November 16, 2016

The 2017-18 Budget

California’s Fiscal Outlook

Executive Summary

In this report, we describe our office’s assessment of the condition of the California economy and budget over the 2016–17 through 2020–21 period.

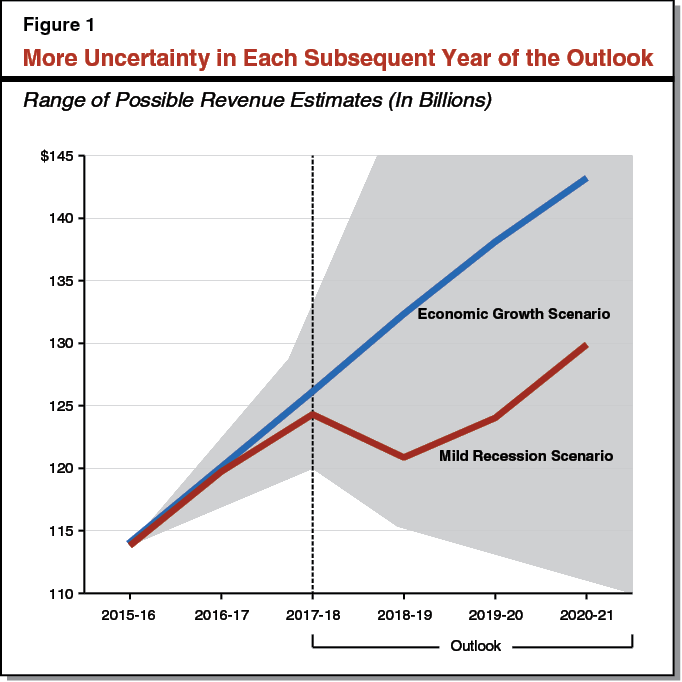

Outlook Subject to Considerable Uncertainty. The condition of the state’s budget depends on many volatile and unpredictable economic conditions, including fluctuations in the stock market. Even in the short term, these conditions cannot be predicted with precision. They are even more difficult to anticipate years in the future. As such, while we have reasonable confidence in our expectations about the economy’s performance in 2017–18, we are much less able to anticipate the economic future in each year thereafter. To reflect these uncertainties, this report emphasizes one estimate of the near–term budget condition through 2017–18 and displays two different estimates of the budget’s condition in 2018–19 through 2020–21.

Positive 2017–18 Budget Outlook. For the near term, under our current economic projections and assuming the state makes no additional budget commitments, we estimate the state would end the 2017–18 fiscal year with $11.5 billion in total reserves. This total includes $2.8 billion in discretionary reserves, which the Legislature can appropriate for any purpose, and $8.7 billion in required reserves, which will be available for a future budget emergency. These reserve levels reflect the continued progress California has made in improving its budget situation.

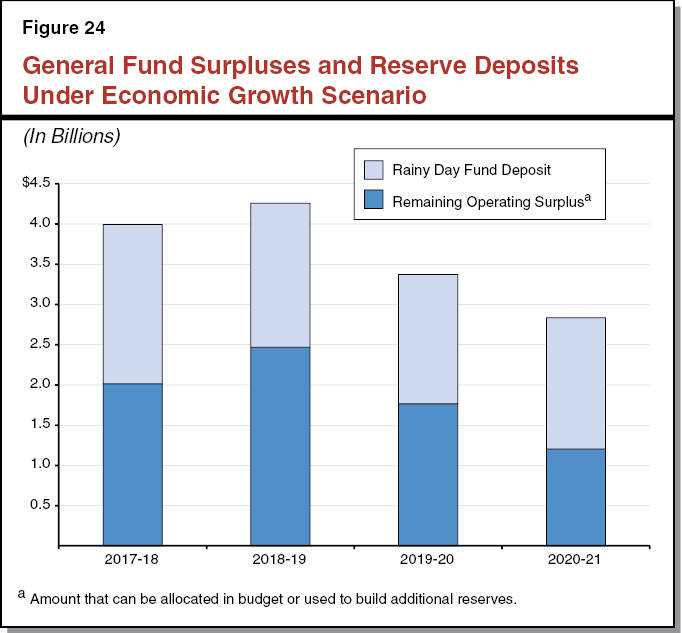

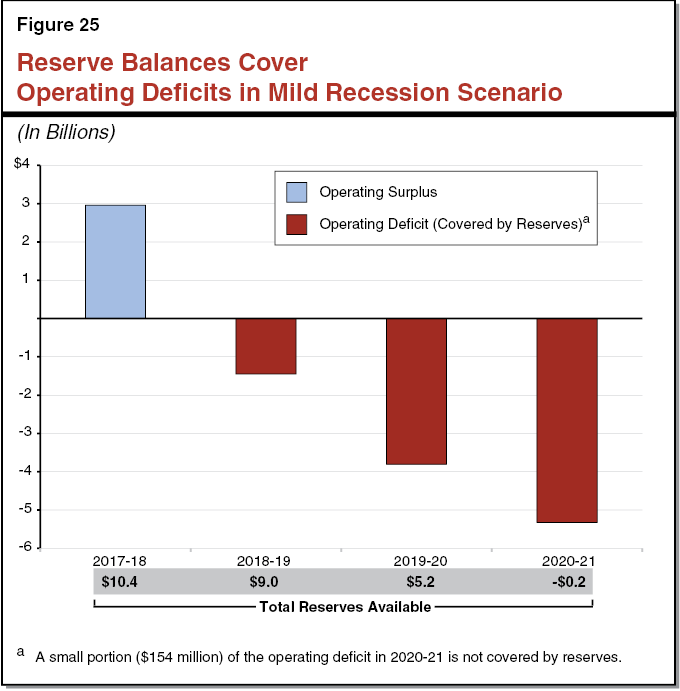

State Is Increasingly Prepared to Weather a Mild Recession. For the longer term, we estimate the condition of the state budget under two different economic scenarios. They are: (1) an economic growth scenario, which assumes the economy continues to grow, and (2) a mild recession scenario, which assumes the state experiences a mild economic downturn beginning in the middle of 2018. Under the growth scenario, we estimate the budget remains in surplus over the outlook period. Under the recession scenario, we find that the state would have enough reserves to cover almost all of its operating deficits through 2020–21. This means, under our assumptions, the state could weather a mild recession without cutting spending or raising taxes through 2020–21.

New Commitments or Policy Changes Would Affect Outlook. Importantly, these estimates assume the state does not make any changes in any year during the outlook period to its current policies and programs. In addition, the outlook also assumes no new changes in federal policy, even though the recent election results suggest some such changes are now likely. Any such state or federal policy changes could have a significant impact on the state’s “bottom line.”

Introduction

Each year, our office publishes the Fiscal Outlook in anticipation of the upcoming 2017–18 budget process. In this report, we summarize our office’s assessment of the condition of the California economy and budget for the upcoming fiscal year (2017–18) as well as the following three years (through 2020–2021). Below, we explain the organization of this report and the basis for our projections.

Organization of This Report

Uncertainty in the Outlook. As this report is published, the first day of the 2017–18 fiscal year is over seven months away. Our expectations about the budget’s condition over the forecast period depend, in large part, on our assumptions about trends in the economy and the stock market. While there is uncertainty over these assumptions in the near term, that uncertainty becomes even greater in each subsequent year. As such, we have reasonable confidence in our expectations about the economy’s performance in 2017–18, but we are much less able to anticipate the economic future in each year thereafter. Figure 1 illustrates this point with regard to General Fund revenues. The figure shows our revenue outlook for the near term, and our two separate revenue outlooks for the out–years, based on two different economic scenarios (described further below). The shaded area in the figure illustrates the uncertainty around these two scenarios. Through 2017–18, revenues could be a few billion dollars above or below our estimates. After 2017–18, revenues could be many billions of dollars above or below our illustrative scenarios, with uncertainty growing in each subsequent year.

This report is organized to reflect our uncertainty about our projections while still producing what we hope is a useful planning document for the Legislature. As such, we emphasize the near–term economic and budget outlook in Chapters 1 through 3 and present out–year budget and economic scenarios in Chapter 4. This organization is discussed in greater detail below.

Chapters 1 and 2 Present One Near–Term Scenario. In Chapter 1 of this report, we present our assessment of the condition of the state General Fund for 2015–16, 2016–17, and 2017–18. Chapter 2, similarly, discusses our estimates of key revenue trends and economic performance through 2017–18. All of our projections through 2017–18 are based on a consensus economic forecast (developed before the election). In these years, there is less uncertainty regarding our assumptions. Also, we hope that presenting one scenario will better assist the Legislature as it plans for the upcoming 2017–18 budget process. However, our estimates of revenues, expenditures, and reserve requirements will change in the following months—especially after the large influx of 2016 tax return payments in April 2017.

Chapter 3 Presents Outlook for State Spending. In Chapter 3 of this report, we discuss our state General Fund spending outlook, again emphasizing the near term. We also comment on key spending trends over the entire outlook period. Generally, these out–year trends are based on our economic growth scenario. The spending estimates aim to reflect the cost of maintaining the state’s existing program commitments and budget act policies over the outlook period. (As such, we have generally provided adjustments to address the impact of inflation with the aim of maintaining the purchasing power of current legislative commitments.) Our estimates also assume the state makes no changes to its programs and policies in the future. This does not mean, however, we believe these policies will or should stay the same. On the contrary, the essence of budgeting is making year–to–year adjustments to spending to accommodate legislative priorities.

