Submitted July 18, 2012

Proposition 31

State Budget. State and Local Government.

Initiative Constitutional Amendment and Statute.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact

-

Fiscal Impact: Decreased state sales tax revenues of $200 million annually, with corresponding increases of funding to local governments. Other, potentially more significant changes in state and local budgets, depending on future decisions by public officials.

Yes/No Statement

A YES vote on this measure means: Certain fiscal responsibilities of the Legislature and Governor, including state and local budgeting and oversight procedures, would change. Local governments that create plans to coordinate services would receive funding from the state and could develop their own procedures for administering state programs.

A NO vote on this measure means: The fiscal responsibilities of the Legislature and Governor, including state and local budgeting and oversight procedures, would not change. Local governments would not be given (1) funding to implement new plans that coordinate services or (2) authority to develop their own procedures for administering state programs.

|

Overview

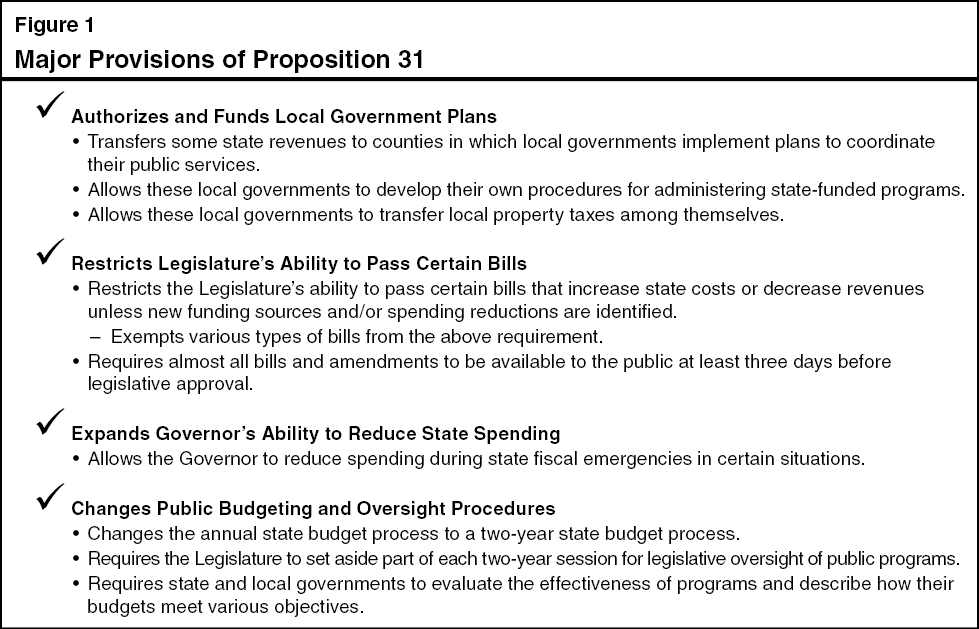

This measure changes certain responsibilities of local governments, the Legislature, and the Governor. It also changes some aspects of state and local government operations. Figure 1 summarizes the measure’s main provisions, each of which are discussed in more detail below.

Authorizes and Funds Local Government Plans

Proposal

Allows Local Governments to Develop New Plans. Under this measure, counties and other local governments (such as cities, school districts, community college districts, and special districts) could create plans for coordinating how they provide services to the public. The plans could address how local governments deliver services in many areas, including economic development, education, social services, public safety, and public health. Each plan would have to be approved by the governing boards of the (1) county, (2) school districts serving a majority of the county’s students, and (3) other local governments representing a majority of the county’s population. Local agencies would receive some funding from the state to implement the plans (as described below).

Allows Local Governments to Alter Administration of State-Funded Programs. If local governments find that a state law or regulation restricts their ability to carry out their plan, they could develop local procedures that are “functionally equivalent” to the objectives of the existing state law or regulation. Local governments could follow these local procedures—instead of state laws or regulations—in administering state programs financed with state funds. The Legislature (in the case of state laws) or the relevant state department (in the case of state regulations) would have an opportunity to reject these alternate local procedures. The locally developed procedures would expire after four years unless renewed through the same process.

