Governor's Proposal

Proposed Tax Initiative Is Cornerstone of Governor's Budget Proposal. The administration estimates that the Legislature and the Governor must address a budget problem of $9.2 billion between now and the start of the 2012–13 fiscal year. The cornerstone of the Governor's 2012–13 budget plan is its assumption that voters will approve a temporary increase in income and sales taxes through an initiative that the Governor has proposed be on the November 2012 ballot. The administration estimates the initiative would increase state revenues by $6.9 billion by the end of 2012–13, and generate billions of dollars per year until its taxes expire at the end of 2016. The taxes would be deposited to the General Fund to pay for the state's Proposition 98 school funding obligations, as increased by the initiative, and to help balance the budget by paying for other state programs. The Governor also proposes significant reductions to social services and child care programs and additional state borrowing.

Administration Estimates Plan Would Return State Budget to Balance. The administration estimates the Governor's plan would leave the state with a $1.1 billion reserve at the end of 2012–13 and balanced annual budgets for the next few years. The Governor also proposes that the state take steps to reduce outstanding state budgetary obligations (which he calls a "wall of debt") during the next several years.

Proposed Trigger Cuts if Voters Reject Governor's Tax Initiative. The Governor's proposal requests that the Legislature approve $5.4 billion of "trigger cuts" to take effect on January 1, 2013, if voters do not approve the Governor's tax initiative. Proposition 98 funding for schools and community colleges would bear the brunt of these trigger cuts: $4.8 billion (90 percent) of the total.

LAO Comments

Governor's Plan Would Continue State's Efforts to Restore Budgetary Balance. In 2011, the Legislature and the Governor took significant steps—through ongoing budgetary actions—to begin to restore the state budget to balance. To finish this job, the Legislature still faces a very difficult task for 2012, as the Governor's proposal shows. The Governor's plan envisions multiyear tax increases and significant reductions in social services and subsidized child care programs. As an alternative, if his tax plan is rejected he proposes much larger cuts, aimed largely at schools. If the state chooses either of the Governor's two paths, the state budget would be moved much closer to balance over the next several years.

Revenue Estimates Bigger Question Mark Than Usual. Our revenue estimates—including estimates of state revenue gains from the Governor's proposed initiative—currently are lower than the administration's. Already, California's budget is dependent on volatile income tax payments by the state's wealthiest individuals, and the Governor proposes that these Californians pay more for the next few years. As has become evident in recent years, differing fortunes for these upper–income taxpayers can create or eliminate billions of dollars of projected state revenues. If our current revenue estimates are closer to the target than the administration's, the Legislature will have to pursue billions of dollars more in budget–balancing solutions.

Restructuring Proposals in Education Merit Serious Consideration. The Governor's plan contains major restructuring of the school finance system, community college categorical funding, and education mandates. We think the Governor's restructuring proposals in all these areas would overcome most widely recognized shortcomings of these current systems and institute lasting improvements.

Social Services and Child Care Proposals Have Merit, But Involve Drawbacks. The Governor proposes to reduce General Fund support for California Work Opportunity and Responsibility to Kids (CalWORKs) and subsidized child care—the state's primary sources of cash assistance and work support for low–income families—by a total of about $1.4 billion. His proposal would focus reforms in the CalWORKs program on achieving the goal of emphasizing work. The Legislature may wish to consider whether the proposed reductions to families most in need of support to achieve self–sufficiency are too severe, as well as the Governor's proposal to restrict eligibility criteria and time lines for subsidized child care. Focusing these programs on a different set of objectives and priorities than the Governor would not necessarily eliminate opportunities for budgetary savings, but the savings potential under such alternatives could be less.

Trigger Cut Framework Needs to Be Considered Carefully. Though the Governor's tax initiative would improve the financial outlook of public education over the next several years, his trigger plan would create significant uncertainty for schools, community colleges, and universities in 2012–13. This uncertainty is likely to be particularly problematic for schools, as most will feel compelled to build their 2012–13 budgets assuming the trigger cuts will be implemented. This means schools in 2012–13 likely will implement most, if not all, of the reductions that many hope to avoid. Given this possibility, the Legislature needs to be very deliberate in structuring a workable trigger package. In particular, the Legislature will need to be careful in setting the size of the trigger reduction; determining the specific education reductions to impose; and designing tools to help schools, community colleges, and universities respond to the trigger cuts.

|

The Governor's Budget Proposal

On January 5, 2012, the Governor proposed a 2012–13 state spending plan with $92.6 billion of General Fund expenditures, $39.8 billion of spending from state special funds, and $5.0 billion of bond fund expenditures. In addition, the budget assumes that $73 billion of federal funds flow through state accounts in 2012–13.

The cornerstone of the plan is its assumption that voters will approve the Governor's proposed tax initiative in November 2012. These taxes would be deposited to the General Fund to pay for the state's Proposition 98 school funding obligations, as increased by the initiative, and to help balance the budget by paying for other state programs. Under the administration's estimates, as shown in Figure 1, the state would end 2012–13 with a $1.1 billion General Fund reserve. The budget plan also contains trigger cuts that would take effect if voters reject the Governor's tax proposal.

Figure 1

Governor's Budget General Fund Condition

(Dollars in Millions)

|

|

|

|

Proposed for 2012–13

|

|

|

Actual 2010–11

|

Proposed 2011–12

|

Amount

|

Percent Change

|

|

Prior–year fund balance

|

–$5,019

|

–$3,079

|

–$986

|

|

|

Revenues and transfers

|

93,489

|

88,606

|

95,389

|

7.7%

|

|

Total resources available

|

$88,470

|

$85,527

|

$94,404

|

|

|

Expenditures

|

$91,549

|

$86,513

|

$92,553

|

7.0%

|

|

Ending fund balance

|

–$3,079

|

–$986

|

$1,850

|

|

|

Encumbrances

|

$719

|

$719

|

$719

|

|

|

Reservea

|

–$3,797

|

–$1,704

|

$1,132

|

|

$9.2 Billion Budget Problem Projected for 2012–13

Consists of $4 Billion 2011–12 Deficit, Plus $5 Billion Shortfall for 2012–13. Each year, in assembling the Governor's proposed budget, the administration estimates what revenues and expenditures would be under current tax and expenditure policies. This is called the baseline, or workload, budget forecast. For 2012–13, the administration projects that baseline General Fund revenues are $89.2 billion, while baseline General Fund spending is $94.3 billion. In addition to this prospective annual budget shortfall of over $5 billion for 2012–13, the administration estimates that 2011–12 will end with a General Fund deficit of over $4.1 billion. Combined, the state faces an estimated budget problem of $9.2 billion to address between now and the start of the new fiscal year.

Several Major Differences From LAO's November 2011 Forecast. In our November 2011 publication,

California's Fiscal Outlook, our office estimated that the baseline budget problem for the state's General Fund would total $12.8 billion for 2012–13. This is about $3.6 billion more than the estimated budget problem reflected in the 2012–13 Governor's Budget. The administration's definition of the 2012–13 budget problem differs from ours in several ways:

- Administration's Revenue Forecast. The administration forecasts that baseline General Fund revenues and transfers will be $4.7 billion higher over 2011–12 and 2012–13 combined than indicated in our November 2011 forecast. This is partially offset by the administration's estimate of $803 million less in revenues and transfers than we estimated for the prior year, 2010–11. For the three fiscal years combined, therefore, the Governor's budget forecasts baseline revenues that are over $3.9 billion higher than those forecast by our office in November. The vast majority of our differences during this period are related to our respective forecasts of personal income tax (PIT) revenues.