Chapter 4 Presents Two Out–year Scenarios. In Chapter 4, we present two estimates of the state’s General Fund condition in 2018–19 through 2020–21. These estimates are based on two different examples of how the economy could perform over the outlook period. They are: (1) an economic growth scenario, which assumes the economy continues to grow throughout the outlook period, and (2) a mild recession scenario, which assumes an economic downturn—with a big stock market decline—begins in the middle of calendar year 2018. These alternate scenarios are only two of many possible future economic realities. Actual experience could be more positive than the growth scenario or more negative than the mild recession scenario.

How We Build Our Outlook

Three Main Outlook Techniques for Spending. In broad terms, we use three different methodologies to build our spending outlook in Chapter 3. They are:

- Formula–Driven Outlooks. These programs have constitutionally required minimum funding levels based on formulas with specified inputs. These include the formulas for determining schools and community college funding (Proposition 98) and reserve deposits and debt payments (Proposition 2).

- Outlooks Based on Caseload, Utilization, and Price. These programs experience changes in funding levels based on a combination of changes in their number of participants (caseload), the intensity at which participants use services (utilization), and the costs per enrollee (price). Examples include Medi–Cal, the state’s insurance program for low–income Californians, and the California Department of Corrections and Rehabilitation, which operates the state’s correctional facilities and parole system. The outlook for these programs use models that identify relationships between economic and demographic trends and spending levels.

- Discretionary Outlooks. These programs have funding levels that are generally determined by legislative priorities. We typically assume a continuation of recent budget practices—for example, funding for universities and employee salaries and health benefits.

Revenues Depend on Volatile Economic Indicators. Our revenue outlook depends, in large part, on our assumptions about the performance of the economy and the stock market. In particular, revenues from the personal income tax, which make up about 70 percent of General Fund revenues, depend on highly volatile estimates of capital gains. As a result, ordinary movement in the stock market—over just a period of weeks or months—can result in billions of dollars in higher or lower revenues for the state. Our revenue estimates also assume current laws and policies stay in place—both at the state and federal levels. For example, our outlook assumes the tax on managed care organizations will expire at the end of 2018–19, consistent with current law. Similarly, our estimates of growth in the sales and use tax reflects a quarter–cent reduction in the tax rate after December 2016 as that provision of Proposition 30 (2012) expires.

Effects of November 2016 Voter Initiatives Included. Our fiscal outlook reflects the fiscal effects of propositions approved by the voters on the November 8, 2016 ballot. (We have assumed that Proposition 66, which deals with the death penalty processes, is approved, although votes are still being counted.)

Chapter 1: General Fund Through 2017–18

This chapter summarizes our office’s assessment of the near–term condition of the state General Fund, the state’s main operating account.

Outlook for the 2017–18 Budget

Figure 2 displays our estimate of the General Fund condition through 2017–18. We estimate that 2016–17 will end with $7.5 billion in total reserves, about $1 billion lower than the assumptions in the budget act. Assuming no new commitments are made in the 2017–18 budget, we estimate total reserves will grow to $11.5 billion at the end of the fiscal year—an increase of $4 billion. This $11.5 billion total includes $2.8 billion in the Special Fund for Economic Uncertainties (SFEU), the state’s discretionary budget reserve, and $8.7 billion in the Budget Stabilization Account (BSA), the state’s required budget reserve.

Figure 2

LAO General Fund Condition

(In Millions)

|

2015–16 |

2016–17 |

2017–18 |

|

|

Prior–year fund balance |

$2,935 |

$3,715 |

$1,717 |

|

Revenues and transfers |

115,643 |

119,991 |

128,123 |

|

Expenditures |

114,863 |

121,988 |

126,109 |

|

Ending fund balance |

$3,715 |

$1,717 |

$3,731 |

|

Encumbrances |

966 |

966 |

966 |

|

SFEU balance |

2,749 |

751 |

2,765 |

|

Reserves |

|||

|

SFEU balance |

$2,749 |

$751 |

$2,765 |

|

BSA balance |

3,420 |

6,714 |

8,694 |

|

Total Reserves |

$6,169 |

$7,466 |

$11,459 |

|

SFEU = Special Fund for Economic Uncertainties (the General Fund’s discretionary budget reserve) and BSA = Budget Stabilization Account. |

|||

2016–17: Revised Reserve Levels of $7.5 Billion

The estimated $1 billion decrease in 2016–17 reserves is the net result of the following:

- $510 Million Downward Revision to Entering Fund Balance. We include two revisions to the budget condition before 2015–16 that affect the current budget situation. First, based on our estimates of required funding for schools and community colleges, we assume the state will pay an additional $351 million in “settle up” payments related to earlier minimum funding guarantees. (We discuss these settle up payments further in Chapter 3.) Second, our estimate reflects a $159 million reduction in prior years’ estimated revenue collections and accruals.

- Revenues Lower by $1.7 Billion in 2015–16 and 2016–17. Between 2015–16 and 2016–17, we estimate revenues will be lower than the budget act estimates by $1.7 billion. In particular, our estimates for total revenues—across the two fiscal years—associated with the sales and use tax (SUT) and corporation tax (CT) are $2.6 billion lower than budget act assumptions. These shortfalls, however, are partially offset by net upward revisions in our estimate of personal income tax (PIT) revenues over the two fiscal years—$923 million below budget estimates in 2015–16 and $1.7 billion above estimates in 2016–17.

- Expenditures Lower by $1.2 Billion in 2015–16 and 2016–17. We estimate expenditures in 2015–16 and 2016–17 will be lower than budget act assumptions by a net $1.2 billion. Two factors explain most of the lower spending. First, General Fund Proposition 98 spending declines by $640 million in 2015–16, due to lower state revenues and higher local property taxes. Second, in 2016–17, we assume the $400 million set–aside for affordable housing in the budget package is not spent because it was contingent on changes in state law that did not occur.

- Required BSA Deposits Unchanged. Proposition 2 establishes a minimum amount that the state must deposit each year into the BSA, the state’s required budget reserve. Under the measure’s “true up” provisions, the state revisits these estimates twice: once in each of the two subsequent budgets. However, the 2016–17 budget package set aside a $2 billion optional deposit and specified that these funds would be used to meet true up requirements for 2015–16 and 2016–17. The estimated true up deposits associated with 2015–16 and 2016–17 are together less than $2 billion. As a result, we assume no additional true ups are made, leaving the already revised 2015–16 deposit and initial 2016–17 deposits unchanged.

2017–18 Outlook: Year Ends With $11.5 Billion Reserve

Revenues and Transfers Grow $8.1 Billion. We estimate that revenues and transfers will grow by $8.1 billion in 2017–18, including a $6.4 billion (5.4 percent) increase in the “Big Three” revenues: the PIT, SUT, and CT. Most of this growth is driven by a 6.9 percent year–over–year increase in the PIT.

Spending Grows $4.1 Billion. We estimate that General Fund expenditures—absent any new program commitments—would grow $4.1 billion between 2016–17 and 2017–18. This increase is in part attributable to a $1.4 billion increase in the General Fund share of the minimum funding guarantee for schools and community colleges. Another $1.5 billion is attributable to the net increase in spending related to health and human services programs, including about an $800 million increase in Medi–Cal, the state’s health insurance program for low–income Californians. Various other spending items grow too. In contrast, spending declines between 2016–17 and 2017–18 due to the expiration of many one–time expenditures in the 2016–17 budget. These items include, for example, one–time spending on deferred maintenance, capital outlay, and several criminal justice programs.

Reserves Grow to $11.5 Billion. Based on our current estimates of revenues, particularly those related to capital gains, we estimate the state will be required to make an initial deposit of $2 billion into the BSA for the 2017–18 fiscal year. In addition, based on our estimates that growth in revenues will outpace expenditures, and assuming no new budget commitments are made, we estimate 2017–18 would end with additional reserves of $2 billion in the SFEU. Together, these reserves would build on the $7.5 billion balance estimated in 2016–17, bringing total reserves to $11.5 billion by the end of 2017–18.

LAO Comments

Positive 2017–18 Budget Outlook. Based on our current economic and budget projections, we estimate the General Fund will end 2017–18 with $11.5 billion in total reserves, including $2.8 billion in discretionary reserves. (That $2.8 billion amount is displayed in our figures as the balance in the SFEU.) These reserve levels reflect the continued progress California has made in improving its budget situation. The state budget remains on steady footing.

Lower 2017–18 Revenue Estimates Would Mean Fewer Discretionary Resources. Our revenue outlook is based, in part, on assumptions about the stock market. As we describe in Chapter 2, this outlook makes certain assumptions about how estimated and final PIT payments will strengthen during the second half of 2016–17. We believe these assumptions are reasonable, but if they do not come to pass, our revenue estimates easily could be about $2 billion lower in both 2016–17 and 2017–18. In this case, 2017–18 would end with over $2 billion less in discretionary reserves. (The $4 billion revenue decline over the two fiscal years would be offset by lower Proposition 98 and Proposition 2 requirements.) In this scenario, the Legislature would have significantly fewer discretionary resources in the 2017–18 budget process.

