities, prisons, parks, water projects, and office buildings

(that is, public infrastructure-related projects). This is done mainly because

these facilities provide services over many years, their large dollar costs can

be difficult to pay for all at once, and the different taxpayers who pay off the

bonds benefit over time from the facilities. Bonds also have been used to help

finance certain private infrastructure, such as housing.

What Types of Bonds Does the State Sell?

The state sells three major types of bonds to finance projects. These are:

- General Obligation Bonds. Most of these

are directly paid off from the state’s General Fund, which is largely

supported by tax revenues. Some, however, are paid for by designated revenue

sources, with the General Fund only providing back-up support in the event

the revenues fall short. (An example is the Cal-Vet program, under which

bonds are issued to provide home loans to veterans and are paid off using

veterans’ mortgage payments.) General obligation bonds must be approved by

the voters and their repayment is guaranteed by the state’s general taxing

power.

- Lease-Revenue Bonds. These bonds are paid

off from lease payments (primarily financed from the General Fund) by state

agencies using the facilities the bonds finance. These bonds do not require

voter approval and are not guaranteed by the state’s general taxing power.

As a result, they have somewhat higher interest costs than general

obligation bonds.

- Traditional Revenue Bonds. These also

finance capital projects but are not supported by the General Fund. Rather,

they are paid off from a designated revenue stream generated by the projects

they finance—such as bridge tolls. These bonds also are not guaranteed by

the state’s general taxing power and do not require voter approval.

Budget-Related Bonds. Recently, the state

has also used bond financing to help close major shortfalls in its General Fund

budget. In March 2004, the voters approved Proposition 57, authorizing

$15 billion in general obligation bonds to help pay off the state’s accumulated

budget deficit and other obligations. Of this amount, $11.3 billion was raised

through bond sales in May and June of 2004, and the remaining available

authorizations were sold in February 2008. These bonds will be paid off over the

next several years. They are excluded from the remainder of this discussion,

which focuses on infrastructure-related bonds.

What Are the Direct Costs of Bond Financing?

The state’s cost for using bonds depends primarily on the amount sold, their

interest rates, the time period over which they are repaid, and their maturity

structure. For example, the most recently sold general obligation bonds will be

paid off over a 30-year period with fairly level annual payments. Assuming that

a bond issue carries a tax-exempt interest rate of 5 percent, the cost of paying

it off with level payments over 30 years is close to $2 for each dollar

borrowed—$1 for the amount borrowed and close to $1 for interest. This cost,

however, is spread over the entire 30-year period, so the cost after adjusting

for inflation is considerably less—about $1.30 for each $1 borrowed.

The State’s Current Debt Situation

Amount of General Fund Debt. As of June 1,

2008, the state had about $53 billion of infrastructure-related General Fund

bond debt outstanding on which it is making principal and interest payments.

This consists of about $45 billion of general obligation bonds and $8 billion of

lease-revenue bonds. In addition, the state has not yet sold about $68 billion

of authorized general obligation and lease-revenue infrastructure bonds. Most of

these bonds have been committed to projects, but the projects involved have not

yet been started or those in progress have not yet reached their major

construction phase.

General Fund Debt Payments. We estimate

that General Fund debt payments for infrastructure-related general obligation

and lease-revenue bonds were about $4.4 billion in 2007-08. As previously

authorized but currently unsold bonds are marketed, outstanding bond debt costs

will rise, peaking at approximately $9.2 billion in 2017‑18.

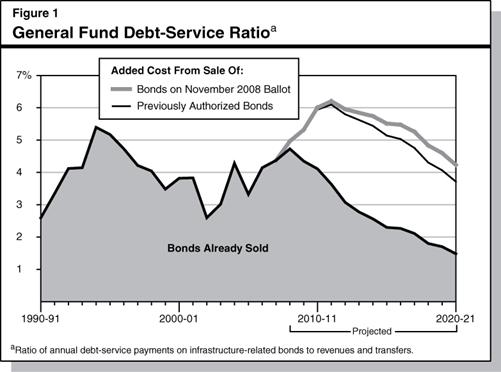

Debt-Service Ratio. One indicator of the

state’s debt situation is its debt-service ratio (DSR). This ratio indicates the

portion of the state’s annual revenues that must be set aside for debt-service

payments on infrastructure bonds and therefore are not available for other state

programs. As shown in Figure 1, the DSR increased in the early 1990s and peaked

at 5.4 percent before falling back to below 3 percent in 2002-03, partly due to

some deficit-refinancing activities. The DSR then rose again beginning in

2003-04 and currently stands at 4.4 percent for infrastructure bonds. It is

expected to increase to a peak of 6.1 percent in 2011-12 as currently authorized

bonds are sold.

Effects of the Bond Propositions on This Ballot

There are four general obligation bond measures on this

ballot, totaling $16.8 billion in new authorizations. These include:

- Proposition 1A, which would authorize the state to issue

$9.95 billion of bonds to finance a high-speed rail project.

- Proposition 3, which would authorize the state to issue

$980 million of bonds for capital improvement projects at children’s

hospitals.

- Proposition 10, which would authorize the state to

issue $5 billion of bonds for various renewable energy, alternative fuel,

energy efficiency, and air emissions reduction purposes.

- Proposition 12, which would authorize the state to

issue $900 million of bonds under the Cal-Vet program to be paid off from

mortgage payments.

Impacts on Debt Payments. If the three

General Fund-supported bonds on this ballot (Propositions 1A, 3, and 10) are all

approved, they would require total debt-service payments over the life of the

bonds of about twice their authorized amount. The average annual debt service on

the bonds would depend on the timing and conditions of their sales. Once all

these bonds were sold, the estimated annual budgetary cost would be about

$1 billion.

Impact on the Debt-Service Ratio. Figure 1

shows what would happen to the state’s estimated DSR over time if all of the

bonds were approved and sold. It would peak at 6.2 percent in 2011-12, and

decline thereafter. (Future debt-service costs shown in Figure 1 would be higher

if, for example, voters approved additional bonds in elections after November

2008.)

Prepared by the Legislative Analyst’s Office

Return to Propositions

Return to Legislative Analyst's Office Home Page