- Proposition 98 Estimates. The administration's baseline figures are different from those in our November forecast for state General Fund spending for Proposition 98. Specifically, for the 2011–12 and 2012–13 fiscal years combined, the administration's baseline General Fund Proposition 98 estimates are about $1.1 billion lower than our estimates. A number of reasons account for these differences, including the treatment of the realignment revenues, redevelopment revenues, the gas tax swap, and 2011–12 trigger cuts.

- Non–Proposition 98 Spending. Compared to our November forecast, the administration's workload budget estimates for 2011–12 and 2012–13 include a net amount of about $1.4 billion more in non–Proposition 98 General Fund spending. There appear to be a variety of reasons for these differences, such as the administration's estimates of several hundred million dollars of higher General Fund expenses for some health and social services programs and debt service. Contrary to our past practices in developing workload budgets, the administration also includes over $700 million of General Fund expenses to reimburse local governments for the prior–year costs of currently inactive mandates. In addition, we understand that budget proposals to augment some programs are included in the administration's workload budget estimates, such as a proposed $90 million increase to the University of California (UC) budget. Finally, the administration also assumes in its workload budget $500 million of savings from using revenues from the Air Resources Board's (ARB's) auction of "cap–and–trade" greenhouse gas emission allowances to offset unspecified General Fund costs. The Legislature, however, has never explicitly adopted such a policy for the use of cap–and–trade auction revenues, and accordingly, we regard the revenues as a budgetary solution (not as a change in the definition of the problem).

Governor's Budget Proposals

Proposes Over $10 Billion of Budget–Balancing Actions. The Governor proposes over $10 billion of budget–balancing actions to address the administration's estimated $9.2 billion budget problem—leaving the state with a reserve of $1.1 billion at the end of 2012–13. Figure 2 summarizes the administration's estimates of savings or revenue related to the Governor's major proposals. (We list the administration's estimates in every case but two—the cap–and–trade and mandate issues noted above.)

Figure 2

Budget–Balancing Actions Proposed by the Governor

2011–12 and 2012–13 General Fund Benefit (In Millions)

|

Revenue Actions

|

|

|

Increase personal income and sales and use taxes through voter initiative

|

$6,935

|

|

Make permanent the existing tax on Medi–Cal managed care plans

|

162

|

|

Implement changes to unclaimed property program

|

70

|

|

Implement other revenue actions (net)

|

19

|

|

Subtotal

|

($7,186)

|

|

Increased Proposition 98 Costs Due to Proposed Tax Increases

|

–$2,534

|

|

Expenditure Actions

|

|

|

Restructure and reduce CalWORKs and subsidized child care program costs

|

$1,393

|

|

Defer payments to Medi–Cal providers and other related actions

|

682

|

|

Make various Proposition 98 adjustments

|

544

|

|

Use part of cap–and–trade program auction revenues to offset unspecified General Fund costsa

|

500

|

|

Change Cal Grant awards and eligibility requirements

|

302

|

|

Eliminate domestic and related services for certain In–Home Supportive Services recipients

|

164

|

|

Reduce Medi–Cal costs through program efficiencies and other changes

|

160

|

|

Defer payment on pre–2004 local mandate obligationsb

|

100

|

|

Reduce Healthy Families Program managed care rates

|

64

|

|

Reduce various other program costs

|

49

|

|

Implement other fund shifts

|

28

|

|

Subtotalc

|

($3,987)

|

|

Other Actions

|

|

|

Delay loan payments to special funds

|

$631

|

|

Borrow from disability insurance fund to pay costs of federal unemployment insurance loans

|

417

|

|

Use weight fee revenues to offset General Fund costs

|

350

|

|

Suspend county share of child support collections on one–time basis

|

35

|

|

Subtotal

|

($1,432)

|

|

Total

|

$10,070

|

Key Proposals. The budget plan rests predominantly on proposals in three areas, all of which are discussed in greater detail in the sections that follow:

- Plan Assumes Voters Approve Governor's Tax Initiative. The centerpiece of the Governor's budget plan is its assumption that voters approve his initiative proposal to temporarily increase PIT on upper–income filers and sales and use taxes (SUT) for the next several years. The administration estimates that this plan would generate $6.9 billion of revenues to benefit the 2012–13 General Fund budget plan.

- Proposition 98 Proposals. As always, Proposition 98 funding for schools and community colleges is the single largest spending priority in the proposed budget. For 2012–13, the Governor proposes state and local Proposition 98 funding of $52.5 billion—the administration's estimate of the Proposition 98 minimum guarantee. The guarantee reflects the additional revenue assumed to be raised by the Governor's tax initiative. The year–to–year funding increase under the Governor's budget proposal is dedicated largely to reducing the size of existing K–14 payment deferrals. The budget also includes proposals that would dramatically change how the state provides general purpose, categorical, and mandate funding to schools.

- Significant Changes for CalWORKs and Child Care Funding. The Governor proposes to reduce General Fund support for the CalWORKs program and subsidized child care, the state's primary sources of cash assistance and work support for low–income families, for total savings of about $1.4 billion. The savings would be achieved primarily by reducing cash grants to a significant portion of current CalWORKs recipients, further limiting eligibility for subsidized child care and CalWORKs employment services, and reducing payments to child care providers.

Borrowing From State Special Funds. Typical of budgets in recent years, the administration proposes further delays to specified General Fund loan repayments to state special funds. Many special funds are fee–driven accounts eligible to be used for specific public programs. The budget plan assumes $631 million of such loan repayment delays. Examples of these delays include deferrals of General Fund repayments to the Off–Highway Vehicle Trust Fund ($90 million) and the Electronic Waste Recovery and Recycling Fund ($80 million). The budget also proposes to borrow again from the disability insurance fund ($417 million) to pay the state's interest costs to the federal government on its unemployment insurance loan.

Trigger Cuts

Over $5 Billion of Additional Cuts if Voters Reject Tax Measure. The Governor proposes $5.4 billion of trigger cuts to take effect in January 2013 if voters reject his proposed tax measure this November. These trigger cut proposals are summarized in Figure 3. Proposition 98 funding for schools and community colleges would bear the brunt of such reductions: $4.8 billion (90 percent) of the $5.4 billion in total trigger cuts. University and judicial branch appropriations, among others, would see significant reductions in this scenario under the Governor's plan.

Figure 3

Proposed "Trigger" Reductions If Voters Reject Proposed Tax Initiative

2012–13 General Fund Benefit (In Millions)

|

Proposition 98 funding for schools and community colleges

|

$4,837

|

|

University of California

|

200

|

|

California State University

|

200

|

|

Judicial branch

|

125

|

|

CalFire

|

15

|

|

Department of Water Resources flood control programs

|

7

|

|

Department of Fish and Game

|

4

|

|

Department of Parks and Recreation

|

2

|

|

Department of Justice law enforcement programs

|

1

|

|

Total

|

$5,390

|

Impact on Future Years

Smaller Shortfalls Projected. Using its estimates of workload revenues and expenditures, the administration estimates that the state currently faces a future annual budget shortfall of $4.7 billion in 2013–14, $2.9 billion in 2014–15, and $1.9 billion in 2015–16—much reduced from the outyear budget shortfalls projected one year ago. Higher revenue collections and the results of last year's ongoing budgetary actions are responsible for this improvement in the state's fiscal health.

Shortfalls Estimated to Be Eliminated. The administration estimates that the Governor's 2012–13 budget plan would continue last year's progress in returning the state budget to balance. Specifically, the administration's calculations indicate the Governor's plan would "eliminate future budget problems throughout the forecast period under current projections." (The administration's forecast period runs through 2015–16.)

