This report summarizes our office’s assessment of California’s economy and budget condition. Our main outlook scenario (referred to as our “main scenario” or “main economic scenario”) assumes continued moderate economic growth, though many other scenarios—both stronger and weaker—are possible. In this chapter, we present our estimates of the near–term budget condition. In Chapter 2, we discuss key revenue trends and our assessment of the economy. Chapter 3 presents our outlook for state spending over the next few years. We discuss various choices the state has in implementing Proposition 2—the budget reserve and debt payment measure recently approved by voters—in Chapter 4. Finally, we discuss the longer–term outlook for the budget condition in Chapter 5, comparing our main economic scenario to alternate sets of assumptions—including a hypothetical economic slowdown. The box below discusses some key information needed to understand this report.

Keys to Understanding This Report

Outlook Based on Current Laws and Practices. Our outlook is based on the state’s revenue and spending policies currently in place. For example, we assume that the temporary taxes passed by voters in Proposition 30 expire consistent with existing law. We also assume continuation of recent budget practices, such as funding increases for universities and state employee pay, as best we can. (In some programs, different interpretations of how to extend recent budget practices into the future are possible.)

Future Resources Will Differ Based on Future Policy Decisions. Our outlook provides state policymakers a sense of future budgetary resources available under a scenario in which no new budget commitments are approved. The state’s leaders can use our estimates along with other information to make decisions about changes in policies which may increase or decrease state spending or revenues. Because the state will make such changes over time, future estimates of revenues and spending will not be directly comparable to those reflected in this report.

Our Main Economic Scenario Is One of Many Possible Scenarios. We develop economic scenarios in order to produce our budget outlook. Our main economic scenario—discussed throughout this publication—reflects our best estimate, as of now, of economic trends through 2015-16. After 2015-16, it assumes moderate, ongoing economic growth, consistent with standard practices employed by many economic forecasters. Our main scenario, however, is only one of many possible economic outcomes. Future economic conditions could be stronger or weaker than our main scenario—or even weaker than the hypothetical economic slowdown scenario discussed in Chapter 5.

Different Economic Outcomes Will Affect Future State Budgets. As described above, future economic conditions may differ substantially from the scenarios we develop for this report. In particular, it is impossible to predict future stock market trends—an extremely volatile variable that is key to predicting personal income tax collections, Proposition 98, and Proposition 2 requirements. The links between the state budget, the stock market, and the economy mean that the future “bottom line” of the budget—particularly past 2015-16—will likely vary significantly from our outlook. We advise policymakers to consider our main scenario, the hypothetical economic slowdown, and other information discussed in Chapter 5 in making choices about future state policies.

Figure 1 displays our estimate of the condition of California’s General Fund through 2015–16 under our main scenario. As shown in the figure, absent changes to current law and practices, we estimate that the state would end 2015–16 with $4.2 billion in total reserves. This would consist of $641 million in the Special Fund for Economic Uncertainties (SFEU)—the state’s traditional budget reserve—and $3.6 billion in the Budget Stabilization Account (BSA). We distinguish between amounts that were deposited in the BSA before and after the voters passed Proposition 2 in Figure 1. (As discussed in Chapter 4, there is a strong argument that the Legislature could appropriate pre–Proposition 2 BSA balances with a simple majority vote, whereas the Governor would have to declare a budget emergency before the Legislature could access BSA funds deposited after passage of Proposition 2.)

Figure 1

LAO General Fund Condition Under Main Scenarioa

(In Millions)

|

|

2013–14

|

2014–15

|

2015–16

|

|

Prior–year fund balance

|

$2,186

|

$3,680

|

$836

|

|

Revenues and transfers

|

102,277

|

107,442

|

111,397

|

|

Expenditures

|

100,783

|

110,286

|

110,638

|

|

Difference between revenues and expenditures

|

$1,494

|

–$2,843

|

$760

|

|

Ending fund balance

|

$3,680

|

$836

|

$1,596

|

|

Encumbrances

|

–955

|

–955

|

–955

|

|

SFEU balance

|

2,725

|

–119

|

641

|

|

Reserves

|

|

|

|

|

SFEU balance

|

$2,725

|

–$119

|

$641

|

|

Pre–Proposition 2 BSA balance

|

—

|

1,606

|

1,606

|

|

Proposition 2 BSA balance

|

—

|

—

|

1,974

|

|

Total Reserves

|

$2,725

|

$1,488

|

$4,222

|

2014–15 Budget Erosions

The state’s 2014–15 budget package assumed that 2014–15 would end with $2.1 billion in total reserves. This consisted of a $450 million reserve in the SFEU and a $1.6 billion balance in the BSA. We now estimate a $569 million erosion in the SFEU reserve balance, leaving a year–end deficit of $119 million in that account. Combined with the $1.6 billion balance in the BSA, we estimate that total reserves will be $1.5 billion at the end of 2014–15. The decline in the SFEU balance is the net result of (1) our lower estimate of 2013–14’s entering fund balance; (2) higher revenues; (3) higher General Fund spending necessary to satisfy the Proposition 98 minimum guarantee for schools and community colleges; (4) $170 million in mandate reimbursements to cities, counties, and special districts resulting from a “trigger” included in the 2014–15 budget; and (5) other small estimating differences.

Revenue Accruals, SUT Correction Reduce Entering Fund Balance (–$243 Million). The 2014–15 budget assumed a 2013–14 entering fund balance of $2.4 billion. The state commonly adjusts the prior fiscal year’s entering fund balance as part of the budget process to reflect changes in past revenue and spending estimates. Under the state’s revenue accrual policies, personal income tax (PIT) and corporation tax (CT) estimates are regularly adjusted in this way. We estimate that PIT and CT revenue accruals for 2012–13 will increase the entering fund balance by a combined $114 million. This gain, however, is offset by a $358 million downward adjustment relating to an allocation of state sales and use tax (SUT) to local governments to correct for past accounting issues. All told, these adjustments result in an entering fund balance of $2.2 billion, or $243 million lower than the budget’s assumptions. Given our limited information about prior–year expenditures and the complexity of the state’s revenue accrual policies, we stress that this assumption could easily prove hundreds of millions of dollars too low or too high.

Revenues in 2013–14 and 2014–15 Combined Exceed Budget Projections ($2 Billion). We project that General Fund revenues and transfers will be higher than the budget’s assumptions by $92 million in 2013–14 and $2 billion in 2014–15. This is primarily due to the combination of $2.1 billion in higher PIT revenues, $984 million in higher CT collections, and $911 million in lower SUT revenues over those two fiscal years. In addition to our revised estimates for the state’s major taxes, we also estimate General Fund revenues from the unclaimed property program to be over $100 million lower than budget act estimates for 2013–14 and 2014–15 combined based on recent cash receipts that fell far short of budget act assumptions. We also assume no 2014–15 General Fund fine or penalty payments from the Pacific Gas & Electric (PG&E) Company related to the 2010 San Bruno pipeline explosion. The 2014–15 budget assumed that the General Fund would receive a $300 million PG&E payment, but an appeal makes the timing and amount of any such payment highly uncertain. It is quite possible that the General Fund will receive some payments from PG&E in the coming years, and if so, these payments would improve the budget’s bottom line.

Higher Revenues Offset by Higher Proposition 98 Spending (–$2.1 Billion). Proposition 98 is the state’s constitutional minimum funding guarantee for schools and community colleges. Under current practices for calculating the guarantee, higher state revenues in certain years can result in a dollar–for–dollar increase in Proposition 98 requirements. In 2014–15, our higher estimates of General Fund proceeds of taxes results in a nearly equal increase in General Fund spending under Proposition 98. While lower assumptions of unclaimed property revenues and the PG&E penalty reduce General Fund revenues, they do not reduce Proposition 98 requirements because these particular revenues are not proceeds of taxes factored into the Proposition 98 calculation. This partly explains the disproportionate increase in General Fund spending under Proposition 98 ($2.1 billion) compared to the increase in total General Fund revenues ($2 billion). We discuss Proposition 98 in more detail in Chapter 3.

Mandates Trigger Increases Spending (–$170 Million). The 2014–15 budget requires the Director of Finance to determine as of May 2015 whether General Fund proceeds of taxes exceed the administration’s May 2014 estimates. If so, after setting aside amounts necessary to satisfy the Proposition 98 minimum guarantee, any remaining proceeds of taxes—up to $800 million—will be allocated to cities, counties, and special districts for outstanding mandate claims. Under our estimates, this trigger results in $170 million in mandate reimbursements. (This trigger calculation does not consider some of the budget erosions described earlier.)

Main Outlook Scenario: $4.2 Billion in Reserves in 2015–16

We estimate that—absent changes to current law and practices—total reserves would grow from $1.5 billion at the end of 2014–15 to $4.2 billion at the end of 2015–16. We estimate moderate growth in the state’s “big three” revenue sources. Specifically, we estimate PIT, CT, and SUT collections to increase 4.6 percent in 2015–16, from $105 billion to $110 billion. General Fund spending is largely flat between 2014–15 and 2015–16 under our outlook, in part because certain one–time spending items do not continue into 2015–16. The combination of revenue growth and flat General Fund spending results in a $760 million increase in our estimated year–end SFEU balance during 2015–16. In addition, we calculate that Proposition 2 will require $4 billion of revenues to be split between deposits to the BSA reserve and payments on existing state debts. Below, we discuss some of the major trends in 2015–16.

