LAO Contact

Related Publications

December 21, 2017

Long-Term Capacity for Debt Payments Under Proposition 2

Our recent Fiscal Outlook publication provided our short-term and longer-term outlook for the state budget. The Fiscal Outlook considers potential future requirements under Proposition 2 (2014)—including required rainy day fund deposits and payments toward certain state debts. Some have asked whether Proposition 2 debt funding payments can be used to reduce liabilities of teacher and other public employees' pension plans. As we discuss in this post, there may be little ongoing capacity to make additional commitments from Proposition 2 debt funding payments through the mid-2020s. The Legislature, however, could change the state’s existing Proposition 2 debt payment priorities (to prioritize different types of debt) or use non-Proposition 2 resources to pay down additional liabilities, such as pension debt.

Provisions of Proposition 2

Key Provisions of Proposition 2. Proposition 2 requires the state to make: (1) minimum annual payments toward certain eligible debts (until 2029‑30) and (2) deposits into the state’s rainy day fund. Proposition 2 has a two part calculation to determine the amounts the state must dedicate for each of these purposes. First, it requires the state to put aside 1.5 percent of General Fund revenues (the “base amount”). Second, it requires the state to put aside a portion of capital gains revenues that exceed a specified threshold (“excess capital gains”). The state combines these two amounts and allocates half of the total to pay down debts and the other half to build the rainy day reserve.

True Up Provisions. Under Proposition 2’s “true up” provisions, the state reevaluates the estimate of Proposition 2 requirements twice: once in each two subsequent budgets. Under these reevaluations, the rainy day fund deposit is revised up (down) if capital gains taxes were higher (lower) than the state’s prior estimates. The state does not revisit its estimate of the base amount in the true up calculation. Debt payments are also not adjusted when new capital gains estimates are available later.

Proposition 2 Debt Funding Priorities

While there is no overarching statutory plan for future Proposition 2 debt payments, the Legislature and Governor have agreed—in some cases, informally, and, in a few cases, in state law—to prioritize certain debts that involve multiyear commitments. This section describes these agreements and the commitments now being funded by Proposition 2 debt payments. (A more detailed list of Proposition 2 eligible debts and recent uses of funding is available on page 4 of this budget brief and page 2 of the administration’s multiyear projections.)

Prefunding Retiree Health Benefits. The Legislature and Governor have agreed to implement the state’s plan to address retiree health benefit liabilities with (1) employer (state) and employee contributions to prefund these benefits and (2) a reduction in the benefits earned by future employees. Through the collective bargaining process, the state has implemented this plan for most state employees. Consistent with actions in the last two budget packages, the Legislature and Governor have agreed to use Proposition 2 debt payments to pay the employer costs of prefunding these benefits.

Transportation-Related Special Fund Loans. As one of the many actions taken in the 2000s to address its budget problems, the state loaned amounts to the General Fund from other state accounts known as special funds. These funds included certain transportation-related accounts. Current state law provides for the repayment of transportation-related loans over the next few years. The Legislature and Governor have agreed to use Proposition 2 debt payments to repay these loans and, in the case of one major loan, this agreement is reflected in statute.

Repaying CalPERS Borrowing Plan. In the 2017‑18 budget package, the Legislature approved a plan to make a $6 billion supplemental payment to CalPERS using a loan from the Pooled Money Investment Account. The administration has proposed using Proposition 2 debt payments to repay the General Fund’s share of the principal and interest on this loan (which the administration currently estimates is $3.4 billion). The Legislature approved this proposal for 2017‑18 and has not raised objections to the administration’s repayment plan. The administration’s apparent goal—stated in a September report to the Joint Legislative Budget Committee—is to maximize savings by paying off the CalPERS loan by the mid-2020s. Paying this loan faster is desirable as it would likely yield more savings over the lifetime of the loan.