Reducing State Budgetary Obligations. In addition to providing funding for support of existing General Fund program commitments, the Governor proposes to use tax revenues over the next several years to pay down what the administration characterizes as a $33 billion wall of debt. This consists of budgetary obligations such as deferred payments to schools and community colleges, the Economic Recovery Bonds that were used to refinance the state's early–2000s deficit, unpaid local government mandate reimbursements, and loans from state special funds. The 2012–13 Governor's Budget Summary states the Governor's plan would "pay off" this $33 billion by 2015–16.

LAO Comments

Governor's Plan Would Continue State's Efforts to Restore Budgetary Balance. In 2011, the Legislature and the Governor took significant steps—through ongoing budgetary actions—to begin to restore California's state budget to balance. To finish this job, the Legislature still faces a very difficult task in 2012, as the Governor's proposal shows. The administration's major proposed budgetary actions this year are significant—multiyear income and sales tax increases coupled with significant reductions in social services and subsidized child care. As an alternative, if the voters choose not to approve the proposed tax increases, the Governor proposes much larger cuts, aimed largely at schools. If the state chooses either of the Governor's two paths, the state budget would be moved much closer to balance over the next several years.

Revenue Estimates Are a Bigger Question Mark Than Usual. As we discuss later in this report, our revenue estimates for 2011–12, 2012–13, and subsequent years currently are lower than the administration's, and we estimate the revenue gain from the Governor's proposed tax initiative would also be significantly lower. The administration has made a good–faith effort in its revenue and economic forecasting despite the huge uncertainties involved in projecting the state's recovery from an unprecedented economic downturn. Nevertheless, our differences with the administration's estimates for high–income tax filers mean we now project billions of dollars less in state revenues. We will continue to review incoming revenue and economic data and update the Legislature during the next few months.

Already, California's budget is dependent on volatile income tax payments by the state's wealthiest individuals. The top 1 percent of PIT filers pay around 40 percent of state income taxes, the General Fund's dominant funding source. Because the Governor's budget proposal is centered on his idea for these wealthy tax filers to pay more, the state would become more dependent on this uncertain revenue source. For this reason, revenue estimates are an even bigger question mark than usual for the Legislature this year. As we have learned in past years, differing fortunes for upper–income taxpayers can quickly create or eliminate billions of dollars of projected state revenues. If our current revenue estimates are closer to the target than the administration's, the Legislature will have to pursue billions of dollars more in budget–balancing solutions.

Restructuring Proposals in Education Merit Serious Consideration. The Governor's package also contains major restructuring of the K–12 finance system, community college categorical funding model, and education mandate system. In all three cases, the state's existing systems are widely recognized as having longstanding, fundamental shortcomings. We think the Governor's restructuring proposals in all three areas would overcome most of these shortcomings and institute lasting improvements. As such, we recommend the Legislature adopt the Governor's basic restructuring approaches. The Legislature, however, might want to make some modifications to specific proposals. For example, the Legislature might want to change the amount of mandate block grant funding provided or the specific mix of mandated programs that are eliminated versus made discretionary.

Now Not the Time for Major New Programs or Program Expansions. We agree with the Governor's assessment that now is not the time to initiate major new programs or authorizing program expansions. The Governor's plan contains associated proposals that together would help lower costs by $300 million. Of greatest magnitude, we recommend the Legislature adopt the Governor's proposal not to initiate the transitional kindergarten program set to go into effect beginning in 2012–13. Not initiating this program yields $224 million in associated revenue limit savings. We also recommend the Legislature adopt the Governor's proposals to halt the Cal Grant expansions that would otherwise come about through loosened transfer entitlement rules and cohort default rate limits beginning in 2012–13. These two proposals would result in state savings of more than $70 million.

Social Services and Child Care Proposals Have Merit, But Involve Trade–Offs. The Governor's budget proposes to reduce General Fund support for CalWORKs and subsidized child care—the state's primary sources of cash assistance and work support for California's low–income families—by a total of about $1.4 billion. The Governor's proposal recognizes that, given current funding constraints, it is difficult to fully achieve existing goals of the CalWORKs program. Accordingly, his proposal would focus reforms in the CalWORKs program on achieving the goal of emphasizing work.

Although we find the Governor's CalWORKs and child care proposals have some advantages, they also involve potential trade–offs. Most clearly, the reductions proposed by the Governor would have significant negative impacts on many of California's low–income families. Regarding CalWORKs, the Legislature may wish to consider whether reductions made to families most in need of support to achieve self–sufficiency would be too severe. Similarly, the Legislature may want to consider whether the Governor's proposal too severely restricts eligibility criteria and time lines for subsidized child care. More generally, the Legislature should consider whether focusing CalWORKs and subsidized child care primarily on supporting efforts of low–income families to obtain employment is consistent with its priorities or whether other objectives are also important. Focusing these programs on a different set of objectives and priorities than the Governor would not necessarily eliminate opportunities for budgetary savings; however, the potential for savings could be less and there could be trade–offs in other areas of the budget.

Legislature Needs to Carefully Consider Any Trigger Framework. Though the Governor's tax initiative would improve the financial outlook of public education over the next several years, his trigger plan would create significant uncertainty for schools, community colleges, and universities in 2012–13. This uncertainty is likely to be particularly problematic for schools, with most schools feeling compelled to build their 2012–13 budgets assuming the trigger cuts are implemented (that is, assuming only the state revenue that they are assured of receiving). This means schools in 2012–13 out of necessity likely will be implementing most, if not all, of the reductions that many would be hoping to avoid. Given this is the case, the Legislature needs to be very deliberate in structuring a trigger package. In particular, the Legislature should be careful in setting the size of the trigger reduction; determining the specific education reductions to impose; and designing tools to help schools, community colleges, and universities respond to the triggers. The Legislature also needs to assess whether specific trigger plans are workable. One major consideration, for example, is how the state treats realignment sales tax revenues in calculating the Proposition 98 minimum guarantee.

Economic Forecast

Summer's Economic Slowdown Apparently Temporary. The administration's 2012 forecast reflects an economy that has rebounded from its generally disappointing performance this past summer. Economic weakness during the summer months was primarily due to the reaction of financial markets to the European debt crisis and congressional deadlock over the federal debt ceiling. Employment and other economic news improved during the fall and early winter months. We agree with the administration that a return of the U.S. economy to recession is unlikely now. The U.S. and California economies are poised to continue slow recoveries.

Administration's Forecast for 2012. As shown in Figure 4, the administration's new economic forecast is similar to, but slightly more pessimistic than, our November 2011 economic forecast. Both forecasts are based on the assumption that Congress extends the partial employee payroll tax holiday and emergency unemployment insurance benefits beyond their current expiration dates next month. Absent these extensions, economic performance in the immediate future probably would be weaker than shown in Figure 4.

Figure 4

Comparing the Administration's Economic Projections With LAO's November 2011 Forecast

|

|

2012

|

|

2013

|

|

LAO Forecast—November 2011

|

Governor's Budget Forecast—January 2012

|

|

LAO Forecast—November 2011

|

Governor's Budget Forecast—January 2012

|

|

United States

|

|

|

|

|

|

|

Percent change in:

|

|

|

|

|

|

|

Real gross domestic product

|

2.1%

|

1.7%

|

|

2.8%

|

2.5%

|

|

Wage and salary employment

|

1.0

|

0.9

|

|

1.7

|

1.4

|

|

California

|

|

|

|

|

|

|

Percent change in:

|

|

|

|

|

|

|

Personal income

|

4.1%

|

3.8%

|

|

4.5%

|

4.1%

|

|

Wage and salary employment

|

1.3

|

1.3

|

|

2.1

|

1.8

|

|

Housing permits (thousands)

|

61

|

52

|

|

77

|

80

|

|

Taxable sales (billions)

|

$537

|

$538

|

|

$579

|

$573

|

Modest Strengthening in 2013 Expected. The administration's economic forecast projects cautious, but steadily expanding, growth in 2013. More robust growth is being held back by lingering foreclosure activity and continued price declines in the California housing market, as well as relatively weak growth in real incomes. The administration, however, expects the economy to begin expanding more rapidly in 2013, which is consistent with our recent forecast.