Outlook for Future Shapes Decisions Today. Under our current estimates, the Legislature will face decisions in the 2017–18 budget process about how to allocate the $2.8 billion in discretionary reserves. The Legislature could opt to hold some or all of this in reserves or make some new one–time or ongoing commitments. The choices the Legislature makes for these funds may depend, in large part, on its consideration of the future prospects for the state budget. We present two possible out–year budget scenarios in Chapter 4 of this report. We hope these scenarios help inform the Legislature’s decisions as the 2017–18 budget process begins.

Chapter 2: The Economy and Revenues

The Economy

Our near–term projections are based on a consensus of economists about the likely trend of the U.S. economy through 2018, as reported in October (prior to the election) by Moody’s Analytics, a national economics consulting firm. This differs from our most recent projections, which were premised on the analyses of just the economists at Moody’s Analytics. (The administration’s projections are based on analyses by a different firm.) Using these consensus views about the U.S. economy, our office develops a California–specific macroeconomic scenario.

Our near–term economic projections are summarized in Figure 3 and compared to the administration’s May 2016 projections—the underlying basis for the revenue estimates in the 2016–17 state budget—in Figure 4. Our near–term projections reflect the consensus view that the economic expansion is likely to continue in the U.S. over at least the next couple of years. This, however, is not a certainty. The possibility exists that a slowdown or recession could emerge in the short term. In addition, the October consensus of economists does not reflect federal policy and budget changes that may result from this month’s election of a new President and a new Congress.

Figure 3

LAO Economic Assumptions Through 2018

Percent Change Unless Otherwise Noted

|

United States |

2015 |

2016 |

2017 |

2018 |

|

Real gross domestic product |

2.6% |

1.6% |

2.3% |

2.2% |

|

Personal income |

4.4 |

3.3 |

4.3 |

4.8 |

|

Wage and salary employment |

2.1 |

1.7 |

1.1 |

0.8 |

|

Unemployment rate (percent) |

5.3 |

4.9 |

4.6 |

4.6 |

|

Consumer price index |

0.1 |

1.1 |

2.3 |

2.2 |

|

Core Personal Consumption Expenditures price index |

1.4 |

1.6 |

2.0 |

1.6 |

|

Federal funds rate (percent) |

0.1 |

0.4 |

1.0 |

1.9 |

|

Housing permits (thousands) |

1,178 |

1,158 |

1,294 |

1,366 |

|

S&P 500 (annual average) |

2,061 |

2,078 |

2,165 |

2,231 |

|

California |

2015 |

2016 |

2017 |

2018 |

|

Personal income |

6.4% |

3.9% |

5.0% |

5.6% |

|

Wage and salary employment |

3.0 |

2.6 |

1.9 |

1.6 |

|

Unemployment rate (percent) |

6.2 |

5.4 |

5.3 |

5.2 |

|

Consumer price index |

1.5 |

2.3 |

2.8 |

2.7 |

|

Housing permits (thousands) |

98 |

96 |

98 |

100 |

|

Single–unit permits |

45 |

47 |

50 |

52 |

|

Multifamily permits |

53 |

49 |

48 |

48 |

|

Population growth |

1.0 |

1.0 |

0.9 |

0.9 |

|

Note: Based generally on Moody’s Analytics’ October 2016 U.S. macroeconomic “consensus scenario,” a scenario that incorporates the central tendency of a range of baseline projections from various institutions and professional economists. S&P 500 index levels, however, are lowered from those assumed in the Moody’s Analytics’ consensus scenario. The California–specific assumptions above reflect a California state macroeconomic scenario developed by the LAO based on the U.S. consensus scenario. |

||||

Figure 4

Comparison to 2016–17 Budget Acta Economic Assumptions

Percent Change Unless Otherwise Noted

|

2016 |

2017 |

2018 |

||||||

|

Budget Act June 2016 |

LAO Nov. 2016 |

Budget Act June 2016 |

LAO Nov. 2016 |

Budget Act June 2016 |

LAO Nov. 2016 |

|||

|

United States |

||||||||

|

Real gross domestic product |

2.1% |

1.6% |

2.8% |

2.3% |

2.7% |

2.2% |

||

|

Personal income |

3.9 |

3.3 |

4.9 |

4.3 |

5.1 |

4.8 |

||

|

Wage and salary employment |

1.9 |

1.7 |

1.4 |

1.1 |

0.9 |

0.8 |

||

|

Unemployment rate (percent) |

4.8 |

4.9 |

4.7 |

4.6 |

4.7 |

4.6 |

||

|

Consumer price index |

1.0 |

1.1 |

2.2 |

2.3 |

2.0 |

2.2 |

||

|

Federal funds rate (percent) |

0.6 |

0.4 |

1.4 |

1.0 |

2.4 |

1.9 |

||

|

S&P 500 (annual average) |

2,075 |

2,078 |

2,117 |

2,165 |

2,160 |

2,231 |

||

|

California |

||||||||

|

Personal income |

5.5% |

3.9% |

5.3% |

5.0% |

4.5% |

5.6% |

||

|

Wage and salary employment |

2.1 |

2.6 |

1.7 |

1.9 |

1.1 |

1.6 |

||

|

Unemployment rate (percent) |

5.3 |

5.4 |

5.2 |

5.3 |

5.1 |

5.2 |

||

|

Consumer price index |

2.2 |

2.3 |

2.8 |

2.8 |

2.6 |

2.7 |

||

|

Housing permits (thousands) |

107 |

96 |

126 |

98 |

142 |

100 |

||

|

Single–unit permits |

51 |

47 |

62 |

50 |

71 |

52 |

||

|

Multifamily permits |

55 |

49 |

64 |

48 |

71 |

48 |

||

|

Population growth |

0.9 |

1.0 |

0.9 |

0.9 |

0.9 |

0.9 |

||

|

aThe 2016–17 Budget Act reflected the administration’s May 2016 revenue assumptions, this figure, therefore, describes the administration’s May 2016 economic assumptions as those reflected in the 2016–17 Budget Act, which was passed in June 2016. |

||||||||

The U.S. Economy

Long Economic Expansion Continues. The national economy has been expanding since the end of the last recession in June 2009. This month marks the 89th month of the expansion, which makes it the fourth–longest in the U.S. since at least 1854, as shown in Figure 5. Early next year, if the expansion continues, it will surpass the expansion of the 1980s to become the third longest in U.S. history.

Figure 5

Current Economic Expansion Already Among Longest in U.S. History

Data Since 1854

|

Economic Expansion |

Number of Months |

|

April 1991 to March 2001 |

120 |

|

March 1961 to December 1969 |

106 |

|

December 1982 to July 1990 |

92 |

|

July 2009 to present |

89 (so far) |

|

July 1938 to February 1945 |

80 |

|

December 2001 to December 2007 |

73 |

|

April 1975 to January 1980 |

58 |

|

April 1933 to May 1937 |

50 |

|

Average Economic Expansion, 1945 to 2009 |

58 |

|

Source: National Bureau of Economic Research. |

|

Economic expansions do not die of old age. (Australia, for example, just marked 25 years of its current expansion—now the longest in the developed world.) Instead, expansions commonly end because of imbalances that build up and “overheat” the economy. Economic shocks and major changes in the economy or public policy also can depress activity enough to end an expansion. While policy makers should note this expansion’s age, they also should be aware that economic expansions have been getting longer. The last three lasted an average of 95 months—longer than the 58–month average for expansions since 1945. Improved management of U.S. monetary policy and other government policies have been credited with a reduction in macroeconomic volatility over time. Also credited are better management by businesses of inventories, the rise of the relatively stable service sector, and technological change.

When Will the Expansion End? Economists and other forecasters (including us) are not good at projecting the end of expansions far in advance. (That is one reason why—later in this publication—we consider one scenario of what could happen to the state budget if a mild recession hits around 18 months from now.) History provides us with a few instructive lessons to foreshadow the demise of the current expansion. The past few U.S. expansions have ended about three years after the economy reached what is considered “full employment.” Once an economy reaches that point, wages and inflation may accelerate, necessitating tighter monetary policy (including higher interest rates). The U.S. unemployment rate has been at or below 5 percent—a commonly estimated level of full employment—since last October. If the experience of the past few expansions repeated itself, the current expansion would continue over the next couple of years.

Some economists, however, have been saying that the lack of robust wage growth, among other factors, suggests that full employment currently requires an even lower unemployment rate. That reasoning would be consistent with an expansion that continued for an even longer period of time. We note, however, that wage growth recently has picked up somewhat. A related uncertainty is how much “slack” remains in the labor market—as in, how many more people not currently seeking work will return to the labor force in the coming years. Labor market slack can help prolong the expansion by preventing the economy from overheating.

The California Economy

California’s economy has grown at a good pace in recent years. Different groups and regions have shared in that growth to varying degrees.

Incomes Up. According to the Census Bureau’s American Community Survey (ACS), median household income in California rose 4 percent in 2015—slightly outpacing the nationwide growth rate of 3.8 percent. California’s $64,500 median household income ranked 9th among the 50 states. With 6.2 percent growth in 2015, median household incomes reported in the ACS data for the San Francisco–Oakland metro region was surpassed, among the nation’s large metro areas, only by Atlanta’s 7.1 percent growth. Median household incomes grew by 3.3 percent in the Los Angeles–Orange County region, 2.6 percent in the Inland Empire (Riverside and San Bernardino Counties), and 1.6 percent in San Diego County. (We note, however, that these ACS results have a relatively high margin of error for San Francisco–Oakland, San Diego, and the Inland Empire.)