Allows Transfer of Local Property Taxes. California taxpayers pay about $50 billion in property taxes to local governments annually. State law governs how property taxes are divided among local government entities in each county. This measure allows local governments participating in plans to transfer property taxes allocated to them among themselves in any way that they choose. Each local government affected would have to approve the change with a two-thirds vote of its governing board.

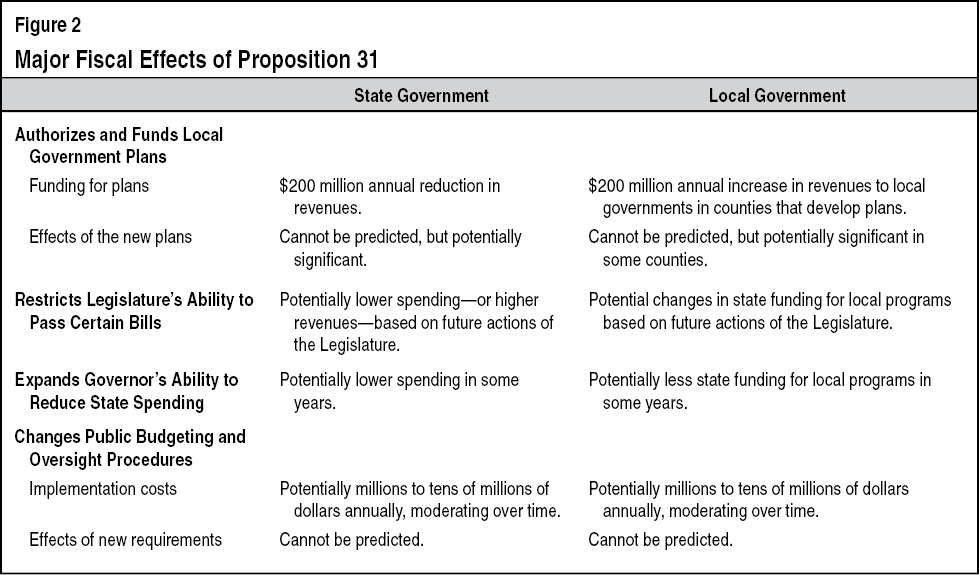

Shifts Some State Sales Tax Revenues to Local Governments. Currently, the average sales tax rate in the state is just over 8 percent. This raised $42.2 billion in 2009-10, with the revenues allocated roughly equally to the state and local governments. Beginning in the 2013-14 fiscal year, the measure would shift a small part of the state’s portion to counties that implement the new plans. This would not change sales taxes paid by taxpayers. The shift would increase revenues of the participating local governments in counties with plans by a total of about $200 million annually in the near term. The state government would lose a corresponding amount, which would no longer be available to fund state programs. The sales taxes would be allocated to participating counties based on their population. The measure requires a local plan to provide for the distribution of these and any other funds intended to support implementation of the local plan.

Fiscal Effects

In addition to the shift of the $200 million described above, there would be other fiscal effects on state and local governments. For example, allowing local governments to develop their own procedures for administering state-funded programs could lead to potentially different program outcomes and state or local costs than would have occurred otherwise. Allowing local governments to transfer property taxes could affect how much money goes to a given local government, but would not change the total amount paid by property taxpayers. Local governments also likely would spend small additional amounts to create and administer their new plans. The changes that would result from this part of the measure depend on (1) how many counties create plans, (2) how many local governments alter the way they administer state-funded programs, and (3) the results of their activities. For those reasons, the net fiscal effect of this measure for the state and local governments cannot be predicted. In some counties, these effects could be significant.

Restricts Legislature’s Ability to Pass Certain Bills

Current Law

Budget and Other Bills. Each year, the Legislature and the Governor approve the state budget bill and other bills. The budget bill allows for spending from the General Fund and many other state accounts. (The General Fund is the state’s main operating account that provides funding to education, health, social services, prisons, and other programs.) In general, a majority vote of both houses of the Legislature (the Senate and the Assembly) is required for the approval of the budget bill and most other bills. A two-thirds vote in both houses, however, is required to increase state taxes.