The administration observes that the California economy is being pulled along, in part, by healthy wage and salary growth in high–income labor markets—most notably the technology sector in the Silicon Valley and other areas of the state. Consumer spending also has picked up in California, as individuals and firms return to more normal consumption behavior fueled, in part, by pent–up demand. The Governor's forecast of taxable sales aligns closely with our November forecast. Although we do not project consumption to weaken, there is some risk to the administration's and our office's taxable sales forecasts because consumers and businesses are contending with low credit availability and weak, albeit improving, consumer confidence.

Uncertainty About Federal Policies in 2012 and Beyond. A number of federal policy changes scheduled—or assumed—to take place in 2012 and 2013 could alter the trajectory of economic growth projected by the administration and our office. As noted above, the administration's forecast assumes Congress will extend the payroll tax holiday and unemployment benefits through 2012. In addition, various tax reductions enacted under the prior federal administration (and extended under the current administration) are scheduled to expire at the end of 2012, and both of our economic forecasts now anticipate these tax cuts will be extended. Automatic congressional spending cuts, known as sequestration, also are set to occur in early 2013, and the President recently announced a broad proposal to shrink the size of the Army, the Marine Corps, and other parts of the U.S. military, which could ripple through the national economy. The U.S. Postal Service—a major governmental employer—also must implement large spending reductions in the coming years.

Most economic forecasts—including our own and the administration's—assume that Congress and the executive branch agree to compromises in the coming months to mitigate some of the near–term negative economic effects of these changes. Failure of Congress and the President to agree to such policies could, therefore, negatively affect the economy during the next few years. Over the longer term, the federal government's deep fiscal imbalances will require significant changes to federal programs and taxation that could affect large segments of both the U.S. and California economies.

Economic and Fiscal Forecasting Especially Challenging Now. There is considerable uncertainty in the administration's forecast—as well as our November 2011 forecast—regarding the short– and medium–term path for the economy. In addition to the difficulty in predicting federal policies, there is also significant uncertainty due to the nature of the historically deep recession from which California and the nation are recovering. There is limited precedent with which to make sound judgments about how the economy will proceed in the coming years. Particularly significant in the context of California budgetary forecasting is the difficulty in projecting the income prospects of high–income tax filers, who experienced a disproportionately large drop in income—relative to other groups of taxpayers—during the recession. These Californians are in the state's top marginal income tax brackets and pay a very large share of state tax revenues. Largely because their income—dominated by sales of stocks, bond, and other assets—is volatile, state income tax collections are volatile too.

Revenue Forecast

As shown in Figure 5, the administration's new revenue forecast projects that the General Fund will record $88.6 billion of revenues in 2011–12 and $95.4 billion in 2012–13, including revenue from the Governor's tax initiative proposal. The administration expects that the Governor's tax proposal, if approved by voters, would generate $2.2 billion of revenues attributable to 2011–12 and $4.7 billion in 2012–13. Most of those revenues result from the PIT part of the Governor's tax proposal.

Figure 5

Governor's Budget General Fund Revenue Forecast (Including Revenue Proposals)

(In Billions)

|

|

2011–12

|

2012–13

|

|

Personal income tax

|

$54,186

|

$59,552

|

|

Sales and use tax

|

18,777

|

20,769

|

|

Corporation tax

|

9,479

|

9,342

|

|

Subtotals, "Big Three" Taxes

|

($82,442)

|

($89,663)

|

|

Other revenues

|

$4,751

|

$4,885

|

|

Net transfers and loans

|

1,413

|

841

|

|

Total Revenues and Transfers

|

$88,606

|

$95,389

|

Administration Forecasts Higher Revenues Than Our Office Did in November. Figure 6 compares the administration's baseline revenue forecast (that is, the current–law revenue forecast excluding revenue from the Governor's tax and other revenue proposals) with our November 2011 current–law forecast. For 2010–11, the administration's more up–to–date information on revenue accruals and transfers and loans shows that the General Fund received $803 million less than we assumed in November. For 2011–12 and 2012–13, however, the administration forecasts significantly higher baseline revenues than we did two months ago. In 2011–12, the administration's baseline forecast is higher than ours by $1.5 billion, and in 2012–13, its forecast is higher than ours by $3.2 billion. Over the three fiscal years combined, the administration forecasts $3.9 billion more in baseline General Fund revenues than we did.

Figure 6

Administration's Baseline Revenue Forecasts Differ From LAO'sa

General Fund (In Billions)

|

|

2010–11

|

|

2011–12

|

|

2012–13

|

|

|

LAO November Forecast

|

Governor's Budget Forecast

|

|

LAO November Forecast

|

Governor's Budget Forecast

|

|

LAO November Forecast

|

Governor's Budget Forecast

|

|

Personal income taxb

|

$49,779

|

$49,491

|

|

$50,812

|

$51,937

|

|

$53,134

|

$56,025

|

|

Sales and use tax

|

26,983

|

26,983

|

|

18,531

|

18,777

|

|

19,980

|

19,595

|

|

Corporation tax

|

9,838

|

9,614

|

|

9,483

|

9,479

|

|

9,432

|

9,342

|

|

Subtotals, "Big Three" Taxes

|

($86,600)

|

($86,088)

|

|

($78,826)

|

($80,193)

|

|

($82,546)

|

($84,962)

|

|

Other revenues

|

$5,795

|

$5,913

|

|

$4,486

|

$4,730

|

|

$4,540

|

$4,788

|

|

Net transfers and loans

|

1,897

|

1,488

|

|

1,451

|

1,386

|

|

–1,048

|

–529

|

|

Total Revenues and Transfers

|

$94,292

|

$93,489

|

|

$84,764

|

$86,309

|

|

$86,038

|

$89,221

|

|

Difference—Governor's Budget Minus LAO November Forecast

|

–$803

|

|

$1,545

|

|

$3,183

|

Sizable PIT Forecasting Differences, Particularly for High–Income Taxpayers. Of the $3.9 billion difference in our baseline revenue projections, $3.7 billion can be attributed to our different PIT forecasts. In recent weeks, since the Department of Finance (DOF) announced its updated 2011–12 "trigger" forecast, we have devoted significant time to analyzing these differences. While our respective forecasting models differ—making it difficult to assess the reasons for all of our differences—it seems clear that our office's forecasting models currently assume that high–income tax filers will receive significantly less income than that assumed in DOF's models. Our differences seem particularly significant beginning in tax year 2012, which affects General Fund PIT revenue forecasts for both 2011–12 and 2012–13. It appears that our differences most likely include those in various categories of income for wealthier filers, including wages and salaries, business–related income, retirement income, and the exceptionally volatile income category of capital gains.