Modest Revenue Growth in 2015–16. We estimate that total General Fund revenues and transfers will increase from $107 billion in 2014–15 to $111 billion in 2015–16. This is mostly explained by $2.7 billion in higher PIT revenues, $1.2 billion in increased SUT collections, and $893 million in higher CT revenues. Our PIT estimates assume somewhat slower wage and salary growth in 2015, compared to this year. In addition, we assume that the stock market will decline somewhat through early 2015, remain flat for the remainder of that year, and then grow modestly in 2016. Accordingly, our assumed PIT growth of 3.8 percent in 2015–16 is much lower than in some recent years. On the other hand, we estimate strong CT growth of 9.4 percent in 2015–16, reflecting our assumptions that corporate income will continue to grow through 2015 and that CT refunds will remain lower than budget act assumptions. These revenues are offset by required deposits to the BSA under Proposition 2 and additional special fund loans assumed to be repaid in 2015–16.

Growth in Spending Masked by One–Time Actions. As shown earlier in Figure 1, we estimate General Fund spending across 2014–15 and 2015–16 to be largely flat. Underlying growth in programmatic spending, however, is masked by various one–time and ongoing changes that offset what otherwise would have been a year–to–year increase in General Fund spending. For example, the 2014–15 budget included $1.6 billion to accelerate payment of the state’s prior deficit financing bonds—known as economic recovery bonds (ERBs). The retirement of the ERBs results in $1.7 billion more in property tax revenue available to offset General Fund spending in Proposition 98 beginning in 2015–16. (Had this ERB payment not been made in the 2014–15 budget, General Fund spending would have increased $3.3 billion year over year.) In addition, we assume that savings associated with increased federal funding of the Children’s Health Insurance Program (CHIP) under federal health care reform reduces General Fund spending for Medi–Cal by around $500 million in 2015–16 without affecting the overall level of spending for CHIP. We also assume that various one–time commitments made in the 2014–15 budget are not renewed, including funding for mandates ($270 million), multifamily housing ($100 million), drought assistance ($115 million), and higher education innovation awards ($50 million). Absent all these items, 2015–16 General Fund spending would have been around 4 percent over 2014–15 levels.

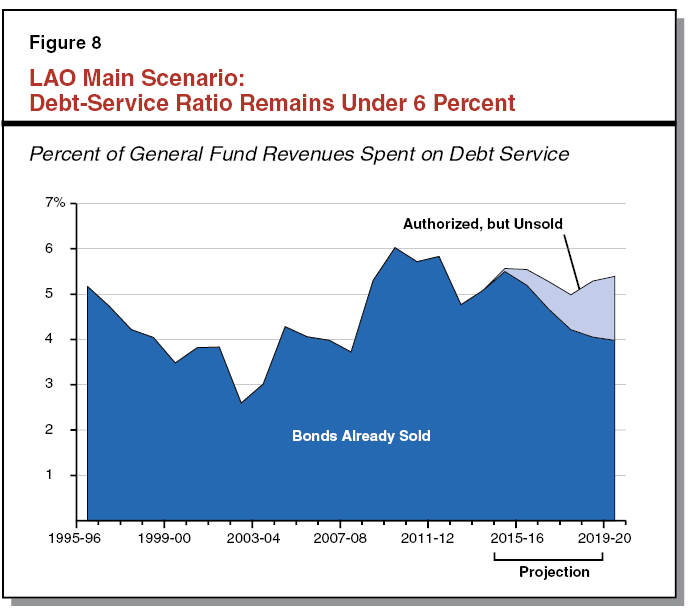

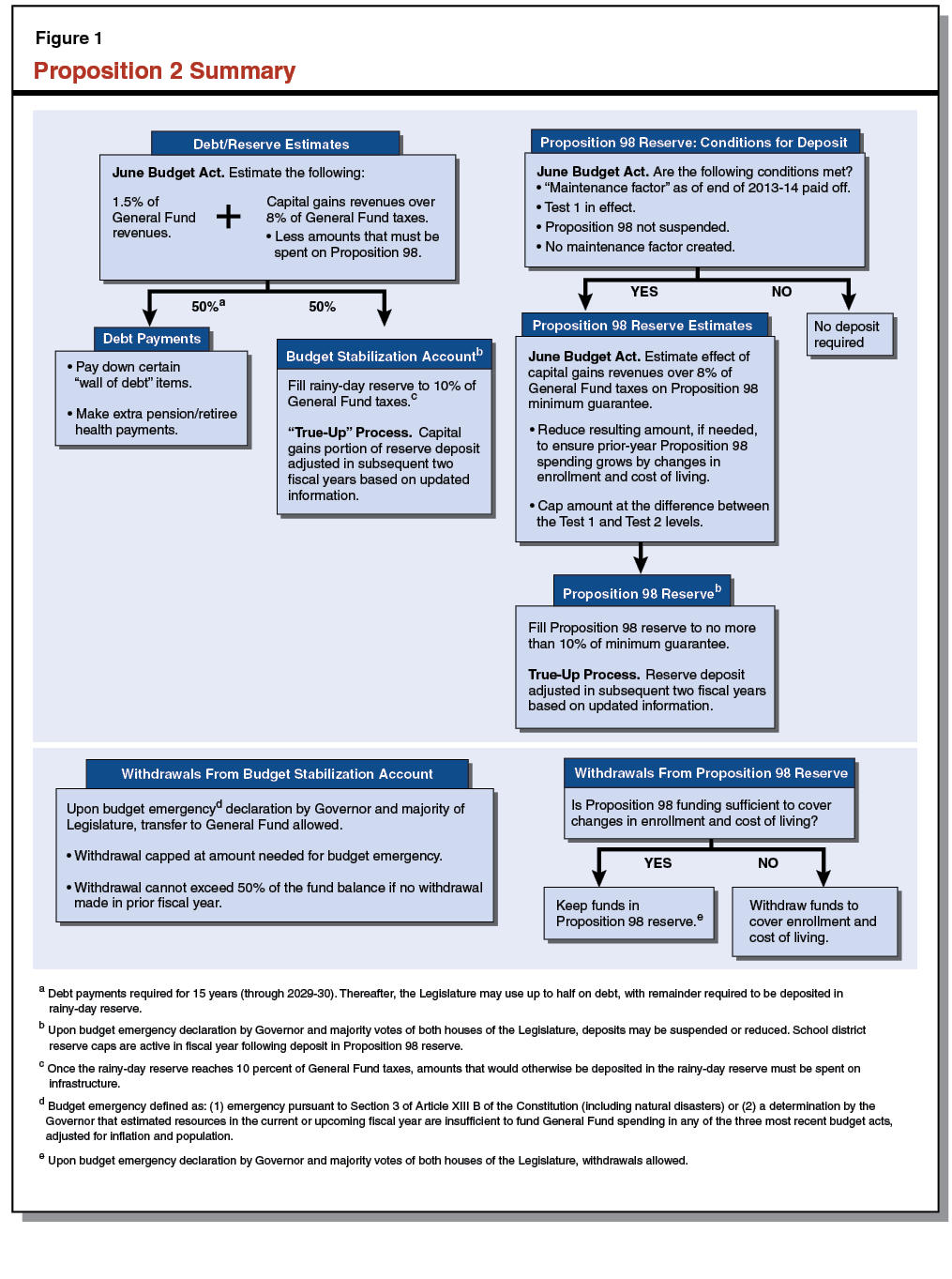

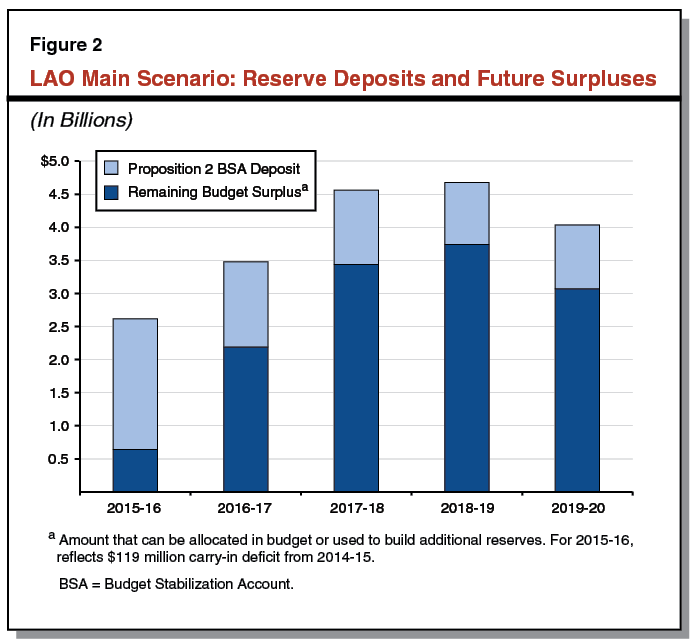

About $4 Billion Split Between Reserves and Debt Under Proposition 2. Beginning in 2015–16, Proposition 2 will change how the state saves money in reserves and pays down debt. Figure 2 summarizes some of the key changes resulting from passage of the measure. Figure 3 displays estimates of Proposition 2 requirements through 2019–20 under our main economic scenario. Because the stock market drives capital gains taxes that affect Proposition 2 and it is impossible to predict future stock market trends with precision, future Proposition 2 estimates will differ from those shown in the figure. Moreover, different choices about implementing Proposition 2 would also result in future calculations that differ from those in Figure 3.