Official Poverty Rate Down. According to ACS data, the official poverty rate in California fell from 16.4 percent in 2014 to 15.3 percent in 2015, representing about 370,000 fewer Californians counted under this poverty measure. While this official poverty measure (OPM) is just above the national average, California’s high housing costs mean that its “supplemental poverty measure” (SPM)—which accounts for forms of public assistance not included in the OPM and adjusts poverty thresholds for housing costs and other factors—is much higher than the rest of the country’s. Based on data from 2013 through 2015, California’s SPM is 20.6 percent—versus 14.4 percent for the rest of the country.

Job Growth Has Been Outpacing the Nation. In September, the number of payroll jobs in California was up by about 380,000 over the prior year, a growth rate of 2.3 percent—better than the 1.7 percent job growth rate for the nation as a whole. California’s job growth rate over the past year ranks 14th best among the 50 states. Among the state’s major employment sectors, professional and technical services jobs (many of them in technology) are up 4.6 percent over the past year, and construction jobs are up 4.2 percent. Oil and gas jobs, which account for only a small fraction of the state total but are very important in some areas such as Kern County, are down 12.5 percent over the past 12 months, but losses have slowed with more stable energy prices recently.

While California’s official unemployment rate—5.5 percent as of September—remains tied for 10th worst with three other states, it has dropped half a percentage point in the last year and 6.7 percentage points from its high point in October 2010. In Los Angeles County, the seasonally adjusted jobless rate was 5 percent in September 2016—down 1.2 percentage points from one year before. In September, unadjusted unemployment rates in the state ranged from just 3.1 percent in San Mateo County to 22.7 percent in Imperial County (among the nation’s highest local unemployment rates). Imperial County’s September unemployment rate was down 2.3 percentage points from one year before. Other rural and agricultural areas continue to have high unemployment rates.

Other Labor Market Improvements. By many measures, California’s labor market has been heating up:

- Participation Up. Even as more and more baby boomers reach retirement age, California’s labor force participation rate—those participating in the labor force as a percentage of the population aged 16 and older—grew from 62 percent in September 2015 to 62.6 percent in September 2016 (its highest level in over two years), according to U.S. and state labor surveys. On a seasonally adjusted basis, the number of those participating in the labor force grew by 380,000 statewide (an increase of 2 percent) over the past year, including 131,000 in Los Angeles County (an increase of 2.6 percent there). Those choosing not to be in the labor force because they were discouraged over their job prospects dropped more than 10 percent over the last 12 months to just 68,000 statewide—down from over 175,000 in early 2011.

- Full–Time Work Up. According to Current Population Survey data, almost all of the net growth in California jobs over the past year has been in full–time positions, as the percent of those employed working full–time in the state grew from 80.3 percent a year ago to 80.6 percent now. Between September 2015 and September 2016, the three–month moving average of private–sector hourly earnings grew by more than 3 percent. The number of those working part–time for economic reasons (generally because there is insufficient demand from their employer) dropped 11 percent over the past year to 946,000—down from over 1.5 million in 2010.

- Jobless Claims and Underemployment Down. Initial jobless claims have fallen to near prerecession levels—under 40,000 per week in some periods this year. California’s “U–6” jobless rate—a broader jobless measure that counts those unemployed, marginally attached to the labor force, and working part–time for economic reasons—fell to 11.6 percent in September (down 1.7 percentage points from one year before). This remains high compared to the rest of the nation, but California’s U–6 rate is far below its 22.1 percent annual peak in 2010.

LAO Projections for 2016 Through 2018. As shown in Figures 3 and 4, our office anticipates that personal income in California will grow a modest 3.9 percent in 2016—faster than the 3.3 percent growth rate expected for the U.S. as a whole. While the 3.9 percent growth rate is disappointing, we note that wages and salaries—the largest component by far of personal income subject to state taxation—are expected to grow by 5.2 percent, which is consistent with the fairly strong trend of personal income tax (PIT) withholding growth we have been seeing this year. The anticipated wage and salary growth in 2016 offsets weak growth in some other personal income categories like dividends, interest, and rent and transfers (such as Social Security payments), some parts of which are not subject to the state income tax. Our current projections anticipate stronger personal income and wage growth in 2017 and 2018, as California’s unemployment rate dips below 5 percent. We anticipate less growth in jobs and more growth in wages over the next few years, as the labor market tightens more and nears full employment. California’s minimum wage also will increase in future years under state law.

The Bay Area

While the Los Angeles area economy is bigger, the Bay Area has contributed disproportionately to state tax revenue and economic growth in recent decades. This continues to be the case today. Because of the Bay Area’s importance to the economy and budget, we focus on it in this section.

Silicon Valley Job Growth. Jobs in the San Jose region (Santa Clara and San Benito Counties) grew by a net 3.6 percent during the 12 months ending in September—far outpacing job growth in the state and its other large metro areas. The bulk of the region’s job growth came in professional and business services—primarily in technology–dominated job categories. Other contributors to Silicon Valley job growth have been private education and health facilities, construction, and restaurants. The San Francisco (San Francisco and San Mateo Counties) and East Bay (Alameda and Contra Costa Counties) regions recorded 2.6 percent year–over–year job growth through September, with noteworthy growth rates in technology, health care, and construction, among other sectors.

Bay Area Contributes Heavily to State Taxes. The state PIT makes up about 70 percent of state General Fund revenues. As shown in Figure 6), Bay Area residents—16.8 percent of the state’s population—receive 29.1 percent of the income reported on state resident tax returns as of 2014 and pay 37 percent of the income taxes assessed. This means that per capita PIT payments by Bay Area residents are far above those of any other region in the state. Among the state’s major regions listed in Figure 6, the Bay Area’s per capita tax payments are almost twice those of Orange County, the next highest area. Below Orange County on the list, all other major regions of the state have per capita PIT payments below the statewide average.

Figure 6

Bay Area Contributes Disproportionately to State Income Tax Revenues

2014 Resident Tax Returns

|

County |

2014 Population |

Adjusted Gross Income |

Personal Income Tax Assessed |

||||||

|

Number (Millions) |

Percent of Statewide Total |

Amount (Billions) |

Percent of Statewide Total |

Amount (Billions) |

Percent of Statewide Total |

Per Capita ($) |

|||

|

San Francisco / Oakland / San Jose MSAs |

6.5 |

16.8% |

$346.2 |

29.1% |

$22.6 |

37.0% |

$3,474 |

||

|

Orange County |

3.1 |

8.1 |

107.3 |

9.0 |

5.7 |

9.3 |

1,821 |

||

|

Ventura County |

0.8 |

2.2 |

26.4 |

2.2 |

1.2 |

2.0 |

1,439 |

||

|

Los Angeles County |

10.1 |

26.1 |

282.9 |

23.8 |

14.5 |

23.7 |

1,434 |

||

|

San Diego County |

3.2 |

8.4 |

97.0 |

8.2 |

4.6 |

7.6 |

1,425 |

||

|

Central Coasta |

1.4 |

3.7 |

39.1 |

3.3 |

1.8 |

3.0 |

1,282 |

||

|

Napa, Solano, and Sonoma Counties |

1.1 |

2.7 |

31.4 |

2.6 |

1.3 |

2.2 |

1,267 |

||

|

Sacramento MSA |

2.2 |

5.8 |

58.8 |

4.9 |

2.4 |

3.9 |

1,063 |

||

|

North Stateb |

1.2 |

3.2 |

22.4 |

1.9 |

0.7 |

1.2 |

612 |

||

|

San Joaquin Valleyc |

4.1 |

10.7 |

72.1 |

6.1 |

2.4 |

4.0 |

593 |

||

|

Riverside and San Bernardino Counties |

4.4 |

11.4 |

81.2 |

6.8 |

2.5 |

4.0 |

559 |

||

|

Other residentsd |

0.4 |

1.0 |

23.5 |

2.0 |

1.3 |

2.1 |

3,498 |

||

|

Totals |

38.7 |

100.0% |

$1,188.2 |

100.0% |

$61.2 |

100.0% |

$1,581e |

||

|

a Includes Monterey, San Luis Obispo, Santa Barbara, and Santa Cruz Counties. b Includes all counties north of San Francisco, Napa, Sonoma, Vallejo–Fairfield, and Sacramento MSAs. c Includes Fresno, Kern, Kings, Madera, Merced, San Joaquin, Stanislaus, and Tulare Counties. d Includes California resident tax returns with (1) an address in another California county or (2) an out–of–state address. Returns with out–of–state addresses collectively had $1.1 billion of tax assessed, the vast majority of the total shown on this line. Excludes nonresident tax returns, which collectively had $2.5 billion of tax assessed. eStatewide average. MSA = metropolitan statistical area. |

|||||||||

The Bay Area contributes so much to PIT because individuals there, on average, have higher incomes than those in other areas of the state. In California’s income tax system, those with higher incomes pay taxes at higher marginal rates. In terms of median adjusted gross income shown on state tax returns, eight of the top ten counties in the state are in the Bay Area. Prior research by our office has shown that Bay Area residents also spend more, on average, on goods subject to the sales tax, compared to other regions of the state. Per capita assessed valuation—for local property taxes—also is higher in the Bay Area than in other areas of the state.