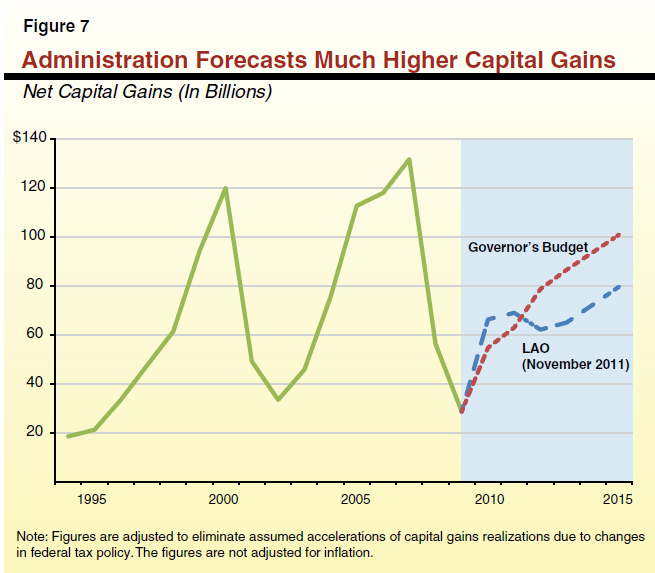

Concerns About the Administration's Capital Gains Forecast. In its new forecast, DOF projects capital gains realized by California tax filers to rise to $96 billion in 2012. By contrast, our office's November forecast assumed $62 billion of 2012 capital gains. This $34 billion difference accounts for about $3 billion of our organizations' differing PIT baseline forecasts in 2011–12 and 2012–13 combined. A part of this $3 billion revenue difference results from our differing assumptions concerning federal tax policy. In contrast to our forecast, DOF's revenue forecast assumes that the 2001 cuts in federal tax rates will be allowed to expire as scheduled at the end of 2012. This expiration then is assumed to cause investors to accelerate realization of capital gains that they otherwise would take in 2013, thereby "shifting" a portion of capital gains income forward from 2013 to 2012. In this forecast, for the first time, DOF also has shifted an additional part of 2013 capital gains to 2012 based on assumed investor behavior to shield income from higher Medicare taxes scheduled to take effect next year. These various shifts tend to reduce projected state revenues for 2013–14 and increase them in earlier years.

We are concerned that the administration's current method of forecasting high–income filers' income—especially capital gains—tends to overestimate state revenue growth from the PIT over the next few years, including revenue growth that would result from the Governor's tax initiative. Figure 7 shows historical net capital gains of California resident tax filers, as well as both our office's November 2011 estimates and DOF's current estimates. In this figure, we have adjusted both sets of estimates to eliminate the federal tax–related shifts described above in order to show our underlying forecasting differences. With these adjustments, DOF forecasts roughly $20 billion more of capital gains than our office in each year beginning in 2012. This results in DOF forecasting roughly $2 billion more in annual baseline revenues than we do going forward. Over time, DOF assumes capital gains begin to approach levels only experienced during previous stock market and real estate "bubbles." We advise the Legislature to regard these estimates with some caution.

As we discussed in our November report,

California's Fiscal Outlook, Franchise Tax Board (FTB) data on the state income tax base lags by one to two years, such that preliminary data on 2010 income tax returns only recently has emerged. Since publication of our report, FTB preliminary data for 2010 suggests that our November 2011 forecast of capital gains for that tax year was too high. This, in turn, may have resulted in our forecast of capital gains for subsequent years being somewhat too high. We expect to adjust for these differences—as well as other differences that may offset the downwardly revised capital gains estimates—in our next revenue forecast (slated for release in late February).

Forecasting capital gains and other income of wealthier Californians is extremely difficult. These forecasts can change rapidly during the course of any given year due to abrupt changes in asset markets and the overall economy, which, as we have seen in recent years, are not all that rare. Yet, both DOF and our office utilize similar assumptions for future stock market and home price growth in our models, and our office has found that movements in these asset prices, combined with simple time trends, have explained more than 80 percent of the annual variation in the major categories of capital gains over the last two decades. We will continue to examine economic and tax collection data in the coming months to try to reconcile our forecasting differences with DOF.

December 2011 Income Taxes Lagged Estimates. Using data from FTB and the Employment Development Department (EDD), which administers PIT withholding, our office and DOF track PIT and corporation tax (CT) agency cash receipts daily. December and January are significant months for collections of PIT estimated payments, which are paid largely by high–income filers. December 2011 was a disappointing month for PIT collections (as well as CT collections). Preliminary FTB data show that estimated PIT payments and PIT withholding lagged prior–year collections for the same month. They also lagged the amount of expected revenues for December 2011 assumed in DOF's June 2011 budget forecast of monthly receipts. (The DOF's new revenue forecast has the effect of increasing the average projected PIT and CT receipts for the rest of 2011–12 above the levels in the June 2011 forecast. This makes it all the more notable that December PIT and CT revenues were over $900 million lower than the June forecast.)

It is too early to make definitive judgments about what these most recent PIT collection trends mean. In particular, receipts over the next two weeks will be an important early indication as to whether our office's or DOF's high–income taxpayer forecast is closer to target. Additional data will emerge in the coming months, particularly during the all–important revenue collection month of April. Negative trends like those we have seen recently can reverse themselves quickly.

The Facebook Effect. Facebook Inc., a privately held company headquartered in Palo Alto, may proceed with an initial public offering (IPO) of its stock in 2012. Facebook reportedly is considering issuing $10 billion of stock in an IPO that would value the company at over $100 billion. Other companies also are considering IPOs in the coming years.

In the coming months, the state's revenue forecasts will need to be adjusted somewhat to account for the possibility of hundreds of millions of dollars of additional revenues related to the Facebook IPO. These revenues could affect the budgetary outlook beginning in 2012–13. We caution that it will be impossible to forecast IPO–related state revenues with any precision, and it is likely that little information about the state revenue gain from the Facebook IPO will be available before investors file tax returns in April 2013. (Even then, due to the confidentiality of individual taxpayer information, we are unlikely to know precisely how much state revenues increased due to Facebook's IPO.)

In considering the size of the Facebook IPO effect in the coming months, revenue forecasters will have a difficult task. Our office's income models are based on historical trends and, therefore, already assume that some level of IPO activity occurs for California companies each year. Moreover, in our recent forecasts, our office has deliberately built in "extra" capital gains (above those generated by our model) in 2010, 2011, and 2012 to try to account for a variety of factors, including the surprisingly strong PIT receipts in some recent months. Finally, Facebook–related capital gains likely will prove to be a relatively small percentage of California's overall capital gains in 2012. If the stock market as a whole has an unusually strong or weak year, that fact could change forecasted capital gains up or down by much more than the positive Facebook effect.

Revenue Proposals

Governor's Tax Initiative Proposal. The Governor's 2012–13 budget plan assumes passage of his initiative proposal for temporary PIT and SUT increases. Specifically, the Governor proposes to increase PIT rates for upper–income Californians for five years (2012 through 2016) and a 0.5 percent increase in the statewide SUT for four years (2013 through 2016). The administration forecasts that this measure would generate $6.9 billion that would be available for the Legislature's consideration during the 2012–13 budget process—$2.2 billion in 2011–12 revenues and $4.7 billion of 2012–13 revenues. All of the 2011–12 revenue and $3.5 billion of the 2012–13 revenue would result from the higher PIT rates.

As we discussed in our recent analysis of the Governor's initiative proposal, our current estimates of the revenue impact of his initiative proposal are lower than the administration's. Currently, we forecast that the proposal would generate $4.8 billion for the 2012–13 budget process, or $2.1 billion less than the administration's estimate. Our estimates of the initiative's revenue increases in later years also are lower than the administration's. The reasons for our lower estimates are essentially the same as the reasons for our differences in baseline revenues described above.

Both our office and the administration agree that the initiative revenues will likely prove to be volatile, given that a large portion of them will relate to upper–income tax filers' capital gains and other nonwage income.

Accrual Proposal. The administration proposes that the budget include a control section authorizing a new method of accruing revenues for tax policy changes enacted in 2012. This proposed change, similar to the administration's rejected accrual change proposal from last year, would apply to the Governor's tax initiative proposals but not other tax revenues.