Figure 2

Key Changes Made By Proposition 2

|

State Debts

|

|

Requires state to spend minimum amount each year to pay down specified debts.a

|

|

State Reserves

|

|

Changes amount of annual Budget Stabilization Account (BSA) deposit.a

|

|

Increases maximum size of the BSA.

|

|

Changes rules for when the state can reduce or suspend the BSA deposit.

|

|

Changes rules for withdrawing funds from the BSA.

|

|

School Reserves

|

|

Creates state reserve for schools and community colleges, the Public School System Stabilization Account (PSSSA).

|

|

Sets maximum reserves that school districts can keep in a year following a deposit into the PSSSA.b

|

Figure 3

Proposition 2 Summary Under Main Scenario

(In Millions)

|

|

2015–16

|

2016–17

|

2017–18

|

2018–19

|

2019–20

|

|

BSA and Debt Payment Calculationsa

|

|

1.5 Percent of General Fund Revenues and Transfers

|

$1,701

|

$1,760

|

$1,833

|

$1,879

|

$1,926

|

|

Excess Capital Gains Revenues

|

|

|

|

|

|

|

Capital gains revenues over 8 percent of General Fund taxes

|

2,393

|

1,613

|

810

|

—

|

—

|

|

Less amount by which these revenues increase Proposition 98 guarantee

|

–145

|

–798

|

–400

|

—

|

—

|

|

Amounts

|

$2,248

|

$815

|

$411

|

—

|

—

|

|

Totals

|

$3,949

|

$2,575

|

$2,244

|

$1,879

|

$1,926

|

|

Deposit Into BSA Reserve

|

$1,974

|

$1,288

|

$1,122

|

$940

|

$963

|

|

Debt Payments

|

1,974

|

1,288

|

1,122

|

940

|

963

|

|

Debt Payments

|

|

Assumed special fund loan repayments

|

$1,280

|

$996

|

$99

|

$113

|

—

|

|

Unallocated debt paymentsb

|

695

|

292

|

1,023

|

827

|

$963

|

|

Total, Debt Payments

|

$1,974

|

$1,288

|

$1,122

|

$940

|

$963

|

No Budget Emergency Available Under Proposition 2 Fiscal Calculation. Under Proposition 2, amounts to be deposited in the BSA can only be reduced in a budget emergency. The Governor may choose to declare a budget emergency based on conditions specified in the measure. One such condition includes a fiscal calculation shown in Figure 4. (A budget emergency could also be declared in the case of a natural disaster.) To determine the availability of a budget emergency under this fiscal calculation, the estimated resources for both the current fiscal year (2014–15) and the upcoming fiscal year (2015–16) are compared to the last three enacted budgets, adjusted for inflation and population growth. Under our main scenario, we estimate that resources in both years would be sufficient to fund the prior three adjusted budgets. As such, no budget emergency would be available under this fiscal calculation. As we describe later in this publication, the state faces choices in how to administer this particular calculation. Different decisions could change how often a budget emergency is able to be declared and could result in near–term calculations that differ from those in Figure 4.

Figure 4

Proposition 2 Budget Emergency Fiscal Calculation

(Dollars in Millions)

|

2014–15 Calculation

|

|

Estimated Resources for 2014–15a

|

$111,773

|

|

|

|

Budget emergency available?b

|

No

|

|

|

|

|

2012–13

|

2013–14

|

2014–15

|

|

Enacted budget spending

|

$91,338

|

$96,281

|

$107,987

|

|

Change in California CPI

|

3.6%

|

1.4%

|

—

|

|

Change in population

|

1.5

|

0.8

|

—

|

|

Adjusted Budget Spending

|

$96,042

|

$98,442

|

$107,987

|

|

2015–16 Calculation

|

|

Estimated Resources for 2015–16a

|

$112,885

|

|

|

|

Budget emergency available?b

|

No

|

|

|

|

|

2012–13

|

2013–14

|

2014–15

|

|

Enacted budget spending

|

$91,338

|

$96,281

|

$107,987

|

|

Change in California CPI

|

5.3%

|

3.1%

|

1.6%

|

|

Change in population

|

2.5

|

1.8

|

1.0

|

|

Adjusted Budget Spending

|

$98,538

|

$101,001

|

$110,794

|

Key Choices in Implementing Proposition 2. As we describe in Chapter 4, the state has some discretion in implementing Proposition 2. Choices the state makes could change the level of budgetary resources available for legislative appropriations in 2015–16. For example, there is a strong argument that the $1.6 billion deposited in the BSA in 2014–15 is not governed by the Proposition 2 rules, meaning that the Legislature would have greater control over these funds than it will over Proposition 2 BSA deposits.

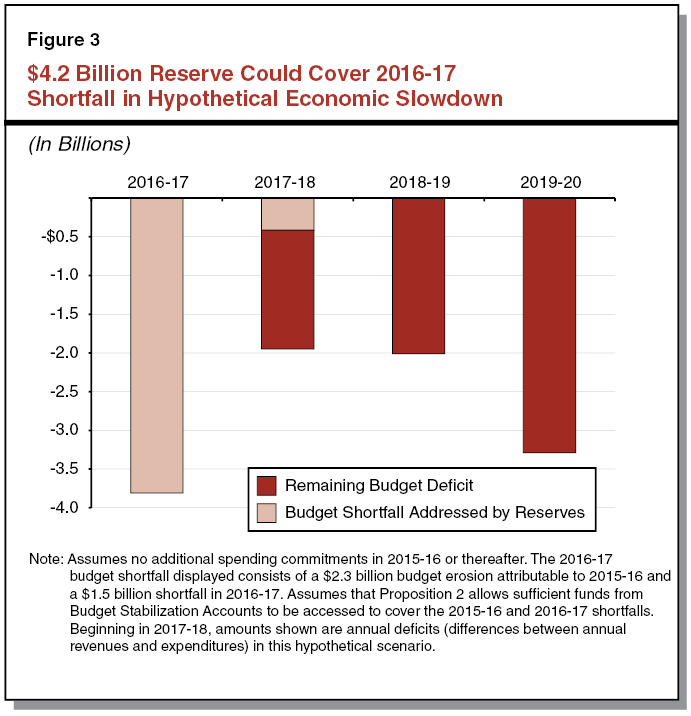

$4.2 Billion Reserve Would Be Substantial Progress. Absent new spending commitments above the increases already contained in our expenditure outlook, we estimate total state budget reserves will be $4.2 billion at the end of 2015–16. Finalizing a budget with a total reserve of this size would mark significant progress. A $4.2 billion total reserve would also be a good start to building the roughly $11 billion reserve envisioned by Proposition 2. As we illustrate in Chapter 5, a $4.2 billion reserve would stave off one hypothetical downturn scenario for a year or two before the state would again face budget problems (albeit modest budget problems compared to those of the 2000s). Considering that the U.S. economy is in the sixth year of the current economic expansion, we advise the Legislature to keep making progress in accumulating state budget reserves. However, in order to maintain approximately $4 billion in total reserves in 2015–16, there would be little or no capacity for added non–Proposition 98 spending commitments in the next year under our estimates.

Even Higher Revenues in 2014–15 Would Almost All Go to Schools. As described in Chapter 2, our estimates for PIT revenues in 2014–15 may prove to be too cautious given recent stock market and other trends. While the current level of the stock market suggests that capital gains revenues may wind up higher in 2014 than what we have assumed in our outlook, we have tried to peg our 2014–15 PIT estimates closer to the more modest cash flow trends received to date in 2014. Nevertheless, even if PIT revenues wind up higher than what we now display for 2014–15, there would be little bottom line benefit for the General Fund, as virtually all of these higher revenues likely would be required to be given to schools and community colleges. In addition, increases in 2014–15 revenues could permanently ratchet up the Proposition 98 minimum guarantee, making it somewhat harder to fund non–Proposition 98 programs in the future. We discuss choices the state faces in budgeting required increases in school funding in Chapter 3.

Positive Trends for U.S. and California. The U.S. economy began its recovery from the last recession in June 2009. Now well into its sixth year of expansion, the U.S. economy—as well as California’s—appears to be on solid footing based on various measures. The U.S. is leading global growth as Europe and China struggle somewhat. Strengthening demand is driving the current U.S. expansion, and this has positive implications for state and local budgets. House prices have strengthened considerably. Stock prices have soared over much of the past year. The unemployment rate has fallen, even though long–term unemployment (those unemployed for 27 weeks or more) remains elevated.