Dependence on the Bay Area. The state’s job growth has been centered in the Bay Area, and its key income, sales, and property taxes are all paid disproportionately by Bay Area residents. Boom times in the Bay Area tend to mean the statewide economy and the state budget are doing well. Economic weakness there hinders the economy and can throw the state budget into a tailspin. With the Bay Area economy dependent on what has been a thriving technology sector, one major risk to the state’s near–term economic health is the possibility of a big slowdown in that sector. While venture capital investments in the Bay Area have fallen from 2014 and 2015 levels, they remain substantial and there is little evidence that a significant slowdown of the Bay Area technology sector is imminent.

Housing Costs a Growing Concern. Home prices and rents remain very high in both the Bay Area and Los Angeles, as well as other parts of the state. Housing affordability is a growing concern in California. Given the importance of the Bay Area to the state budget, as noted above, we focus below on housing affordability issues there.

Over the past year, the San Francisco–Oakland and San Jose metro areas have experienced home price growth of 5.7 percent and 4.7 percent, respectively. This is well below the double–digit growth that occurred in these areas in recent years. Nonetheless, home prices remain high compared to just about anywhere else. Median home prices in the San Jose ($944,000) and San Francisco–Oakland ($813,000) areas ranked first and second highest among major urban areas in the country.

Rents continued to rise quickly in the San Francisco–Oakland (12 percent) and San Jose (13 percent) areas in 2015, according to ACS data. Monthly rents in San Jose ($2,300) and San Francisco–Oakland ($2,000) were rivaled only by those in Honolulu among major urban areas. While there is some anecdotal and survey information showing that rents have stabilized or fallen slightly in 2016, other data sources, such as Zillow’s rental index, show 3 percent to 4 percent growth in rental costs this year in parts of the Bay Area. (ACS data on rents for 2016—which is generally considered to be the most comprehensive—will not be available until next year.)

More residential construction would moderate home price growth over the long term. Building activity in the Bay Area generally has returned to prerecession levels. Building permits in San Francisco–Oakland are at their highest levels since 2006. Despite this recovery, building levels remain low relative to other urban areas throughout the country. Over the past year, the San Francisco–Oakland and San Jose areas approved about 2.8 building permits per 1,000 residents—well below the national average among major urban areas of 3.9 permits per 1,000 residents. Other urban areas with rapidly growing economies—such as Austin, Houston, Portland, and Raleigh—approved over six permits per 1,000 residents during the past year. Over the long term, a constrained supply of new housing may limit prospects for job and economic growth in the Bay Area.

Revenues

Figure 7 displays our office’s revenue outlook through 2017–18. This outlook reflects the U.S. economic projections of an October 2016 consensus of economists, described earlier. (In Chapter 4, we display revenue estimates through 2020–21 under two possible economic scenarios—an economic growth scenario and a recession scenario.)

Figure 7

LAO November 2016 Revenue Outlook

General Fund (Dollars in Millions)

|

2015–16 |

2016–17 |

2017–18 |

Change From 2016–17 |

||

|

Amount |

Percent |

||||

|

Personal income tax |

$79,039 |

$85,085 |

$90,959 |

$5,874 |

6.9% |

|

Sales and use tax |

24,766 |

24,747 |

25,024 |

277 |

1.1 |

|

Corporation tax |

10,032 |

9,892 |

10,162 |

269 |

2.7 |

|

Subtotals, “Big Three” Revenues |

($113,837) |

($119,724) |

($126,144) |

($6,420) |

(5.4%) |

|

Insurance tax |

$2,561 |

$2,376 |

$2,456 |

$80 |

3.4% |

|

Other revenues |

2,219 |

1,779 |

1,650 |

–129 |

–7.3 |

|

BSA transfer |

–1,814 |

–3,294 |

–1,979 |

1,315 |

— |

|

Other transfers |

–1,160 |

–593 |

–148 |

446 |

— |

|

Totals, Revenues and Transfers |

$115,643 |

$119,991 |

$128,123 |

$8,132 |

6.8% |

|

BSA = Budget Stabilization Account. |

|||||

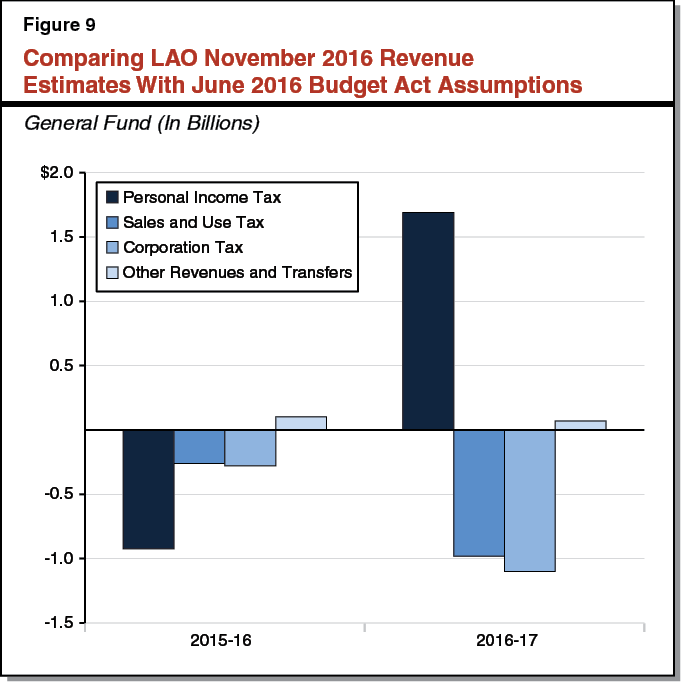

Revenue Estimates $1.7 Billion Below Budget Assumptions for 2015–16 and 2016–17 Combined. Our revenue estimates for 2015–16 and 2016–17 combined are modestly lower than the administration’s May 2016 estimates that served as the basis for the June 2016 budget plan, as shown in Figures 8 and 9. In particular, our estimates of sales and use tax (SUT) and corporation tax (CT) revenues are $2.6 billion below budget act assumptions for 2015–16 and 2016–17 combined. On the other hand, our estimate of PIT revenues is $768 million above budget assumptions for those two fiscal years combined, somewhat offsetting our weak SUT and CT estimates. After accounting for minor revenues and transfers, our bottom line estimates of General Fund revenues and transfers are $1.7 billion below budget assumptions.

Figure 8

Comparing LAO November 2016 Revenue Estimates With June 2016 Budget Act Assumptions

General Fund (In Millions)

|

2015–16 |

2016–17 |

Total Change |

|||||||

|

LAO Nov. 2016 |

Budget Act June 2016 |

Change |

LAO Nov. 2016 |

Budget Act June 2016 |

Change |

||||

|

Personal income tax |

$79,039 |

$79,962 |

–$923 |

$85,085 |

$83,393 |

$1,691 |

$768 |

||

|

Sales and use tax |

24,766 |

25,028 |

–262 |

24,747 |

25,727 |

–980 |

–1,242 |

||

|

Corporation tax |

10,032 |

10,309 |

–277 |

9,892 |

10,992 |

–1,100 |

–1,377 |

||

|

Subtotals, “Big Three” Revenues |

($113,837) |

($115,299) |

(–$1,462) |

($119,724) |

($120,113) |

(–$389) |

(–$1,851) |

||

|

Other revenues and transfers |

$1,806 |

$1,702 |

$104 |

$267 |

$197 |

$70 |

$174 |

||

|

Totals, Revenues and Transfers |

$115,643 |

$117,001 |

–$1,358 |

$119,991 |

$120,310 |

–$319 |

–$1,677 |

||

Strong PIT Growth Drives Healthy Revenue Growth in 2017–18. Looking beyond the current fiscal year, we estimate that the state’s “Big Three” revenues—PIT, SUT, and CT—will grow 5.4 percent in 2017–18, as shown in Figure 7. This growth is driven by a projected 6.9 percent year–over–year increase in the PIT, which makes up about 70 percent of General Fund revenues. We estimate SUT and CT to grow by 1.1 percent and 2.7 percent, respectively, in 2017–18. Year–over–year growth in the SUT would be higher were it not for the end of the quarter–cent Proposition 30 (2012) SUT rate after December 2016. We describe near–term estimates of these tax revenues in more detail below.

Personal Income Tax

June 2016 Cash Receipts Were Disappointing . . . As the Governor signed the 2016–17 Budget Act, PIT cash collections for June came in $888 million below projections, as shown in Figure 10. June is an important revenue collection month as taxpayers submit estimated payments for that year’s tax liability. (Estimated payments are quarterly payments made by individuals and businesses on expected taxable income for which there is no withholding, such as realized capital gains on sales of stocks and other assets.) Estimated payments fell short of projections by $622 million (about 9 percent) in June 2016. Moreover, withholding came in nearly 6 percent, or $250 million, below projections.