We discussed last year's proposal in our January 2011 publication,

The 2011–12 Budget: The Administration's Revenue Accrual Approach. Similar to what we described in that report, the accrual of a portion of the initiative tax revenues to 2011–12 would tend to decrease the state's 2012–13 Proposition 98 minimum school funding guarantee. While we find some merit in the administration's proposed accrual approach, we continue to have concerns that it is not being applied uniformly across all revenues. We recommend that the Legislature pass a law requiring DOF to develop and regularly update a clear, transparent summary of the state's accrual methodologies, and we recommend that the state move toward consistent application of accepted accrual techniques across all tax revenues and spending.

Tax Administration

Proposed Department of Revenue. The 2012–13 Governor's Budget Summary mentions that the Governor will propose merging FTB and the tax administration components of EDD into a new Department of Revenue (DOR). Based on the potential benefits for the state and taxpayers from having a single tax administration entity, our office has long advocated some sort of tax agency merger. In our view, a successful merger would require detailed preparatory work by the tax agencies involved and a significant amount of time to implement merger–related efficiencies gradually.

In addition to merging FTB and the tax administration sections of EDD, we urge the Legislature to consider merging the bulk of the State Board of Equalization's (BOE) tax administration efforts into the proposed DOR. The State Constitution mandates that certain limited tax administration functions remain with the elected BOE, but legislative action could allow most of BOE's functions to be transferred to the proposed DOR. We believe that long–term efficiencies are possible from a carefully planned merger of this type. In addition, taxpayers could benefit from having one, coordinated tax agency with which to interact. Other departments with revenue collection functions also could be considered for inclusion in DOR in the future.

Proposition 98 funds K–12 education, the California Community Colleges (CCC), preschool, and various other state education programs. The Governor's budget increases total Proposition 98 funding by $4.9 billion, or 10 percent between the current year and the budget year. As shown in Figure 8, the year–over–year increases in Proposition 98 General Fund for schools and community colleges are larger—15 percent and 14 percent, respectively, with local property tax revenues estimated to be virtually flat. The funding levels reflected in Figure 8 assume voters approve the Governor's November 2012 ballot measure to raise sales and income tax rates temporarily, with a portion of the associated revenue increase benefiting K–14 education.

Figure 8

Proposition 98 Funding

(Dollars in Millions)

|

|

2011–12 Revised

|

2012–13 Proposed

|

Change From 2011–12

|

|

Amount

|

Percent

|

|

K–12 Education

|

|

|

|

|

|

General Fund

|

$29,329

|

$33,755

|

$4,426

|

15%

|

|

Local property tax revenue

|

12,891

|

12,908

|

17

|

—

|

|

Subtotals

|

($42,220)

|

($46,663)

|

($4,443)

|

(11%)

|

|

California Community Colleges

|

|

|

|

|

|

General Fund

|

$3,217

|

$3,683

|

$465

|

14%

|

|

Local property tax revenue

|

2,107

|

2,101

|

–6

|

—

|

|

Subtotals

|

($5,324)

|

($5,784)

|

($459)

|

(9%)

|

|

Other Agencies

|

$83

|

$80

|

–$2

|

–3%

|

|

Totals, Proposition 98

|

$47,627

|

$52,527

|

$4,900

|

10%

|

|

General Fund

|

$32,629

|

$37,518

|

$4,889

|

15%

|

|

Local property tax revenue

|

14,998

|

15,009

|

11

|

—

|

Makes Various Adjustments to Minimum Guarantee. For 2012–13, the Governor funds at the minimum guarantee ($52.5 billion) assuming approval of his tax measure (which accounts for more than $2 billion of the increase in the guarantee). To arrive at this guarantee, the Governor adjusts or "rebenches" the guarantee in three notable ways. Of greatest magnitude, the Governor permanently rebenches the minimum guarantee to account for a shift in property tax revenues (of approximately $1 billion annually) from redevelopment agencies to school districts and community colleges. By rebenching the guarantee for this shift, the state achieves associated General Fund savings. In addition, the Governor proposes to eliminate existing provisions that require the state to rebench for the "gas tax swap" adopted by the Legislature in 2011. The gas tax swap eliminated the sales tax on gasoline (previously included in the Proposition 98 calculation) and replaced it with an increase in the excise tax on gasoline (excluded from the Proposition 98 calculation). With the rebenching, the minimum guarantee was unaffected by the gas tax swap. Without the rebenching, the minimum guarantee drops by $544 million. Thirdly, the Governor proposes to recalculate last year's rebenchings using the "1986–87 methodology." This change (which applies to child care, student mental health, and redevelopment revenues) increases the 2012–13 guarantee by $217 million.

Makes Two Additional Adjustments to Minimum Guarantee Under Back–Up Plan. If the Governor's tax measure is not adopted, the Governor has a back–up plan that contains $4.8 billion in spending reductions to schools and community colleges, including $2.4 billion in programmatic reductions. These programmatic reductions are linked with the Governor's proposal to include K–14 general obligation bond debt–service payments within the Proposition 98 minimum guarantee. To account for this shift, the Governor proposes a rebenching of the minimum guarantee, resulting in an increase of $200 million. Since the cost of debt–service payments ($2.6 billion) far exceeds the increase in the minimum guarantee from the rebenching, the Governor proposes $2.4 billion in programmatic Proposition 98 reductions to maintain spending at the guarantee. His estimate of the guarantee also excludes the realignment–related sales tax revenue. How the state should treat these revenues is currently being litigated.

Major Proposals

As shown in Figure 9, the year–to–year funding increase under the Governor's basic plan would be dedicated primarily to backfilling one–time solutions from last year, covering a slight increase in the K–12 student population (estimated to be 0.35 percent) for a few select K–12 programs, and paying down existing K–14 deferrals. The plan provides no cost–of–living adjustment for any K–14 education program. (Providing the projected 3.17 percent COLA for K–14 programs would cost $1.8 billion.) It also provides no enrollment growth funding for CCC. Moreover, it contains essentially no programmatic augmentations while containing a few notable programmatic reductions. The Governor's plan also contains a set of proposals to restructure the state's K–12 and CCC funding models. Below, we highlight the Governor's major Proposition 98 spending proposals as well as his major restructuring proposals. (The Governor also proposes significant reductions for the California Department of Education [CDE]–administered child care programs, described in the next section of this report.)

Figure 9

2012–13 Proposition 98 Spending Changes

(In Millions)

|

|

|

|

Technical

|

|

|

Backfill one–time actions

|

$2,440

|

|

Make revenue limit technical adjustments

|

162

|

|

Fund revenue limit growth

|

158

|

|

Backfill Proposition 63 mental health funding

|

99

|

|

Backfill CCC fee revenue decline

|

97

|

|

Make other technical adjustments

|

–182

|

|

Subtotal

|

($2,775)

|

|

Policy

|

|

|

Pay down K–12 deferrals

|

$2,151

|

|

Pay down CCC deferrals

|

218

|

|

Create K–12 mandate block grant

|

98

|

|

Create CCC mandate block grant

|

12

|

|

Do not initiate Transitional Kindergarten program

|

–224

|

|

Reduce preschool funding

|

–58

|

|

Swap one–time funds

|

–57

|

|

Eliminate Early Mental Health Initiative

|

–15

|

|

Subtotal

|

($2,125)

|

|

Total

|

$4,900

|

Dedicates Funding Increase to Paying Down Deferrals. The largest component of the Governor's plan is to pay down $2.4 billion in existing K–14 deferrals ($2.2 billion for school districts and $218 million for CCC apportionments). This funding would reduce the need for school districts and community colleges to borrow to support operations while awaiting the state's late payments. From both a state and a local perspective, paying down deferrals helps to realign funding with expenses. The proposal would reduce the state's outstanding deferrals from $10.4 billion to $8 billion. Because this funding would not be intended to increase programmatic activities, K–12 per–pupil programmatic funding under the Governor's basic plan is roughly flat year over year.