LAO’s Main Economic Scenario Assumptions. The positive trends discussed above are reflected in the main economic and budget scenario we discuss throughout this publication. The major economic assumptions underlying our main scenario are listed in Figure 1. It is important to note that no such set of assumptions will prove completely accurate over time. The main scenario, however, reflects (1) our best estimate, as of now, of near–term economic conditions and (2) a general assumption that growth will continue—and in some respects, accelerate—over the next few years. (In Chapter 5, we discuss hypothetical alternate scenarios—including one involving a stock market downturn and economic slowdown, in order to illustrate such a slowdown’s effect on state finances.) Figure 2 compares some key assumptions in the main scenario to ones in recent state budget outlooks.

Figure 1

LAO Economic Assumptions: November 2014 Main Scenario

Percent Change Unless Otherwise Indicated

|

United States

|

2014

|

2015

|

2016

|

2017

|

2018

|

2019

|

2020

|

|

Real gross domestic product

|

2.3%

|

2.7%

|

2.9%

|

3.1%

|

2.8%

|

2.7%

|

2.6%

|

|

Personal income

|

4.2

|

4.6

|

5.1

|

5.7

|

5.2

|

5.0

|

4.9

|

|

Wage and salary employment

|

1.8

|

1.8

|

1.5

|

1.3

|

1.0

|

0.9

|

0.9

|

|

Unemployment rate (percent)

|

6.2

|

5.7

|

5.5

|

5.3

|

5.2

|

5.1

|

5.0

|

|

Consumer price index

|

1.8

|

1.4

|

1.6

|

2.0

|

2.1

|

2.1

|

2.2

|

|

Housing starts (thousands)

|

994

|

1,194

|

1,356

|

1,492

|

1,522

|

1,548

|

1,566

|

|

Federal funds rate

|

0.1%

|

0.4%

|

1.6%

|

3.3%

|

3.8%

|

3.8%

|

3.8%

|

|

S&P 500 annual average

|

1,914

|

1,929

|

1,979

|

2,041

|

2,104

|

2,176

|

2,250

|

|

California

|

2014

|

2015

|

2016

|

2017

|

2018

|

2019

|

2020

|

|

Personal income

|

4.9%

|

4.8%

|

5.4%

|

6.2%

|

5.7%

|

5.6%

|

5.5%

|

|

Wage and salary employment

|

2.2

|

2.1

|

1.8

|

1.9

|

1.6

|

1.7

|

1.8

|

|

Unemployment rate (percent)

|

7.5

|

6.6

|

5.9

|

5.4

|

5.3

|

5.2

|

5.1

|

|

Consumer price index

|

1.8

|

1.4

|

1.6

|

2.0

|

2.1

|

2.1

|

2.2

|

|

Housing permits (thousands)

|

83.4

|

94.2

|

110.5

|

132.4

|

142.3

|

144.4

|

145.1

|

|

Single–unit permits

|

36.7

|

37.4

|

46.9

|

62.2

|

68.5

|

68.3

|

66.9

|

|

Multifamily permits

|

46.7

|

56.8

|

63.6

|

70.2

|

73.8

|

76.1

|

78.3

|

|

Population growth

|

0.8%

|

0.7%

|

0.5%

|

0.5%

|

0.5%

|

0.5%

|

0.4%

|

Figure 2

Comparing Recent Economic Outlooks

|

|

2014

|

|

2015

|

|

2016

|

|

DOF

May

2014

|

LAO

May

2014

|

LAO

Nov.

2014

|

DOF

May

2014

|

LAO

May

2014

|

LAO

Nov.

2014

|

DOF

May

2014

|

LAO

May

2014

|

LAO

Nov.

2014

|

|

United States

|

|

|

|

|

|

|

|

|

|

|

|

|

Percent change in:

|

|

|

|

|

|

|

|

|

|

|

|

|

Real gross domestic product

|

2.4%

|

2.4%

|

2.3%

|

|

3.0%

|

3.0%

|

2.7%

|

|

3.4%

|

3.4%

|

2.9%

|

|

Personal income

|

3.6

|

3.6

|

4.2

|

|

5.1

|

5.1

|

4.6

|

|

5.4

|

5.4

|

5.1

|

|

Wage and salary employment

|

1.6

|

1.6

|

1.8

|

|

1.9

|

1.9

|

1.8

|

|

2.1

|

2.1

|

1.5

|

|

California

|

|

|

|

|

|

|

|

|

|

|

|

|

Percent change in:

|

|

|

|

|

|

|

|

|

|

|

|

|

Personal income

|

4.6%

|

4.6%

|

4.9%

|

|

5.1%

|

5.6%

|

4.8%

|

|

5.4%

|

5.6%

|

5.4%

|

|

Wage and salary employment

|

2.5

|

2.2

|

2.2

|

|

2.5

|

2.4

|

2.1

|

|

2.4

|

2.2

|

1.8

|

|

Unemployment rate

|

7.6

|

7.6

|

7.5

|

|

6.9

|

6.7

|

6.6

|

|

6.5

|

6.0

|

5.9

|

|

Housing permits (thousands)

|

106

|

93

|

83

|

|

123

|

110

|

94

|

|

141

|

120

|

110

|

Housing Trends a Big Question Mark

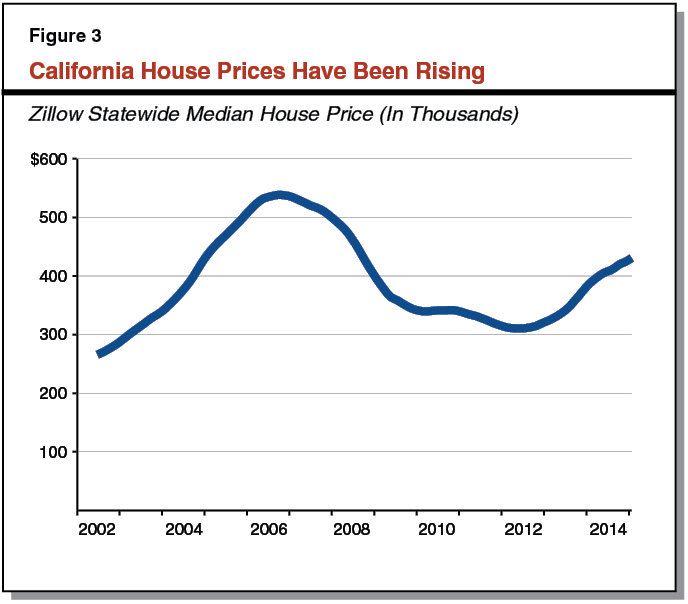

In last November’s Fiscal Outlook, we discussed various unusual features of the housing recovery, including then–unsustainable price gains and limited increases in housing construction. We cautioned that “given the sizable shifts taking place in today’s housing market…actual price gains and construction activity in the coming years could vary widely—either above or below—our office’s forecast over the next few years.” Our caution was well founded. We have been surprised by some recent trends in California’s housing markets.

Prices Have Been Rising Rapidly. As shown in Figure 3, the median house price in California—as tracked by the online real estate company Zillow—has risen sharply since 2012. Over the 12 months ending in May 2014, the median price increased over 15 percent. Year–over–year growth slowed a bit thereafter, but has remained strong. As of September 2014, the median price was about $431,000, up 10 percent from one year prior. Despite these substantial price increases, residential building permits in California this year are far fewer than what we assumed a year ago. In fact, it appears possible that California residential construction activity in 2014, as measured by the number of residential building permits, will be below the 2013 level.

Building Permits Not Responding in Kind. Our main economic scenario—summarized in Figure 1—continues to assume that California residential building permits return over the next several years to levels one would expect based on population growth and historical household formation trends. Yet, it is possible that residential building will not return to these levels or will take much longer to do so than we have assumed. Data suggests that the number of household formations—for example, when younger people move out of parents’ homes—has fallen considerably. There are several possible explanations for this trend. One is that first–time homebuyers are finding it more difficult to purchase homes at current prices. It is also possible that, despite strong demand and rising prices, various factors are preventing developers from increasing production of new housing. These factors may include heightened caution among developers and local government resistance to additional building. Alternatively, Californians may be altering fundamentally their economic, lifestyle, and related choices concerning homes. If these trends continue, they could result in meaningful changes in the California economy—some negative and some positive—affecting construction employment, sales taxes, property taxes, income taxes, population growth, and housing affordability. Our office anticipates releasing additional analyses of issues concerning housing supply, demand, and prices in publications over the next year or so. It is possible that future outlooks concerning California’s housing market will be quite different from the one in this publication.

Figure 4 summarizes state General Fund revenues and transfers under our main economic scenario. Figure 5 compares this revenue outlook to ones that our office and the administration released in May 2014 for 2013–14 and 2014–15. (The administration’s May revenue outlook was used by the Governor and the Legislature as the basis for the 2014–15 Budget Act in June 2014.)