Figure 10

Recent PIT Cash Trends Better Than June 2016

(In Millions)

|

June 2016 |

July 2016 Through October 2016 |

||||||

|

Actual |

DOF Projections |

Difference |

Actual |

DOF Projections |

Difference |

||

|

PIT withholding |

$4,138 |

$4,388 |

–$250 |

$17,536 |

$17,464 |

$72 |

|

|

Estimated payments |

6,187 |

6,808 |

–622 |

3,139 |

3,336 |

–198 |

|

|

Other FTB collections |

685 |

618 |

66 |

2,796 |

2,483 |

312 |

|

|

FTB refunds |

–450 |

–351 |

–99 |

–1,741 |

–1,520 |

–221 |

|

|

Proposition 63 allocation |

–186 |

–202 |

16 |

–382 |

–383 |

1 |

|

|

Totals |

$10,373 |

$11,261 |

–$888 |

$21,347 |

$21,381 |

–$34 |

|

|

PIT = personal income tax; DOF = Department of Finance; and FTB = Franchise Tax Board. |

|||||||

. . . But Recent Collections Have Been on Target. Since June 2016, however, cash receipts have largely hit their mark. Withholding and “other Franchise Tax Board collections” (such as final payments) exceeded budget projections by $72 million and $312 million, respectively. Offsetting these results, estimated payments and refunds were worse than projections ($198 million and $221 million, respectively). In total, PIT receipts over the July through October period fell short of projections by just $34 million (or about two–tenths of 1 percent).

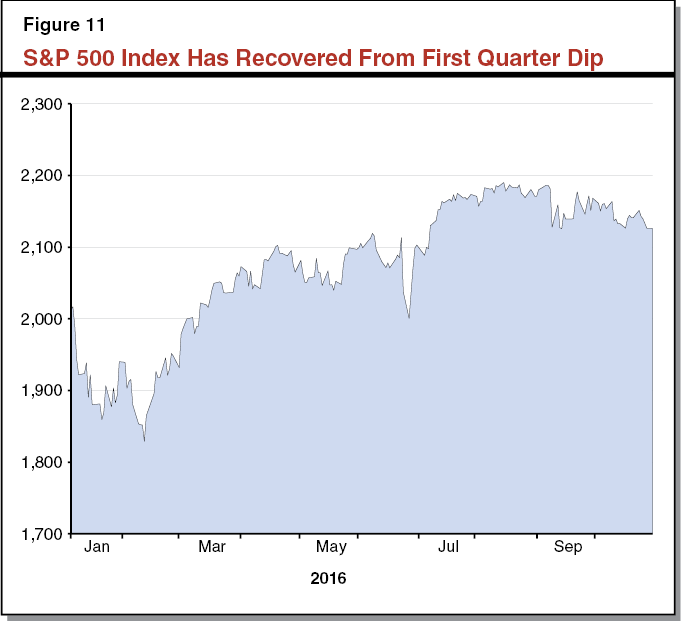

June Collections and the Weak Early 2016 Stock Market. Our working theory is that much of the recent trend in estimated payments can be explained by stock market performance since early 2016. Figure 11 shows S&P 500 index values from January 2016 through October 2016. As shown in the figure, the index was under 1900 for much of the first quarter of 2016. We think that this may help explain the disappointing level of estimated payments in June. Since then, however, the market has largely recovered. Our economic projections assume that the S&P 500 index will average 2,078 in 2016 and 2,165 in 2017, notably higher than early 2016 levels.

Assuming Steady Stock Prices, PIT Estimates Exceed Budget Projections Through 2016–17. If our assumptions come to pass, we estimate that taxpayers will make larger estimated and final payments beginning in December 2016 through early 2017 than was projected in the state budget package. This would essentially “make up” for the weak June collections. Relative to budget act assumptions, this has the effect of shifting revenues from 2015–16 into 2016–17. On net, we estimate PIT revenues will be $768 million higher than assumed in the budget for 2015–16 and 2016–17 combined.

Healthy PIT Growth in 2017–18. Looking beyond the current fiscal year, our assumptions of wages and salaries and capital gains continue to be higher than the administration’s most recent assumptions. While our estimates of personal income growth are below state budget assumptions, we currently project stronger growth in 2018. These and other factors result in healthy PIT growth of nearly 7 percent in 2017–18.

Risks to PIT Estimates. Our revenue estimates are premised upon our near–term projections about the economy and assumptions about the stock market. If those assumptions do not come to pass, revenues in 2016–17 and 2017–18 could be a few billion dollars higher or lower than the estimates reflected in Figure 7. If, for example, the S&P 500 index returns to first quarter 2016 levels, our estimates of taxpayers’ estimated and final payments described above could prove billions of dollars too high for 2016–17 and 2017–18 combined.

Sales and Use Tax

Sales Tax Estimates Down. Estimated General Fund SUT revenue totaled $24.8 billion in 2015–16, $262 million lower than the amount assumed in the June 2016 budget plan. We estimate that SUT revenues remain steady at around $24.7 billion in 2016–17, about $1 billion lower than budget assumptions. Thereafter, estimated SUT revenues increase slightly to $25 billion in 2017–18.

Reasons for Sales Tax Weakness. This short–term weakness in SUT revenue is due to several factors, including: (1) lower–than–expected revenue in 2015–16, (2) a quarter–cent rate reduction, and (3) modest growth in California personal income. At the end of 2015–16, SUT revenue was about a quarter of a billion dollars below the budget’s assumption, setting a lower starting point for subsequent growth. The temporary quarter–cent rate established by Proposition 30 will expire at the end of 2016. This rate expiration likely will reduce annual SUT revenue growth by about 3 percentage points in 2016–17 and in 2017–18 relative to revenue growth with constant tax rates. Finally, we project modest personal income growth of 3.9 percent in 2016, bringing down our near–term SUT estimates.

Corporation Tax

Corporate Profits Expected to Grow Slowly. The CT is levied on profits of California corporations and, for multistate corporations, a share of their total national profits. National corporate profits peaked in 2014 and declined over 2015. As described earlier in this chapter, our near–term economic projections are based on the consensus of various economists about the likely trend of the U.S. economy through 2018. In those projections, national corporate profits grow relatively slowly over the next several years, as rising wages and commodity prices offset increased consumer and business consumption. Consequently, we project CT revenue to decline by about 1 percent in 2016–17, followed by several years of growth that is roughly on pace with the broader economy.

CT Revenue Has Underperformed Budget Assumptions to Date. Our near–term estimates are consistent with recent cash flow trends. Through the first four months of 2016–17, net CT receipts are 14 percent below budget act projections. Last year had elevated levels of refunds, and we see this trend continuing in 2016–17.

Chapter 3: Spending Outlook

Figure 12 displays our General Fund spending estimates, by major program, through 2017–18. (Our spending projections for the entire outlook period are discussed in Chapter 4.)

Figure 12

General Fund Spending Outlook

(Dollars in Billions)

|

Estimates |

Outlook |

||||

|

2015–16 |

2016–17a |

2017–18 |

Change From 2016–17 |

||

|

Education Programs |

|||||

|

Proposition 98b |

$49.1 |

$51.0 |

$52.4 |

2.7% |

|

|

UCc |

3.2 |

3.4 |

3.4 |

1.3 |

|

|

CSU |

3.0 |

3.3 |

3.3 |

2.3 |

|

|

Student Aid Commission |

1.4 |

1.1 |

1.2 |

3.9 |

|

|

Child Care |

0.9 |

0.9 |

1.1 |

17.5 |

|

|

Health and Human Services |

|||||

|

Medi–Cal |

17.5 |

17.9 |

18.7 |

4.5 |

|

|

CalWORKs |

0.7 |

0.7 |

1.0 |

48.2 |

|

|

SSI/SSP |

2.8 |

2.9 |

2.9 |

1.5 |

|

|

IHSS |

3.0 |

3.5 |

3.7 |

6.2 |

|

|

DDS |

3.5 |

4.0 |

4.1 |

2.9 |

|

|

DSH |

1.6 |

1.7 |

1.6 |

–4.3 |

|

|

Other major programsd |

2.2 |

2.4 |

2.4 |

0.6 |

|

|

Criminal Justice Programse |

|||||

|

CDCR |

9.7 |

10.0 |

9.8 |

–1.1 |

|

|

Judiciary |

1.6 |

1.8 |

1.8 |

–2.2 |

|

|

Infrastructure Debt Servicef |

5.3 |

5.4 |

5.5 |

1.7 |

|

|

Other Programs |

|||||

|

CalSTRS |

1.9 |

2.5 |

2.6 |

6.5 |

|

|

Proposition 2 debt paymentsg |

— |

— |

2.0 |

— |

|

|

Remaining programs |

7.4 |

9.7 |

8.6 |

–11.8 |

|

|

Totals |

$114.9 |

$122.0 |

$126.1 |

3.4% |

|

|

aDeferred maintenance spending, which the Department of Finance displays in a single line item, is allocated by department in 2016–17. bReflects General Fund component of Proposition 98 minimum guarantee. cExcludes Proposition 2 payments for the UC Retirement plan. These payments are included under “other programs.” dIncludes DHCS family health and state operations, DPH, DCSS, and DSS programs not itemized above. Smaller health and human services programs are included in “remaining programs.” eExcludes smaller departments—such as the Department of Justice—that are included in “remaining programs.” fDebt service on general obligation and lease revenue bonds generally used for infrastructure. Does not include: (1) lease revenue debt service for community colleges, which is included under Proposition 98, or (2) UC’s and CSU’s debt service, which is included in their respective line items. gIn 2015–16 and 2016–17, Proposition 2 debt payment amounts are reflected elsewhere. Included in 2017–18 is the entire estimate of Proposition 2 debt payment requirements. IHSS = In–Home Supportive Services; DDS = Department of Developmental Services; DSH = Department of State Hospitals; CDCR = California Department of Corrections and Rehabilitation; DHCS = Department of Health Care Services; DPH = Department of Public Health; DCSS = Department of Child Support Services; and DSS = Department of Social Services. |

|||||

One–Time and Temporary Spending Obscure Underlying Growth Rates. One–time spending in the 2016–17 budget package obscures underlying growth in some of these programs. This includes, for example, one–time spending for deferred maintenance in the California Department of Corrections and Rehabilitation, the judicial branch, and the universities. The estimate of “remaining programs” includes one–time funding of $1 billion for the new State Project Infrastructure Fund and other, smaller one–time items. Similarly, the figure overstates the underlying growth in the California Work Opportunity and Responsibility to Kids (CalWORKs) program because 2017–18 spending in that program reflects General Fund backfill of one–time federal funds carried in from prior years (see our “CalWORKs” write–up for more information).