Suspends K–12 Categorical Program Requirements, Phases In Weighted Student Formula Over Five Years. To assist with local budget constraints, the state has temporarily suspended requirements for about 40 categorical programs. The Governor proposes to suspend requirements for up to ten additional programs—essentially phasing out most existing categorical programs beginning in 2012–13. (A few categorical programs—including special education, child nutrition, and the After School Education and Safety program—would remain.) In lieu of the current revenue limit and categorical program model, the Governor proposes that all districts and charter schools receive an equal base per–pupil amount, plus additional general purpose funding intended to serve their disadvantaged students. Specifically, for every dollar districts/charter schools receive for a student, they would get an additional 37 cents if the student were poor and/or an English Learner. Districts/charter schools with large proportions of these disadvantaged student populations also would receive supplemental "concentration" funding. Perhaps as soon as 2013–14, the administration plans to add a performance component to the weighted student formula, which would provide fiscal incentives for districts to improve or sustain high academic performance. Districts would have local discretion as to how to spend weighted student formula funding. The Governor proposes to transition to the new formula over a five year period, with implementation beginning in 2012–13.

Proposes More Flexibility for CCC Categorical Programs. Under current law, 11 of community colleges' 21 categorical programs are included in a "flex item." Through 2014–15, districts are permitted to transfer funds from categorical programs in the flex item to any other categorical purpose. As part of his emphasis on flexibility, the Governor adds seven currently protected categorical programs to the flex item. Under the Governor's proposal, funding for the remaining three CCC categorical programs (Disabled Students Program, Foster Care Education Program, and Telecommunications and Technology Services) would remain restricted.

Replaces Existing K–14 Mandate System With New Block Grant. The Governor proposes a number of K–14 mandate–related changes. Under the Governor's package of changes, the existing mandate system essentially would be replaced with a discretionary block grant.

- Eliminates More Than Half of Existing Mandates. The Governor proposes to eliminate 31 of 57 existing education mandates. The mandates proposed for elimination include two of the costliest mandates—one relating to high school science graduation requirements and one relating to behavioral intervention plans for special education students.

- Suspends Remaining Mandates. The remaining 26 education mandates would be suspended. (Though suspended, school districts and community colleges still would need to undertake these activities if they wanted to access the block grant funding described below.)

- Creates Block Grant. The Governor proposes to create a new, discretionary "mandate block grant." His budget provides $200 million ($178 million for school districts, $22 million for community colleges) for the block grant. School districts and community colleges that choose to receive block grant funding would receive a per–student allocation. As a condition of receiving block grant funding, recipients would be required to complete the 26 sets of activities still deemed to be high priorities. The administration indicates it will establish some auditing and/or compliance monitoring process to ensure grant recipients undertake the required activities.

Does Not Initiate Transitional Kindergarten Program. In response to concerns that California was encouraging children to start attending school before they were developmentally ready, the Legislature recently passed legislation prohibiting children under five years of age from enrolling in kindergarten (unless a parental waiver was obtained). The change is phased in, moving the birthday cutoff back from December 1 to September 1, by one month at a time over three years, beginning with the shift to November 1 in 2012–13. This change reduces the kindergarten population by about 125,000 students and yields estimated revenue limit savings of $224 million in 2012–13. The Legislature, however, redirected these savings to fund a new Transitional Kindergarten program, which is to offer an additional year of public school to the children who will just miss the new kindergarten cutoff. This program also is phased in over three years, beginning 2012–13 for those children turning age five between November 1 and December 1. By proposing not to initiate this new program, the Governor achieves $224 million in 2012–13 savings, growing to roughly $675 million in annual savings (by 2014–15, when the program otherwise would have been fully implemented).

Includes 2012–13 Midyear Trigger Reductions. The Governor's back–up plan includes $4.8 billion in trigger reductions if his ballot measure is rejected by voters. The Governor proposes to implement these reductions by rescinding the $2.4 billion K–14 deferral pay–down and reducing general purpose funding for schools and community colleges by $2.4 billion. Paying down existing deferrals is intended to have no associated programmatic effect but the reduction in general purpose funding would reflect a base cut. Under this scenario, K–12 per–pupil programmatic funding would decline 6 percent from the current–year level.

Several Components Merit Serious Consideration

The Governor's plan addresses several of the longstanding, fundamental, widely recognized problems with the state's K–12 and community college funding systems. Though the Legislature might find ways to improve upon the Governor's specific restructuring plans, we recommend the Legislature adopt the Governor's basic restructuring approaches (regardless of the state's revenue situation). In this fiscal climate, particularly with so many existing outstanding Proposition 98 obligations, we also recommend the Legislature adopt the Governor's proposal to avoid initiating a major new program beginning in 2012–13. We discuss these particular aspects of the Governor's plan in more detail below.

More K–12 Categorical Flexibility, New Funding Model Moving in Right Direction. Most experts and advocates at both the state and local levels agree that the state's current school funding system is overly complex, inequitable, inefficient, and highly centralized. Consequently, the Governor's proposal to simplify and streamline the existing methods for allocating funding deserves both credit and serious consideration. We believe several components of the proposal are particularly sound, including immediate increases in categorical flexibility, a moderate phase–in period for the new formula, and additional funding "weights" for disadvantaged students. The Legislature could use this basic structure but make some modifications to ensure its important policy priorities are preserved. For example, the state could maintain some general requirements to ensure additional funds actually are spent on disadvantaged students. Alternatively, rather than one general purpose weighted formula, the Legislature could consolidate all K–12 funding into a few thematic block grants.

Proposal to Expand CCC Categorical Program Flexibility Has Promise, But More Detail Is Needed. The Governor's plan to expand the number of categorical programs in the CCC flex item also appears to be consistent with recommendations we have made in the past. By placing additional programs in the flex item, districts likely would have more freedom to decide for themselves how best to allocate funds to targeted purposes. This could help districts operate their services more efficiently and effectively, such as by consolidating various separately administered student counseling programs into one comprehensive program. The Governor's full proposal, however, is not yet clear. Specifically, the administration has indicated that it intends to introduce provisional language that will attach certain conditions to how districts spend such funds. The Legislature will need to have this language before deciding on the merits of the Governor's proposal.

Mandate Approach Has Several Strong Points. As with the state's existing K–12 categorical funding system, the state's existing K–14 mandate system also is widely recognized as having fundamental problems. A broadly representative mandate work group that the Legislature asked our office to convene last year identified nine serious flaws with the state's existing system, including significant administrative burden for districts, wide variation in reimbursement rates for completing the same sets of activities, reimbursement regardless of outcomes, and very high disallowance rates of audited claims. The Governor's restructuring approach addresses many of these problems. It provides upfront, standardized per–student funding for all districts using a relatively simple allocation process that does not involve extensive paperwork. Also, by first eliminating all nonessential activities, the state is able to reduce associated costs, thereby freeing up resources that can be used to fund districts that do not participate in the existing process (one of the main factors that drives up the cost of most restructuring proposals). Though the Legislature might want to make some changes to the Governor's proposal (for example, eliminating/suspending a different set of mandates and/or adjusting the amount of block grant funding provided), we recommend the Legislature adopt the Governor's restructuring approach.

Adopt Kindergarten Proposal, Prioritize Access to Preschool for Low–Income Children. Given the major funding and programmatic reductions districts have experienced in recent years—and the potential for additional reductions if the November election does not result in new state revenue—we agree with the Governor's assessment that now is not the time to initiate major new programs. As such, we recommend the Legislature adopt the proposal to not initiate the Transitional Kindergarten program, for the associated revenue limit savings of $224 million. The Legislature could consider prioritizing state preschool slots for low–income children specifically affected by the change in kindergarten start date. Moreover, in the context of this change—and the significant reductions proposed for the state's child care programs—the Legislature may want to modify or reject the Governor's proposed $58 million cut to the state preschool program.