Other Recent Uses of Debt Payments. Below, we describe three additional recent uses of Proposition 2 debt payments, which are either more flexible or are not expected to continue. They are:

-

Other Special Fund Loans. In addition to the transportation-related loans, which have statutory repayment deadlines, the state has used Proposition 2 debt payment funds to repay other special fund loans. In general, there is some flexibility as to when these loans are repaid.

-

Paying Down Settle Up. The state owes “settle up” to schools and community colleges when the formula-driven minimum funding level for K-14 education ends up larger than the amount initially included in the budget. Settle-up obligations incurred before July 1, 2014 are eligible for repayment under Proposition 2. Although the state has not established a statutory schedule for paying its settle-up obligations, it has allocated some Proposition 2 debt funding for this purpose each year since 2015‑16. Some of these payments have been part of the adopted budget plan for the year, whereas others have resulted from midyear actions to reclassify K-14 funding that exceeds the minimum requirement.

-

Supplementing UC Retirement Liability Payments. Under a three-year plan, the UC Regents agreed to limit the amount of future employee salaries that may count toward UC employees’ pension benefits and received additional General Fund payments to reduce their unfunded liabilities. These additional General Fund payments have been counted toward Proposition 2. The 2017‑18 budget paid the last installment of the funds in this agreement.

Estimates of Future Proposition 2 Debt Funding

No Added Debt Funding Requirements in 2017‑18. Our estimates of General Fund revenues and capital gains suggest the state underestimated 2017‑18 Proposition 2 requirements by $1.4 billion. Under the measure’s provisions, the state would need to make a true up deposit of that amount to the state’s rainy day fund. These estimates depend on our assumption that revenue collections in the current month (December) and in early 2018 (particularly January and April) will surge, consistent with strong stock market gains over the last year. When capital gains revenues are higher (or lower) than anticipated, the state adjusts reserve levels, but not debt payment amounts. As a result, these estimates do not result in higher debt payments in 2017‑18. (In general, if the budget consistently underestimates Proposition 2 requirements, it would result in more reserve deposits, and fewer debt payments, than more accurate projections would yield.)

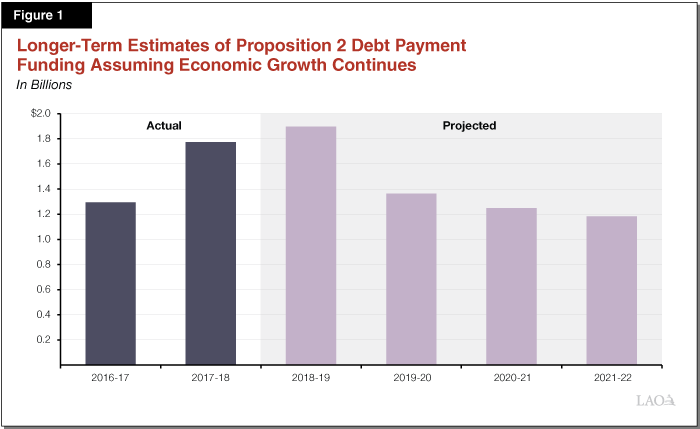

Debt Funding in 2018‑19 and Later. Under our office’s revenue estimates in the Fiscal Outlook, we estimate debt funding will be $1.9 billion in 2018‑19. As shown in Figure 1, these estimates are higher than recent debt funding amounts. When the Governor’s budget is released in January, the administration will provide its own updated estimates of these amounts. Assuming employment and personal income continue to grow, but that the stock market remains mostly flat, Proposition 2 debt payment funding would be around $1.2 billion each year after 2018‑19. (Debt payments and reserve deposits are equal to one another in initial estimates.)

Debt Funding Lower in Recession Scenario. In a recession, the state is able to suspend rainy day fund deposits under certain conditions, but debt payments cannot be reduced. However, in a recession excess capital gains likely will be low or zero and Proposition 2 debt funding only results from the calculation’s base amount. In our Fiscal Outlook estimates, under a recession scenario, Proposition 2 debt payment funding would be about $400 million lower in each 2019‑20 and 2020‑21 and $250 million lower in 2021‑22.