Figure 4

LAO Revenue Outlook (Main Economic Scenario)

General Fund and Education Protection Account Combined (Dollars in Millions)

|

|

2013–14

|

2014–15

|

2015–16

|

2016–17

|

2017–18

|

2018–19

|

2019–20

|

|

Personal income tax

|

$66,667

|

$72,201

|

$74,932

|

$78,011

|

$81,521

|

$83,055

|

$84,054

|

|

Sales and use tax

|

22,251

|

23,420

|

24,653

|

25,433

|

26,029

|

27,238

|

28,418

|

|

Corporation tax

|

8,519

|

9,482

|

10,375

|

10,287

|

10,240

|

10,562

|

11,163

|

|

Subtotals, “Big Three” taxes

|

$97,437

|

$105,103

|

$109,960

|

$113,732

|

$117,790

|

$120,855

|

$123,635

|

|

Percent change from prior year

|

—

|

7.9%

|

4.6%

|

3.4%

|

3.6%

|

2.6%

|

2.3%

|

|

Insurance tax

|

$2,371

|

$2,435

|

$2,512

|

$2,593

|

$2,687

|

$2,771

|

$2,854

|

|

Other revenues

|

2,093

|

2,050

|

2,018

|

1,909

|

1,940

|

1,935

|

1,928

|

|

Transfers to Pre–Proposition 2 BSA

|

—

|

–1,606

|

—

|

—

|

—

|

—

|

—

|

|

Transfers to Proposition 2 BSA

|

—

|

—

|

–1,974

|

–1,288

|

–1,122

|

–940

|

–963

|

|

Transfers and loans

|

376

|

–540

|

–1,118

|

–926

|

–208

|

–288

|

–5

|

|

Totals, Revenues and Transfersa

|

$102,277

|

$107,442

|

$111,397

|

$116,020

|

$121,087

|

$124,335

|

$127,449

|

|

Percent change from prior year

|

—

|

5.1%

|

3.7%

|

4.2%

|

4.4%

|

2.7%

|

2.5%

|

Figure 5

Comparing LAO and Administration Revenue Projections for 2013–14 and 2014–15

General Fund and Education Protection Account Combined (In Millions)

|

|

2013–14

|

|

2014–15

|

|

LAO

May 2014

|

DOF

May 2014

(Budget Act)

|

LAO

Nov. 2014

|

LAO

May 2014

|

DOF

May 2014(Budget Act)

|

LAO

Nov. 2014

|

|

Personal income tax

|

$66,967

|

$66,522

|

$66,667

|

|

$73,012

|

$70,238

|

$72,201

|

|

Sales and use tax

|

22,581

|

22,759

|

22,251

|

|

23,222

|

23,823

|

23,420

|

|

Corporation tax

|

8,398

|

8,107

|

8,519

|

|

8,980

|

8,910

|

9,482

|

|

Subtotals, “Big Three” taxes

|

$97,945

|

$97,388

|

$97,437

|

|

$105,214

|

$102,971

|

$105,103

|

|

Insurance tax

|

$2,271

|

$2,287

|

$2,371

|

|

$2,368

|

$2,382

|

$2,435

|

|

Other revenues

|

2,164

|

2,163

|

2,093

|

|

2,414

|

2,400

|

2,050

|

|

Transfers to Pre–Proposition 2 BSA

|

—

|

—

|

—

|

|

–1,638

|

–1,606

|

–1,606

|

|

Transfers and loans

|

347

|

347

|

376

|

|

–658

|

–658

|

–540

|

|

Totals, Revenues and Transfersa

|

$102,727

|

$102,185

|

$102,277

|

|

$107,700

|

$105,488

|

$107,442

|

As noted above, our November 2014 main scenario reflects (1) our best estimate, as of now, of near–term economic conditions and (2) an assumption that growth generally will continue—and in some respects, accelerate—over the next few years. Actual results will vary from our current revenue outlook, either positively or negatively (and perhaps by billions of dollars), particularly in the later fiscal years displayed.

Rainy–Day Fund Transfers Reflected in Revenue Tables. Consistent with the administration’s method of displaying the state’s fiscal condition, Figures 4 and 5 and other tables in this publication deduct transfers from the General Fund to the state’s rainy–day accounts, displaying them as transfers out of the General Fund. These transfers out are listed as negative numbers in Figures 4 and 5, for example. This is a change in practice for our office, such that the numbers in these figures are not directly comparable to those in prior LAO publications. Figure 5 shows the May and November 2014 revenue estimates on an “apples–to–apples” basis in order to improve comparability.

General Fund Revenues Above Budget Act Projections

Both 2013–14 and 2014–15 Appear Above Budget Projections. State revenue collections finished 2013–14 above the projections that were included in the June 2014 state budget act. In 2014–15, monthly revenue collections have also been running over $1 billion above the budget projections, based on preliminary data through the end of October.

As shown in Figure 5, we currently expect total revenues and transfers for 2013–14 to be booked at $92 million above the June 2014 budget projections. For 2013–14, gains for the personal income tax (PIT) and corporation tax (CT) were offset by declines, relative to budget act projections, for the SUT and unclaimed property revenues.

For 2014–15, we currently project revenues and transfers to end the fiscal year about $2 billion above the June 2014 budget projections. For 2014–15, expected gains for PIT, CT, and the state’s insurance tax are being offset by weakness, relative to budget act projections, for the SUT and some minor state revenue sources. We discuss some of the assumptions underlying these figures below.

Personal Income Tax

Dominant Revenue Source. In our main scenario, California’s PIT makes up about two–thirds of state General Fund revenues and transfers for the foreseeable future—both before and after the temporary Proposition 30 rate increases expire for the state’s highest–income PIT filers. As we have noted previously, the end of the Proposition 30 PIT rate increases will not necessarily cause a sudden revenue drop off—a “cliff effect”—for the annual state budget process. Because these rate increases expire at the end of calendar year 2018, it means that state PIT revenues essentially will include an entire fiscal year of Proposition 30 revenues in 2017–18, half a fiscal year of those revenues in 2018–19, and none of the Proposition 30 revenues in 2019–20. Accordingly, if the economy is growing at that time, as our main scenario assumes, then the expiration of Proposition 30 is likely to result in a slowing of PIT revenue growth in 2018–19 and 2019–20, but not an outright decline in PIT revenues.

Recent Strong Growth of Wage and Salary Withholding. Wages and salaries are a large and generally stable part of California’s PIT revenue base. Employers are required to withhold part of each employee’s paycheck each month and send this money to the state to cover the PIT due on the employee’s income. Withholding makes up about two–thirds of net PIT collections each year. The revenue stream from these withholding payments provides a real–time indicator of the growth of wage and salary income.

Withholding growth has been strong in 2014. Withholding for each month from April to October has been between 7 percent and 11 percent above the same month in 2013 (after adjusting for variation in the number of processing days in a given month from one year to the next). For 2014 as a whole, we assume that wages and salaries for California resident PIT filers will be 6.7 percent above 2013 levels—notably higher than the 6 percent growth we projected in May, as well as the 5 percent growth assumed in the June 2014 state budget package. In 2015, our main scenario assumes that wage and salary growth moderates to 5.1 percent.

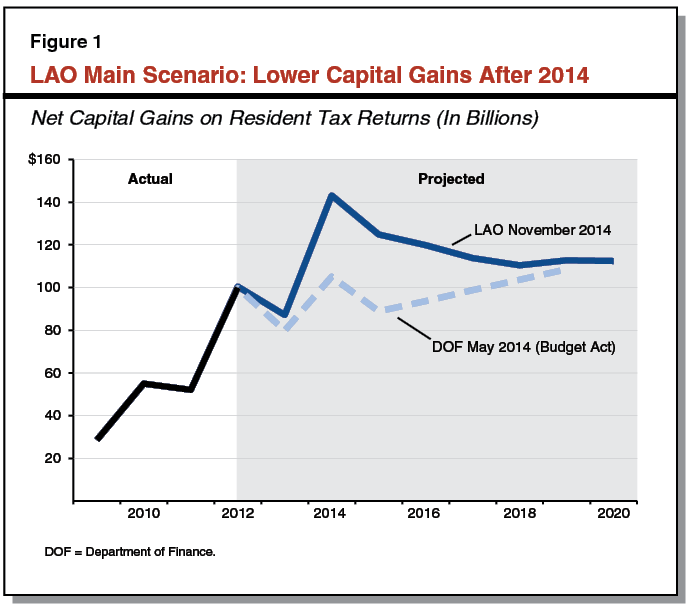

Estimated Payments Also Showing Strong Growth . . . Taxpayers who have significant income from sources other than wages and salaries are required to make quarterly estimated payments. Sources of such income include capital gains from sales of assets such as stocks and real estate, interest and dividend payments, and profits of businesses that are not subject to the state’s CT. As estimated payments come in each year in April, June, and September, they provide early indications of the total amount of taxable nonwage income that higher–income taxpayers will earn that year. In addition to those estimated payments, other 2014 estimated payments will come into the state treasury in December and January, followed by final or extension payments in April. In many years, high–income taxpayers make large estimated payments in December and January and large payments in April to “settle up” their annual tax liabilities.

For tax year 2014, the first three estimated payments are running about 15 percent above the comparable months in 2013. This is a significant increase, and it contributes to our main scenario assumption that the net amount of capital gains income reported on California residents’ PIT returns in 2014 will be $143 billion—up significantly from the $105 billion assumed for 2014 net capital gains in the June 2014 state budget package.