Concerns With Governor's Overarching Proposition 98 Approach

The Governor's Proposition 98 proposal builds one budget plan that is based upon revenues that would not materialize until midyear and then has a relatively severe back–up plan in case the revenues ultimately do not materialize. Such an approach generates significant uncertainty for school districts, as discussed below.

Governor Proposes Relatively Severe Back–Up Plan for Schools. Given his back–up plan would cut schools and community colleges by $4.8 billion (including $2.4 billion in programmatic reductions), schools and community colleges would bear most of the midyear trigger reductions. Schools have difficulty, however, in downsizing operations midyear given students already have been assigned to classes, teachers are working on year–long contracts, and the number of instructional days already has been decided.

Most Districts Likely to Build 2012–13 Budgets Based Upon Governor's Back–Up Plan. Because the Governor's basic plan relies on revenues that have not yet materialized and ultimately might not materialize, and because large midyear reductions are so disruptive, most districts likely would feel compelled to adopt budgets assuming the Governor's back–up plan. Under this scenario, districts would adopt 2012–13 budgets that already contain $2.4 billion in programmatic reductions statewide. That is, they already would make the reductions some would be hoping to avoid. If revenues ultimately did materialize, these districts likely would restore reserve levels immediately but not make major programmatic adjustments until the following school year (2013–14). While districts could make relatively minor programmatic adjustments midyear (such as hiring additional instructional aides), more significant programmatic changes (such as reducing class size and hiring additional teachers) likely would not be undertaken. This is because even these enhancements can be disruptive if implemented midyear, resulting in the shuffling of students among classes and corresponding changes in students' teachers.

Districts That Budget More Optimistically Could Face Very Difficult Midyear Situations. By contrast, districts that feel compelled to be more optimistic and build their budgets assuming the tax measure is adopted could face very difficult midyear fiscal situations. Under this scenario, districts would have few options for making $2.4 billion in programmatic reductions midyear. Given current statutory restrictions, districts cannot lay off teachers midyear. They also typically negotiate changes in the length of the work year with affected unions, with districts needing to follow certain typically lengthy legal procedures if they wish to declare impasse and impose changes to the teacher contract. Moreover, districts with reserve levels at the state–allowed minimums would not have sufficient reserves to cover a reduction as large as the one proposed under the Governor's back–up plan. As a result of all these factors, some of these districts could run out of cash the last part of the school year, be unable to make payroll, and require an emergency state loan (for which the district pays all associated costs and loses local control for a period up to 20 years). Though the administration indicates it is willing to work with districts to ameliorate some of these issues, reaching agreement is likely to be difficult and most of the modifications likely to be considered (such as a new layoff window after the election) still would be disruptive.

Consider Unintended Consequences of Trigger Approach. Though the 2012–13 budget situation under the Governor's plan is awkward for school districts, his plan would improve notably the outlook for schools over the subsequent four years. Nonetheless, the Governor's trigger approach has significant consequences for school districts in 2012–13. As detailed above, for 2012–13, most school districts will feel compelled to make the programmatic reductions imposed by the triggers. Given this is the case, the Legislature needs to be very deliberate in structuring a trigger package, as it in essence would determine the size and quality of California's 2012–13 K–14 education program. The Legislature should be especially careful in setting the size of the trigger reduction, determining the specific K–14 reductions to impose, and designing tools to help districts respond given all the constraints they face in making midyear adjustments. Alternatively, given the potentially unintended consequences of the trigger as well as the major disruptions caused by midyear reductions, the Legislature could consider building a budget without midyear cuts. In this case, the Legislature could focus on a funding level it could afford despite the revenue uncertainties and then use any ballot–measure revenue as one–time investments in 2012–13 to pay down existing Proposition 98 obligations.

CalWORKs and Subsidized Child Care

The Governor's budget proposes to reduce General Fund support for CalWORKs and subsidized child care—the state's primary sources of cash assistance and work support for California's low–income families—by a total of about $1.4 billion. These savings would be achieved primarily by: (1) reducing cash grants received by a significant portion of current CalWORKs recipients, (2) further limiting eligibility for subsidized child care and CalWORKs employment services, and (3) reducing the maximum amount the state pays child care providers. To manage these significant reductions, the Governor proposes to prioritize funding in these programs on efforts to increase work participation and support for families that are most likely to achieve self–sufficiency through employment.

Major Proposals

Restructuring the CalWORKs Program. Currently, the CalWORKs program provides 48 months of cash assistance, employment services, and child care to support efforts of low–income families to achieve self–sufficiency through a variety of welfare–to–work activities (such as employment, education, training, and other activities to remove barriers to work). In addition, the current program provides non–time–limited cash assistance—on behalf of children—to families not participating in welfare–to–work activities. In 2011–12, a combined total of $5.4 billion in federal, state, and local funds support these activities.

Under the Governor's proposal, the current CalWORKs program would be replaced by a three–part system, consisting of two CalWORKs subprograms—CalWORKs Basic and CalWORKs Plus—and a new Child Maintenance program. The CalWORKs Basic program would effectively continue the current CalWORKs program, including current cash assistance levels and employment services, for eligible adults for up to 24 months. After 24 months in CalWORKs Basic, families working a sufficient amount of hours (30 hours for single–parent families, 35 hours for two–parent families, and 20 hours for single–parent families with a child under the age of six) in unsubsidized employment would be eligible for an additional 24 months (48 months total) of cash assistance, employment services, and child care through the CalWORKs Plus program. Families who fail to meet these work participation requirements—for various reasons—would be transferred to the Child Maintenance program. In addition, all families with parents who are not work–eligible (such as those with undocumented immigrant parents) would be placed in the new Child Maintenance program rather than the CalWORKs program. Families in the Child Maintenance program would receive reduced cash assistance (27 percent below current CalWORKs levels) and no employment services or child care. Participation in the Child Maintenance program would not be time limited. Time limits in both the CalWORKs Basic (24 months) and the CalWORKs Plus (an additional 24 months) would be applied retroactively to all CalWORKs recipients, including those exempted from work participation requirements or in sanction status.

Although these three programs would continue to serve the same population as the current CalWORKs program, a majority of current recipients would face a reduced cash grant and all recipients would face more restrictive limitation on receipt of employment services and child care. Altogether, the Governor's proposed restructuring would reduce General Fund expenditures for CalWORKs by an estimated $942 million. The Governor's budget also proposes to transfer $736 million in federal Temporary Assistance for Needy Families (TANF) block grant funds (the primary source of federal funding for the CalWORKs program), made available by the CalWORKs restructure, to the Student Aid Commission to fund Cal Grants. This transfer is necessary to fully realize the General Fund savings from the reduced CalWORKs expenditures described above, while continuing to satisfy requirements for state maintenance–of–effort in programs which fulfill the goals of the TANF program.

Tightening Work Participation Requirements. The Governor's proposal would narrow the scope of work activities which allow a family to meet its CalWORKs work participation requirement. The first way the proposal would do this is by limiting countable activities to a more restrictive list of federal requirements. More specifically, the Governor's proposal would eliminate the opportunity for CalWORKs recipients to pursue higher education beyond 12 months of vocational training or receive mental health or substance abuse treatment as part of welfare–to–work activities. Additionally, the proposal would allow recipients to participate only in unsubsidized employment (as opposed to subsidized employment or education) after 24 months of cash assistance. This narrowed employment eligibility definition would also apply to all subsidized child care programs, limiting eligibility for subsidized child care to those families who meet the work requirements described above for the CalWORKs Plus program.