Future Proposition 2 Debt Commitments

Existing Commitments for Funding Total About $1 Billion Annually. As noted above, the Legislature and Governor have reached agreements in recent years on certain uses of Proposition 2 debt funding. Based on these past agreements (which are largely reflected in the administration’s multiyear debt and liabilities estimates) we estimate the following costs:

Prefunding retiree health benefits will continue to rise, reaching about $230 million by 2021‑22 (according to our estimates) and growing with inflation thereafter.

Paying off transportation-related special fund loans will reach nearly $700 million in 2019‑20, but under current law should be fully repaid before 2021‑22.

Repaying the CalPERS borrowing plan by the mid-2020s, costs which are flexible but would require payments on average of at least a few hundred million dollars each year. Under the administration’s current plan, these repayments would be lower in the near-term but rise after transportation-related loans are repaid.

Repaying additional special fund loans and settle up, which have more flexible repayments schedules, would also require hundreds of millions of dollars until the mid-2020s.

Together, these existing commitments would total more than $1 billion annually over the next few years.

Existing Debt Payment Priorities May Use All Funding Until Mid-2020s. Under our estimates, Proposition 2 funding amounts would be around $1.2 billion each year, assuming the economy continues to grow. As such, the $1 billion in commitments described above would consume the vast majority of Proposition 2 debt payment funds—at least in years when stock market growth is at or below average. By the mid-2020s, assuming special fund loans and the CalPERS borrowing plan are fully repaid, there could be some additional capacity for new Proposition 2 funding commitments. Thereafter, until Proposition 2’s debt payment provisions expire in 2030‑31, the state might have some additional capacity for new commitments.

Significant Stock Market Gains Could Result in Temporary Capacity. The projection shown in Figure 1 assumes relatively flat stock market growth in our multiyear projections. As a result, these estimates do not anticipate large, but temporary, increases in Proposition 2 debt funding that could occur if the stock market experiences significant growth. For example, if our estimates of capital gains and Proposition 2 debt funding come to pass in the June 2018 budget package for 2018‑19 (or if there were stock market gains in any other future year), the state could have hundreds of millions of dollars in additional debt funding in that year. These additional funding amounts could be used to pay more toward any eligible Proposition 2 debts on a one-time or short-term basis.

Less Funding Available in a Recession. The projection shown in Figure 1 also assumes the economy continues to grow, producing positive revenue growth in each year. If this does not occur, for example in the case of a recession, debt funding would be lower than what we have shown here. In fact, under the estimates provided earlier, debt funding requirements would be lower than the currently planned repayments. The state would either have to reduce repayments or use other General Fund resources to keep repayments the same. This could push repayments of more flexible items—such as settle up, the CalPERS borrowing plan, or special fund loan repayments—to later years, reducing the capacity for new commitments after the mid-2020s.

LAO Bottom Line

Our analysis of existing Proposition 2 commitments by the Legislature and Governor suggests that, under the existing set of agreements for Proposition 2 debt funding priorities, there may be little ongoing capacity for additional debt funding commitments from this source until at least the mid-2020s. Put another way, there may be little capacity for Proposition 2 to make a major ongoing contribution to paying down an additional category of debt, such as CalSTRS’ liabilities, until that point in time. In order to use Proposition 2 to make a major ongoing contribution to paying down a different category of debt prior to the mid-2020s, the Legislature probably would have to deprioritize one of the debt funding priorities already slated for future Proposition 2 funding. The Legislature could use one-time surges in Proposition 2 debt funding, if any emerge, to provide one-time payments to pay down additional types of debt. Moreover, the Legislature would always have the option to use other General Fund resources to pay more toward debt retirement than Proposition 2 requires.