. . . But Our Outlook Makes Cautious Assumptions About 2014 Capital Gains. Despite our positive outlook for capital gains, relative to the most recent budget act assumptions, we believe that our assumptions for 2014 capital gains—and estimated payments generally—are cautious. We think there is a significant possibility that capital gains reported on 2014 PIT returns will prove to be higher than we now assume. The S&P 500 stock index, for example, has risen substantially in recent months—considerably above our prior expectations. The trend in stock and other asset prices, as well as recent trends in personal income, suggest that 2014 taxable income from capital gains and business activity will be above levels indicated by estimated payments that have been received to date. Our near–term fiscal outlook, however, adopts the cautious assumption that revenue from estimated payments through January 2015 and final payments in April 2015 will be fairly consistent with the estimated payment trend observed to date this year. If capital gains and other estimated payment sources are stronger than we now assume, this could easily increase 2014–15 state PIT revenues by $1 billion or more above our current outlook. As discussed elsewhere in the publication, virtually all of those increased 2014–15 revenues would go to schools and community colleges under the state’s Proposition 98 minimum funding guarantee.

Modest Future Stock Price Growth Assumed. California’s PIT is heavily reliant on high–income taxpayers who pay the highest marginal PIT rates and who receive a large share of capital gains and business income. In fact, the top 1 percent of California PIT filers paid 50 percent of the state’s personal income taxes in 2012. Capital gains—generating over $12 billion of PIT revenues in 2014–15, according to our forecast assumptions—are one major source of year–over–year volatility in PIT collections. As they are closely connected with trends of highly variable stock prices, they are impossible to predict far in advance with any precision. The S&P 500 stock index closed at 2,040 on November 14, 2014—up about 250 points from one year before. In our main scenario, we assume that the S&P 500 stock index retreats somewhat from these strong recent gains by declining to just over 1,925 in early 2015 and remaining flat throughout the rest of 2015. We assume modest growth of about 3 percent per year in the S&P 500 index in our main scenario beginning in 2016. While every forecast of California’s state budget must make assumptions about stock prices—either explicitly or implicitly—actual results will vary from our future assumptions either positively or negatively in any given year. As we discuss in Chapter 5, a large stock market drop—if one were to occur—could cause state revenues to fall by billions of dollars in a single year.

Sales and Use Tax

Below 2014 Budget Projections. Estimated General Fund SUT revenue totaled $22.3 billion in 2013–14, $508 million lower than the amount assumed in the 2014–15 budget. In our main economic scenario, SUT receipts increase by 5.3 percent in each of the next two fiscal years, totaling $23.4 billion in 2014–15 and $24.7 billion in 2015–16. Our 2014–15 estimate is $403 million lower than the assumption in the June 2014 state budget. Under our main scenario, SUT revenues then grow more slowly over the following two fiscal years as the one–quarter cent Proposition 30 SUT increase ends in December 2016. As with the Proposition 30 PIT increases, the timeline of this tax expiration means that the state will see a gradual drop off in Proposition 30 SUT revenues over two fiscal years.

Prior Years’ Local SUT Adjustment. As discussed in Chapter 1, we assume that the General Fund’s entering fund balance in 2013–14 will be lowered by $358 million to reflect a prior–year misallocation of SUT revenues to local governments that recently was identified and corrected by the state. We understand that this amount will be booked in the state’s budgetary accounting system in this way, thereby not affecting any particular fiscal year’s accrued SUT revenues.

Corporation Tax

Above 2014 Budget Projections. Refunds to CT payers have been running below June 2014 budget assumptions. This is a positive development for net CT collections by the state. As a result, in our main scenario, estimates of net CT revenues accrued to 2012–13 and of CT revenues in 2013–14 and 2014–15 are all above budget act projections. In that scenario, we estimate that CT revenue will grow from $8.5 billion in 2013–14 to $9.5 billion in 2014–15 and $10.4 billion in 2015–16. Our near–term CT outlook reflects strong growth in recent CT collections and an assumption that recent trends in CT refunds will continue. Our main scenario assumes that corporate income will continue to grow through 2015. In later years, however, corporate income is assumed to decline somewhat from these high levels.

Operating Loss Deductions Expected to Remain at Elevated Levels. As we anticipated in last year’s Fiscal Outlook, corporations significantly increased their use of net operating loss (NOL) deductions from $3 billion in 2011 to approximately $19 billion in 2012. The use of NOL deductions—in which corporations deduct a prior loss from current tax year profits—was suspended for most corporations during tax years 2008 through 2011. We anticipate that NOLs will remain at elevated levels throughout the forecast period, but NOL use in any given year is highly uncertain. We also expect use of the state’s largest corporate tax credit program, the research and development tax credit, to increase somewhat in future years. Beginning in the 2016 tax year, our forecast takes into account recent legislative actions to increase the amount of credits available under the film and television tax credit and California Competes tax program.

Other Issues

Unclaimed Property Revenues Lower Than June 2014 Budget Projections. The State Controller’s Office receives various types of property considered to be abandoned by owners. The state maintains an obligation to reunite these properties with their rightful owners, should they make a claim. Each month, however, amounts unclaimed in excess of $50,000 become General Fund revenues. June and July are the most important cash months for unclaimed property. Official reports for July 2014 show cash receipts well below 2014–15 budget assumptions. We assume this reflects an ongoing reduction in the amount of property received by the state, affecting each year starting with 2013–14. Over 2013–14 and 2014–15 combined, we estimate that revenues related to unclaimed property will be over $100 million lower than assumed in the 2014–15 budget package. Because various parts of the program expire after 2015–16 under current law, we expect these revenues to decrease around 10 percent in 2016–17 and remain steady thereafter.

$1.3 Billion in Special Fund Loans Assumed Repaid in 2015–16. Figure 6 displays the loans we assume that the General Fund will repay to various state special funds in 2015–16. (If all of those payments were made, $1.8 billion in special fund loans would remain outstanding.) We assume that any loan with a deadline in law will be repaid by that date. In addition, when it appears a special fund requires a loan repayment, we assume any loan outstanding to that fund is repaid. As discussed in Chapter 1, special fund loan repayments count toward the debt payment requirements of Proposition 2.

Figure 6

Special Fund Loans Assumed to Be Repaid in 2015–16a

(In Millions)

|

Fund Name

|

Amount

|

|

Disability Insurance Fund

|

$303.5

|

|

Motor Vehicle Account, State Transportation Fund

|

300.0

|

|

State Court Facilities Construction Fund

|

220.0

|

|

Greenhouse Gas Reduction Fund

|

200.0

|

|

Occupancy Compliance Monitoring Account

|

57.0

|

|

Tax Credit Allocation Fee Account

|

48.0

|

|

Hospital Building Fund

|

30.0

|

|

Electronic Waste Recovery & Recycling Account

|

27.0

|

|

Off–Highway Vehicle Trust Fund

|

21.0

|

|

Hazardous Waste Control Account

|

13.0

|

|

False Claims Act Fund

|

12.7

|

|

California Health Data and Planning Fund

|

12.0

|

|

Dealers’ Record of Sale Account

|

6.5

|

|

California Debt and Investment Advisory Commission Fund

|

2.0

|

|

California Debt Limit Allocation Committee Fund

|

2.0

|

|

Drinking Water Operator Certification Special Account

|

1.6

|

|

Illegal Drug Lab Cleanup Account

|

1.0

|

|

Driving–Under–the–Influence Program Licensing Trust Fund

|

0.3

|

|

Total

|

$1,257.6

|

The three largest loan repayments shown in Figure 6 have 2015–16 deadlines in law. It appears to us that the Legislature may have considerable flexibility in determining whether to repay these loans. In addition, while the Greenhouse Gas Reduction Fund loan does not have a deadline in current law, the 2014–15 budget package authorized amounts to be repaid and used for the high–speed rail project beginning in 2015–16. Of the $400 million balance currently outstanding from that fund, we assume that half is repaid in 2015–16 and that the remainder is repaid in 2016–17.

Major Penalty and Fine Revenue Uncertain. Each year, the state General Fund receives payments from court and administrative judgments. In 2012–13, for example, $23 million of such payments were received by the General Fund. The June 2014–15 budget assumed that the state would receive $323 million of such payments in 2014–15, including a potential $300 million payment from the Pacific Gas and Electric (PG&E) Company, the possibility of which had been disclosed publicly to PG&E investors earlier in the spring. The penalties and fines were related to PG&E operations and practices, including the 2010 rupture of a gas pipeline in San Bruno. On September 2, the California Public Utilities Commission issued decisions by administrative law judges that sought to impose a $1.4 billion penalty on PG&E, including a $950 million payment to the state General Fund. On October 2, PG&E filed appeals concerning these decisions. Accordingly, there is now uncertainty about the timing of any General Fund payments by PG&E, as well as the amounts of those payments. Due to this uncertainty, we assume no General Fund payments by PG&E in our revenue outlook. It is quite possible that some PG&E payments will be received by the General Fund in the future, and if so these payments would improve the budget’s bottom line.