Education

Education Spending. In this section, we focus on Proposition 98, the universities, student financial aid programs, and child care programs. The “Proposition 98” section estimates total combined spending for elementary and secondary education (commonly referred to as K–12 education), the California Community Colleges, and a large portion of the state’s subsidized preschool program. The next section estimates spending for the University of California and the California State University. The “Financial Aid” section focuses on spending for Cal Grants and Middle Class Scholarships. The last section estimates non–Proposition 98 General Fund spending for the rest of the state’s preschool program as well as most child care programs.

Proposition 98

Proposition 98 Minimum Guarantee for Schools and Community Colleges. State budgeting for schools and community colleges is governed largely by Proposition 98, passed by voters in 1988. The measure, modified by Proposition 111 in 1990, establishes a minimum funding requirement, commonly referred to as the minimum guarantee. Both state General Fund and local property tax revenue apply toward meeting the minimum guarantee. In addition to Proposition 98 funding, schools and community colleges receive funding from the federal government, other state sources (such as the lottery), and various local sources (such as parcel taxes).

Calculating the Minimum Funding Guarantee. The Proposition 98 minimum guarantee is determined by one of three tests set forth in the State Constitution (see Figure 13). These tests depend upon several inputs, including changes in K–12 average daily attendance, per capita personal income, and per capita General Fund revenue. Though the calculation of the minimum guarantee is formula–driven, a supermajority of the Legislature can vote to suspend the formulas and provide less funding than they require. This happened in 2004–05 and 2010–11. In some cases, including as a result of a suspension, the state creates a higher out–year funding obligation referred to as a “maintenance factor.” The state is required to make progress toward meeting this higher obligation when year–to–year growth in state General Fund revenue is relatively strong. Though in most years the state has provided an amount at or close to the minimum guarantee, the state has discretion to provide any amount above the minimum guarantee.

Figure 13

The Tests and Basic Rules for Calculating the Minimum Guarantee

|

Test 1—Share of General Fund |

|

|

|

|

Test 2—Growth in Personal Income |

|

|

|

|

Test 3—Growth in General Fund Revenue |

|

|

|

|

Note: The state has suspended Proposition 98 twice. |

2015–16 and 2016–17 Updates

2015–16 Minimum Guarantee Down $378 Million From Budget Act Estimate. The decrease in the minimum guarantee (see Figure 14) is due to our estimated $1.4 billion drop in General Fund tax revenue relative to budget act estimates. As a result of this revenue drop, the state is no longer required to make the $379 million maintenance factor payment included the June budget package. This drop in the guarantee is offset by a $1 million increase due to various other adjustments.

Figure 14

Updating Estimates of 2015–16 and 2016–17 Minimum Guarantees

(In Millions)

|

2015–16 |

2016–17 |

||||||

|

June Budget Plan |

November LAO Estimate |

Change |

June Budget Plan |

November LAO Estimate |

Change |

||

|

Minimum Guarantee |

|||||||

|

General Fund |

$49,722 |

$49,082 |

–$640 |

$51,050 |

$50,973 |

–$77 |

|

|

Local property tax |

19,328 |

19,589 |

262 |

20,824 |

20,891 |

67 |

|

|

Totals |

$69,050 |

$68,672 |

–$378 |

$71,874 |

$71,864 |

–$10 |

|

2015–16 Local Property Tax Estimate Revised Upward. Though the minimum guarantee has fallen from budget act estimates, Proposition 98 local property tax revenue is up $262 million. The bulk of this increase is attributable to higher–than–expected transfers from Educational Revenue Augmentation Funds to schools and community colleges. The increase in property tax revenue reduces Proposition 98 General Fund costs on a dollar–for–dollar basis. Coupling the increase in property tax revenue with the decline in the guarantee results in Proposition 98 General Fund dropping $640 million.

Further Downward Revisions in General Fund Revenue Unlikely to Affect 2015–16 Minimum Guarantee. Under our latest revenue estimates, the operative test for calculating the guarantee in 2015–16 changes from Test 2 to Test 3. Whenever Test 3 is operative, statute requires the state to make a supplemental appropriation if needed to ensure Proposition 98 funding grows as quickly as the rest of the budget. In 2015–16, shifting to Test 3 results in the state needing to make a $53 million supplemental appropriation. This additional funding raises the guarantee up to the Test 2 level. In 2015–16, were General Fund revenue to be further revised downward by as much as $1.6 billion, the required supplemental appropriation would increase correspondingly, bringing the guarantee back up to the Test 2 level. That is, further revenue declines in 2015–16 likely would have no effect on the minimum guarantee.

2016–17 Minimum Guarantee Down $10 Million From Budget Act Estimate. At the time of budget enactment, Test 3 was the operative test in 2016–17. Even under our latest estimates, Test 3 remains operative. In Test 3 years, the minimum guarantee builds upon the prior–year funding level adjusted for changes in per capita General Fund revenue and K–12 attendance. Compared with June budget act assumptions, we estimate General Fund revenue is $1.4 billion lower in 2015–16 and $350 million lower in 2016–17. Because the drop in the prior year is greater than the drop in the current year, the year–to–year growth rate increases. The higher growth rate offsets the decline in the prior–year funding level. After updating for various other inputs, including slightly lower estimates of K–12 attendance, the minimum guarantee is only $10 million below the level assumed in June. Under the latest inputs, the state creates $321 million in new maintenance factor, for a total outstanding maintenance factor obligation at the end of 2016–17 of $873 million. The new maintenance factor created dropped from the June budget package level of $746 million, due largely to the higher General Fund growth rate.

Forecast Assumes State Funds at the Revised Estimates of the Prior–Year and Current–Year Minimum Guarantees. Although the 2015–16 minimum guarantee has fallen by $378 million, the state allocated funding to schools and community colleges based upon the higher June 2016 estimate of the guarantee. After adjusting for changes in various program costs, we estimate that currently authorized 2015–16 spending exceeds the minimum guarantee by $351 million. Historically, in virtually all cases when the prior–year or current–year guarantee has been revised downward, the state has acted to reduce associated spending. For purposes of our outlook, we assume the state designates the $351 million as payment toward its outstanding settle–up obligation. (The state currently has an outstanding settle–up obligation of about $1 billion, mostly related to the 2009–10 minimum guarantee. The state creates a settle–up obligation when the minimum guarantee rises above the level initially assumed in the budget act.) Under this approach, the $351 million is not built into the 2016–17 Proposition 98 base.

2017–18 Budget Planning

2017–18 Guarantee $2.6 Billion Higher Than Revised 2016–17 Level. As shown in Figure 15, we estimate that the minimum guarantee will grow from $71.9 billion in 2016–17 to $74.5 billion in 2017–18, an increase of $2.6 billion (3.6 percent). Test 2 is operative, with the guarantee adjusted for a 2.7 percent increase in per capita personal income and a 0.2 percent decline in K–12 attendance. In addition, because General Fund revenue is growing more quickly than per capita personal income, the state is required to make an $894 million maintenance factor payment. After making this payment, the state would end the year with no outstanding maintenance factor for the first time since 2005–06.

Figure 15

Proposition 98 Key Inputs and Outcomes Through 2017–18

(Dollars in Millions)

|

2015–16 |

2016–17 |

2017–18 |

|

|

Minimum Guaranteea |

|||

|

General Fund |

$49,082 |

$50,973 |

$52,354 |

|

Local property tax |

19,589 |

20,891 |

22,132 |

|

Totals |

$68,672 |

$71,864 |

$74,486 |

|

Change From Prior Year |

|||

|

General Fund |

–$948 |

$1,891 |

$1,380 |

|

Percent change |

–1.9% |

3.9% |

2.7% |

|

Local property tax |

$2,474 |

$1,301 |

$1,241 |

|

Percent change |

14.5% |

6.6% |

5.9% |

|

Total guarantee |

$1,526 |

$3,193 |

$2,621 |

|

Percent change |

2.3% |

4.6% |

3.6% |

|

Operative Test |

3 |

3 |

2 |

|

Maintenance Factor |

|||

|

Amount created (+) or paid (–) |

— |

$321 |

–$894 |

|

Total outstandingb |

$525 |

873 |

— |

|

Growth Rates |

|||

|

K–12 average daily attendance |

–0.2% |

–0.2% |

–0.2% |

|

Per capita personal income (Test 2) |

3.8 |

5.4 |

2.7 |

|

Per capita General Fund (Test 3)c |

3.7 |

4.4 |

4.9 |

|

K–14 cost–of–living adjustment |

1.0 |

0.0 |

1.1 |

|

aAssumes state funds at revised estimate of minimum guarantee each year. bOutstanding maintenance factor is adjusted annually for changes in K–12 attendance and per capita personal income. cAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. |

|||

Nearly Half of Increase Covered With Property Tax Revenue. Of the $2.6 billion increase in Proposition 98 funding, state General Fund revenue covers $1.4 billion and local property tax revenue covers $1.2 billion. The main factor explaining the increase in property tax revenue is a 5.3 percent increase in assessed property values. This factor accounts for about $930 million of the increase. The other large contributing factor is a $340 million increase in the ongoing savings associated with the dissolution of redevelopment agencies. This increase is primarily due to the phase out of certain one–time costs related to recent changes in the dissolution process.