Figure 1 displays our estimates of General Fund spending for 2013–14 and 2014–15, as well as our outlook for spending through 2019–20. The estimates in Figure 1 reflect our main economic scenario. Assuming continued moderate economic growth, we estimate General Fund spending to grow at an average annual rate of 2.4 percent. This slow growth rate is primarily explained by key assumptions concerning Proposition 98. The assumed expiration of Proposition 30’s taxes and our assumption that capital gains revenues decline contribute to slow growth in the Proposition 98 minimum guarantee in the later years of the outlook. Further, our General Fund spending outlook is affected by local revenues because Proposition 98 is funded by a combination of state General Fund and local property taxes. While we project growth in overall Proposition 98 funding, our strong outlook for local property tax growth offsets what would otherwise be higher General Fund spending necessary to meet Proposition 98 requirements. Because Proposition 98 General Fund spending represents around 40 percent of the budget, these assumptions are key factors in the slow growth rate of spending overall. We discuss this and other spending trends throughout this chapter. In general, this chapter discusses our main scenario spending outlook unless noted otherwise.

Figure 1

General Fund Spending Under Main Scenario

Includes Education Protection Account (Dollars in Millions)

|

|

Estimates

|

|

Outlook

|

Average Annual Growtha

|

|

|

2013–14

|

2014–15

|

2015–16

|

2016–17

|

2017–18

|

2018–19

|

2019–20

|

|

Education Programs

|

|

|

|

|

|

|

|

|

|

|

Proposition 98

|

$42,794

|

$46,548

|

|

$46,422

|

$47,555

|

$48,715

|

$49,350

|

$49,909

|

1.4%

|

|

Child care

|

762

|

822

|

|

848

|

855

|

865

|

877

|

891

|

1.6

|

|

CSUb

|

2,256

|

2,696

|

|

2,816

|

2,940

|

3,069

|

3,204

|

3,343

|

4.4

|

|

UC

|

2,844

|

2,991

|

|

3,106

|

3,230

|

3,360

|

3,494

|

3,634

|

4.0

|

|

Student Aid Commission

|

1,056

|

1,547

|

|

1,649

|

1,783

|

1,899

|

1,962

|

2,029

|

5.6

|

|

Health and Human Services

|

|

|

|

|

|

|

|

|

|

|

Medi–Cal

|

16,647

|

17,239

|

|

17,051

|

17,862

|

18,678

|

19,493

|

20,972

|

4.0

|

|

CalWORKs

|

1,195

|

783

|

|

766

|

553

|

461

|

447

|

448

|

–10.5

|

|

SSI/SSP

|

2,780

|

2,810

|

|

2,847

|

2,886

|

2,926

|

2,967

|

3,009

|

1.4

|

|

IHSS

|

2,027

|

2,248

|

|

2,480

|

2,550

|

2,625

|

2,692

|

2,764

|

4.2

|

|

DDS

|

2,797

|

2,956

|

|

3,055

|

3,211

|

3,315

|

3,422

|

3,534

|

3.6

|

|

DSH

|

1,435

|

1,463

|

|

1,492

|

1,522

|

1,560

|

1,594

|

1,594

|

1.7

|

|

Other major programsc

|

1,493

|

1,663

|

|

1,644

|

1,655

|

1,655

|

1,657

|

1,657

|

–0.1

|

|

CDCR

|

8,937

|

9,073

|

|

9,066

|

9,071

|

9,160

|

9,263

|

9,366

|

0.6

|

|

Judiciary

|

1,215

|

1,392

|

|

1,488

|

1,515

|

1,549

|

1,584

|

1,621

|

3.1

|

|

CalSTRS

|

1,360

|

1,486

|

|

1,928

|

2,413

|

2,463

|

2,539

|

2,617

|

12.0

|

|

Infrastructure Debt Serviced

|

5,132

|

5,446

|

|

5,618

|

5,543

|

5,532

|

6,084

|

6,390

|

3.2

|

|

Proposition 58 Early Debt Payments

|

—

|

1,606

|

|

—

|

—

|

—

|

—

|

—

|

—

|

|

Unallocated Proposition 2 Debt Paymentse

|

—

|

—

|

|

695

|

292

|

1,023

|

827

|

963

|

—

|

|

Other Programs

|

6,054

|

7,517

|

|

7,669

|

8,394

|

8,794

|

9,141

|

9,634

|

5.1

|

|

Totals

|

$100,783

|

$110,286

|

|

$110,638

|

$113,829

|

$117,649

|

$120,597

|

$124,376

|

2.4

|

|

Percent change

|

—

|

9.4%

|

|

0.3%

|

2.9%

|

3.4%

|

2.5%

|

3.1%

|

—

|

Education Outlook. Below, we discuss our outlook for Proposition 98, the universities, and the state’s financial aid programs. Our Proposition 98 outlook estimates spending for preschool, elementary and secondary education (commonly referred to as K–12 education), and the California Community Colleges (CCC) combined. Our university outlook estimates spending for the California State University (CSU), the University of California (UC), and Hastings College of the Law (Hastings). Our student financial aid outlook estimates spending for the Cal Grant program, Middle Class Scholarships, and a few small specialized programs.

Proposition 98 Minimum Guarantee for Schools and Community Colleges. State budgeting for schools and community colleges is governed largely by Proposition 98, passed by voters in 1988. The measure, modified by Proposition 111 in 1990, establishes a minimum funding requirement, commonly referred to as the minimum guarantee. Both state General Fund (including Education Protection Account) and local property tax revenue apply toward meeting the minimum guarantee. In addition to Proposition 98 funding, schools and community colleges receive funding from the federal government, other state sources (such as the lottery), and various local sources (such as parcel taxes).

Calculating the Minimum Funding Guarantee. The Proposition 98 minimum guarantee is determined by one of three tests set forth in the State Constitution (see Figure 2). These tests are based on several inputs, including changes in K–12 average daily attendance (ADA), per capita personal income, and per capita General Fund revenue. Though the calculation of the minimum guarantee is formula–driven, a supermajority of the Legislature can vote to suspend the formulas and provide less funding than the formulas require. This happened in 2004–05 and 2010–11. In some cases, including as a result of a suspension, the state creates an outyear obligation referred to as a “maintenance factor.” The state is required to make maintenance factor payments when year–to–year growth in state General Fund revenue is relatively strong. Though in most years the state has provided an amount at or close to the minimum guarantee, the state has discretion to provide any amount above the minimum guarantee.

Figure 2

Calculating the Proposition 98 Minimum Guarantee

|

|

|

Three Tests Used to Determine Minimum Guarantee:

|

|

Test 1—Share of General Fund. Provides roughly 40 percent of state General Fund revenues to K–14 education. The guarantee was determined using this test 4 of the last 26 years.

|

|

Test 2—Growth in Per Capita Personal Income. Adjusts prior–year Proposition 98 funding for changes in K–12 attendance and per capita personal income. The guarantee was determined using this test 13 of the last 26 years.

|

|

Test 3—Growth in General Fund Revenues. Adjusts prior–year Proposition 98 funding for changes in K–12 attendance and per capita General Fund revenues. Generally, this test is operative when General Fund revenues grow more slowly than per capita personal income. The guarantee was determined using this test 7 of the last 26 years.

|

2013–14 and 2014–15 Updates

2013–14 Minimum Guarantee Up Slightly From Budget Act Estimates. Figure 3 compares our updated estimates of the 2013–14 minimum guarantee with what was assumed in the most recently enacted spending plan. Our estimate of the 2013–14 minimum guarantee is up $177 million. Of this amount, $100 million is associated with an upward revision in K–12 ADA. Latest ADA estimates are up about 10,000 ADA (0.17 percent) from budget act estimates. The remainder of the increase is due to 2013–14 General Fund revenue being higher than budget act assumptions. General Fund revenue that counts toward Proposition 98 is up $137 million, with the corresponding increase in the guarantee slightly more than half this amount. Test 3 remains the operative test for calculating the 2013–14 guarantee. Given the increase in the guarantee, the size of the new maintenance factor created is smaller compared to budget act assumptions ($381 million, down from $458 million).

Figure 3

Updating Estimates of 2013–14 and 2014–15 Minimum Guarantees

(Dollars in Millions)

|

|

2013–14

|

|

2014–15

|

|

2014–15

Budget Plan

|

November LAO Estimates

|

Change

|

2014–15

Budget Plan

|

November LAO Estimates

|

Change

|

|

Minimum Guarantee

|

|

|

|

|

|

|

|

|

General Fund

|

$42,731

|

$42,794

|

$63

|

|

$44,462

|

$46,548

|

$2,086

|

|

Local property tax

|

15,571

|

15,686

|

114

|

|

16,397

|

16,656

|

259

|

|

Totals

|

$58,302

|

$58,479

|

$177

|

|

$60,859

|

$63,204

|

$2,345

|

|

Operative Test

|

3

|

3

|

—

|

|

1

|

1

|

—

|

|

K–12 ADA

|

5,982,431

|

5,992,567

|

10,136

|

|

5,975,558

|

5,985,682

|

10,124

|

|

New Maintenance Factor:

|

|

|

|

|

|

|

|

|

Created

|

$458

|

$381

|

–$77

|

|

—

|

—

|

—

|

|

Paid

|

—

|

—

|

—

|

|

$2,583

|

$3,843

|

$1,260

|

2013–14 General Fund Proposition 98 Costs Up Slightly. Though the guarantee is up $177 million, the General Fund share of the guarantee is up only $63 million. This is because our estimate of local property tax revenue also is up from budget act estimates. Local property tax estimates are up a net of $114 million due to various adjustments (some offsetting), including slight changes in regular and supplemental property tax payments as well as updated estimates of revenue shifted to school and community college districts from former redevelopment agencies (RDAs).