$2.8 Billion Available for Proposition 98 Priorities. As shown in Figure 16, the 2016–17 Budget Act provided $71.9 billion in funding for schools and community colleges. Of this amount, $496 million was allocated for one–time activities. Though this funding is freed up for other purposes moving forward, the state already has committed through previous budget agreements to $276 million in higher 2017–18 spending. The net effect of these changes, in combination with the $2.6 billion increase in the minimum guarantee, results in the state having $2.8 billion to spend on its 2017–18 Proposition 98 priorities.

Figure 16

$2.8 Billion Increase in Proposition 98 Funding Projected for 2017–18

(In Millions)

|

2016–17 Budget Act Spending |

$71,874 |

|

Back out one–time actions: |

|

|

Secondary school career technical education grants (year two) |

–$292 |

|

CCC maintenance and instructional equipment |

–154 |

|

CCC Innovation Awards |

–25 |

|

CCC intersegmental college partnerships |

–15 |

|

CCC zero–textbook–cost degree startup funding |

–5 |

|

Adult education consortia technical assistance |

–5 |

|

Subtotal |

(–$496) |

|

Fund previously approved commitments: |

|

|

Secondary school career technical education grants (year three)a |

$200 |

|

Preschool rate and slot increasesb |

76 |

|

Subtotal |

($276) |

|

New Funds Available in 2017–18 |

$2,833 |

|

2017–18 Minimum Guarantee |

$74,486 |

|

aThe state could fund all or a portion of this program with unspent prior–year funds. bReflects augmentations of $44 million for the full–year cost of increasing the Standard Reimbursement Rate effective January 1, 2017; $24 million for the full–year cost of additional slots that will begin on April 1, 2017; and $8 million for the partial–year cost of additional slots that will begin on April 1, 2018. |

|

State Could Achieve Almost Full Implementation of the Local Control Funding Formula (LCFF) in 2017–18. In recent years, the state has dedicated most new Proposition 98 funding to implementing the LCFF. If the state continued this practice in 2017–18, we estimate it could fund 99 percent of LCFF’s full implementation cost. Specifically, we estimate the state could spend $2.5 billion to close the remaining LCFF gap, increasing per–student LCFF funding by 4.5 percent over 2016–17 levels. Our estimate assumes community colleges continue to receive 11 percent of Proposition 98 funding, the state funds previously agreed–upon commitments, and other K–12 categorical programs are adjusted for changes in attendance and cost of living.

2017–18 Guarantee Moderately Sensitive to Declines in State Revenue. We estimate that General Fund revenue could fall as much as $500 million below our estimates in 2017–18 with no change in the minimum guarantee. Even at this lower level, Test 2 would remain operative and year–to–year revenue growth would be large enough to require the state to pay down all remaining maintenance factor. For each additional dollar of revenue decline beyond this level, the guarantee would drop by about 40 cents. Regarding possible revenue increases, the minimum guarantee is mostly insensitive to any increase above the level assumed in our outlook. We estimate that 2017–18 General Fund revenue could increase about $5.5 billion before having any effect on the minimum guarantee. (An increase of this magnitude would make Test 1 operative and provide schools and community colleges about 40 cents of each dollar above the $5.5 billion threshold.) For the purpose of this sensitivity analysis, we assume prior–year revenue and other inputs remain constant. Changes to these factors could affect the thresholds and make the guarantee more or less sensitive.

Outlook for Later Years

Many Economic Scenarios Could Unfold Over the Period. State General Fund revenue over the next four years is likely to be affected by a variety of short–term developments (such as swings in the stock market) as well as long–term trends (such as growth in housing prices). In this section, we describe how the minimum guarantee would respond to two hypothetical economic scenarios—one assuming continued moderate growth over the period and one assuming a mild recession beginning in the middle of 2018. (These scenarios are discussed in greater detail in Chapter 4.) Both scenarios have built in the additional state General Fund revenue resulting from the recent passage of Proposition 55, which extended the income tax rates paid by high–income earners for an additional 12 years. (Though it does not affect the calculation of the guarantee, the recent passage of Proposition 51 is another significant development for schools and community colleges. The measure provides $9 billion in bonds for building and renovations school facilities.)

Under Growth Scenario, Minimum Guarantee Continues to Rise. As shown in the top part of Figure 17, the minimum guarantee under the growth scenario increases from $71.9 billion in 2016–17 to $83.5 billion in 2020–21. The average annual growth rate under this scenario is 3.8 percent. Under this scenario, the state creates little new maintenance factor, ending the period with about $200 million in outstanding maintenance factor obligation.

Figure 17

Proposition 98 Outlook Under Two Economic Scenarios

(Dollars in Billions)

|

2016–17 |

2017–18 |

2018–19 |

2019–20 |

2020–21 |

|

|

Economic Growth Scenario |

|||||

|

General Fund Tax Revenue |

$122.9 |

$129.5 |

$135.8 |

$142.0 |

$147.2 |

|

Minimum Guarantee |

$71.9 |

$74.5 |

$77.5 |

$80.7 |

$83.5 |

|

Year–to–year change |

— |

$2.6 |

$3.0 |

$3.2 |

$2.8 |

|

Percent change |

— |

3.6% |

4.1% |

4.1% |

3.4% |

|

Operative Test |

3 |

2 |

2 |

3 |

3 |

|

Maintenance Factor |

|||||

|

Amount created (+) or paid (–) |

$0.3 |

–$0.9 |

— |

$0.2 |

$0.0 |

|

Total outstandinga |

0.9 |

— |

— |

0.2 |

0.2 |

|

Key Factors |

|||||

|

Per capita personal income (Test 2) |

5.4% |

2.7% |

4.5% |

4.7% |

3.8% |

|

Per capita General Fund (Test 3)b |

4.4 |

4.9 |

4.6 |

4.3 |

3.4 |

|

Mild Recession Scenario |

|||||

|

General Fund Tax Revenue |

$122.9 |

$127.6 |

$124.3 |

$128.0 |

$133.9 |

|

Minimum Guarantee |

$71.9 |

$73.8 |

$72.4 |

$73.8 |

$78.1 |

|

Year–to–year change |

— |

$1.9 |

–$1.4 |

$1.5 |

$4.2 |

|

Percent change |

— |

2.7% |

–1.9% |

2.0% |

5.7% |

|

Operative Test |

3 |

2 |

3 |

1 |

1 |

|

Maintenance Factor |

|||||

|

Amount created (+) or paid (–) |

$0.3 |

–$0.2 |

$4.4 |

–$0.7 |

–$1.4 |

|

Total outstandinga |

0.9 |

0.7 |

5.1 |

4.5 |

3.1 |

|

Key Factors |

|||||

|

Per capita personal income (Test 2) |

5.4% |

2.7% |

4.5% |

1.1% |

1.7% |

|

Per capita General Fund (Test 3)b |

4.4 |

3.5 |

–2.9 |

2.7 |

4.4 |

|

Comparison of Scenarios |

|||||

|

Minimum Guarantee |

|||||

|

Economic Growth Scenario |

$71.9 |

$74.5 |

$77.5 |

$80.7 |

$83.5 |

|

Mild Recession Scenario |

71.9 |

73.8 |

72.4 |

73.8 |

78.1 |

|

Difference |

— |

$0.7 |

$5.1 |

$6.9 |

$5.4 |

|

aOutstanding maintenance factor is adjusted annually for changes in K–12 attendance and per capita personal income. bAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. |

|||||

Under Recession Scenario, Minimum Guarantee Declines in 2018–19 and Remains Below Growth Scenario. As shown in the middle part of Figure 17, the guarantee under the recession scenario declines by $1.4 billion (1.9 percent) from 2017–18 to 2018–19. In 2018–19, the state creates more than $4 billion in new maintenance factor. Even with the state making maintenance factor payments the subsequent two years, the state ends the period with $3.1 billion in outstanding maintenance factor obligation. Under the recession scenario, the guarantee grows from $71.9 billion in 2016–17 to $78.1 billion in 2020–21, an average annual growth rate of 2.1 percent. As shown in the bottom section of Figure 17, by 2020–21 the minimum guarantee under the recession scenario is more than $5 billion below the level in the growth scenario. (Though this scenario assumes the recession does not begin until 2018–19, the 2017–18 year also is affected due to state accrual policies.)