2014–15 Minimum Guarantee Up $2.3 Billion From Budget Act Estimates. Figure 3 also compares our updated estimates of the 2014–15 minimum guarantee with what was assumed in the 2014–15 Budget Act. The increase in the 2014–15 guarantee is due primarily to General Fund revenue being higher than budget assumptions. General Fund revenue that counts toward Proposition 98 is up $2.2 billion, yielding a near dollar–for–dollar increase in the guarantee. Test 1 remains the operative test for calculating the 2014–15 guarantee. Given the significant increase in General Fund revenue, the size of the required maintenance factor payment is up notably (now estimated at $3.8 billion, up from the budget act estimate of $2.6 billion). As of the end of 2014–15, we estimate the state’s total outstanding maintenance factor obligation to be $2.7 billion.

2014–15 General Fund Proposition 98 Costs Up Significantly. Of the $2.3 billion increase in the guarantee, the General Fund share increases $2.1 billion and the local property tax share increases $259 million. Similar to 2013–14, the increase in local property tax revenue is due to various relatively minor adjustments.

Increase Sufficient to Trigger Paydown of All Remaining Education Deferrals. Chapter 32, Statutes of 2014 (SB 858, Committee on Budget and Fiscal Review), set forth that if the minimum guarantees for 2013–14 or 2014–15 came in higher than budget act assumptions, the first $992 million in higher–than–assumed growth would be used for paying down remaining education deferrals. We estimate the 2013–14 and 2014–15 minimum guarantees are up a combined $2.5 billion—high enough to trigger the paydown of all remaining deferrals by the end of 2014–15.

$1.5 Billion Available for Other One–Time Purposes. After retiring all education payment deferrals, $1.5 billion would remain available under our forecast for additional Proposition 98 spending in 2014–15. Given the 2014–15 school year is underway, this funding in practical terms is available for one–time purposes. In recent years, the state has prioritized various one–time purposes, including paying down the education mandate backlog, paying down outstanding Emergency Repair Program (ERP) obligations, and supporting new initiatives, such as implementation of the Common Core State Standards and creation of the California Career Pathways Trust. We estimate the state currently has a total of $4.3 billion in unpaid education mandate claims ($3.9 billion for schools and $405 million for community colleges). It has $274 million in outstanding ERP obligations.

Temporary Revenue Surge Would Increase 2014–15 Guarantee. The minimum guarantee in 2014–15 is highly sensitive to changes in General Fund revenue. This is because the state has a large outstanding maintenance factor obligation, Test 1 is operative, and the state has chosen to make maintenance factor payments on top of the Test 1 level. In this situation, the guarantee increases virtually dollar–for–dollar with growth in General Fund revenue. Because of this heightened sensitivity to changes in General Fund revenue, together with the possibility that personal in come tax (PIT) revenue could be higher in 2014–15 than assumed in our main forecast scenario, one of the economic scenarios we considered involved a hypothetical, temporary surge of capital gains revenue in 2014–15. Under this surge scenario, we assume General Fund revenue is above our main scenario by $1.5 billion in 2014–15 and $0.5 billion in 2015–16. The $1.5 billion General Fund increase in 2014–15 results in a $1.5 billion increase in the 2014–15 minimum guarantee. Because the guarantee in 2015–16 builds upon the amount provided the prior year, it too increases by $1.5 billion. Under this scenario, the “bottom line” of the General Fund benefits virtually none from the revenue growth in 2014–15 and is worse off moving forward. (We discuss the temporary revenue surge scenario’s effects on the state budget in more detail in Chapter 5.)

If General Fund revenue in 2014–15 ends up more than $1.6 billion above our main outlook, then the spike protection provisions of the Constitution become operative. As a result, any growth in the guarantee above $1.6 billion in 2014–15 would be excluded from the Proposition 98 calculations in 2015–16. This reduces the 2015–16 guarantee from what it would be otherwise, thereby limiting potential fiscal effects on the rest of the state budget.

2015–16 Budget Planning

2015–16 Guarantee $2.6 Billion Higher Than Updated 2014–15 Guarantee. Under our main scenario (see Figure 4), the minimum guarantee grows from $63.2 billion in 2014–15 to $65.8 billion in 2015–16—an increase of $2.6 billion (4.1 percent). Test 2 is operative, with the increase in the guarantee driven by growth in per capita personal income. We assume K–12 ADA declines by 0.4 percent, but the decline does not affect the guarantee. This is because the Constitution has a two–year hold harmless provision that insulates the guarantee from initial drops in K–12 ADA. (As we assume drops in K–12 ADA every year of the forecast period, the guarantee under our forecast would be affected beginning in 2016–17.) The state would not be required to make a maintenance factor payment in 2015–16 (as the Test 2 and Test 3 levels are very close, with growth in per capita personal income similar to growth in General Fund revenue).

Figure 4

Comparing Proposition 98 Minimum Guarantee Under Three Scenarios

(In Millions)

|

|

2014–15

|

2015–16

|

2016–17

|

|

Main Scenario

|

|

|

|

|

General Fund

|

$46,548

|

$46,422

|

$47,555

|

|

Local property tax

|

16,656

|

19,389

|

20,511

|

|

Minimum Guarantee

|

$63,204

|

$65,810

|

$68,066

|

|

Slowdown Scenarioa

|

|

|

|

|

General Fund

|

$46,548

|

$46,155

|

$44,490

|

|

Local property tax

|

16,656

|

19,389

|

20,355

|

|

Minimum Guarantee

|

$63,204

|

$65,543

|

$64,846

|

|

Temporary Revenue Surge Scenariob

|

|

|

|

General Fund

|

$48,007

|

$47,941

|

$48,870

|

|

Local property tax

|

16,656

|

19,389

|

20,511

|

|

Minimum Guarantee

|

$64,663

|

$67,330

|

$69,380

|

Entire Increase in Guarantee Covered by Higher Local Property Tax Revenue. Under our main scenario, General Fund Proposition 98 costs drop slightly in 2015–16 despite the increase in the guarantee. This is because local property tax revenue is $2.7 billion (16 percent) higher in 2015–16 compared to 2014–15. The large increase in property tax revenue is mainly a result of the following three factors. (The increases identified below are offset by a small reduction in various other components of our property tax estimate.)

- “Triple Flip” Ends. The largest factor is the end of the triple flip. Under the triple flip, the state (1) diverted local sales tax revenue to pay off the state’s Economic Recovery Bonds (approved by voters in 2004 to help close the state budget gap), (2) backfilled cities and counties with school and community college property tax revenue, and (3) backfilled schools and community colleges with state General Fund. Under our main forecast, the state retires the Economic Recovery Bonds by the end of 2014–15. As a consequence, $1.7 billion in local property tax revenue flows back to schools and community colleges in 2015–16.

- Underlying Property Tax Revenue Grows at Healthy Rate. Under our main scenario, we project underlying property tax revenue to increase 5.5 percent in 2015–16. This is slightly lower than the prior–year growth rate (6.1 percent) but still healthy by historic standards. The 5.5 percent increase equates to $950 million in additional local property tax revenue.

- Revenue Shifts From Former RDAs Continue to Increase. We project that ongoing property tax revenue shifted from RDAs to schools and community colleges increases about $200 million from 2014–15 to 2015–16—growing to about $1 billion in 2015–16. (We project one–time shifts relating to former RDA assets will remain roughly flat in 2015–16 before decreasing steadily through the end of the forecast period.)

$6.4 Billion Available for Proposition 98 Priorities. Figure 5 identifies the amount of funding available for Proposition 98 priorities in 2015–16 under our main scenario. With a projected 2015–16 minimum guarantee of $65.8 billion and an ongoing Proposition 98 spending level currently at $59.4 billion, the state has $6.4 billion for its 2015–16 Proposition 98 priorities. The Legislature’s key Proposition 98 decisions in the coming budget cycle likely will revolve around how best to allocate these funds among preschools, schools, and community colleges; how much to designate for ongoing versus one–time purposes; and how much to use for starting new initiatives versus sustaining or extending existing efforts.

Figure 5

Considerable New Proposition 98 Funding Projected for 2015–16

LAO Main Scenario (In Millions)

|

2014–15 Budget Act Spending Level

|

$60,859

|

|

Back out one–time actions:

|

|

|

K–14 deferral paydowns

|

–662

|

|

K–14 mandate backlog

|

–337

|

|

Career Pathways Trust

|

–250

|

|

CCC maintenance and instructional support

|

–148

|

|

CCC Economic and Workforce Development

|

–50

|

|

Preschool quality activities and facility loans

|

–35

|

|

CCC technology infrastructure

|

–1

|

|

Total one–time actions

|

–$1,483

|

|

2014–15 Ongoing Spending

|

$59,377

|

|

Annualize approved preschool slots

|

$15

|

|

New Funds Available in 2015–16

|

$6,419

|

|

2015–16 Minimum Guarantee

|

$65,810

|