As part of their usual process for considering new laws, the Legislature and Governor review estimates of each proposed law’s effects on state spending and revenues. While the State Constitution does not mandate that the state identify how each new law would be financed, it requires that the state’s overall budget be balanced. Specifically, every year when the state adopts its budget, the state must show that estimated General Fund revenues will meet or exceed approved General Fund spending.

Proposal

Restricts Legislature’s Ability to Increase State Costs. This measure requires the Legislature to show how some bills that increase state spending by more than $25 million in any fiscal year would be paid for with spending reductions, revenue increases, or a combination of both. The requirement applies to bills that create new state departments or programs, expand current state departments or programs, or create state-mandated local programs. Exemptions from these requirements include bills that allow one-time spending for a state department or program, increase funding for a department or program due to increases in workload or the cost of living, provide funding required by federal law, or increase the pay or other compensation of state employees pursuant to a collective bargaining agreement. The measure also exempts bills that restore funding to state programs reduced to help balance the state budget in any year after 2008-09.

Restricts Legislature’s Ability to Decrease State Revenues. This measure also requires the Legislature to show how bills that decrease state taxes or other revenues by more than $25 million in any fiscal year would be paid for with spending reductions, revenue increases, or a combination of both.

Changes When Legislature Can Pass Bills. This measure makes other changes that could affect when the Legislature could pass bills. For example, the measure requires the Legislature to make bills and amendments to those bills available to the public for at least three days before voting to pass them (except certain bills responding to a natural disaster or terrorist attack).

Fiscal Effects

This measure would make it more difficult for the Legislature to pass some bills that increase state spending or decrease revenues. Restricting the Legislature’s ability in this way could result in state funds spent on public services being less—or taxes and fees being more—than otherwise would be the case. Because the fiscal effect of this part of the measure depends on future decisions by the Legislature, the effect cannot be predicted, but it could be significant over time. Because the state provides significant funding to local governments, they also could be affected over time.

Expands Governor’s Ability to Reduce State Spending

Current Law

Under Proposition 58 (2004), after the budget bill is approved, the Governor may declare a state fiscal emergency if he or she determines the state is facing large revenue shortfalls or spending overruns. When a fiscal emergency is declared, the Governor must call the Legislature into special session and propose actions to address the fiscal emergency. The Legislature has

45 days to consider its response. The Governor’s powers to cut state spending, however, currently are very limited even if the Legislature does not act during that 45-day period.

Proposal

Allows Governor to Reduce Spending in Certain Situations. Under this measure, if the Legislature does not pass legislation to address a fiscal emergency within 45 days, the Governor could reduce some General Fund spending. The Governor could not reduce spending that is required by the Constitution or federal law—such as most school spending, debt service, pension contributions, and some spending for health and social services programs. (These categories currently account for a majority of General Fund spending.) The total amount of the reductions could not exceed the amount necessary to balance the budget. The Legislature could override all or part of the reductions by a two-thirds vote in both of its houses.

Fiscal Effects

Expanding the Governor’s ability to reduce spending could result in overall state spending being lower than it would have been otherwise. The fiscal effect of this change cannot be predicted, but could be significant in some years. Local government budgets also could be affected by lower state spending.

Changes Public Budgeting and Oversight Procedures

Proposal

Changes Annual State Budget Process to a Two-Year Process. This measure changes the state budget process from a one-year (annual) process to a two-year (biennial) process. Every two years beginning in 2015, the Governor would submit a budget proposal for the following two fiscal years. For example, in January 2015 the Governor would propose a budget for the fiscal year beginning in July 2015 and the fiscal year beginning in July 2016. Every two years beginning in 2016, the Governor could submit a proposed budget update. The measure does not change the Legislature’s current constitutional deadline of June 15 for passing a budget bill.

Sets Aside Specific Time Period for Legislative Oversight of Public Programs. Currently, the Legislature oversees and reviews the activities of state and local programs at various times throughout its two-year session. This measure requires the Legislature to reserve a part of its two-year session—beginning in July of the second year of the session—for oversight and review of public programs. Specifically, the measure requires the Legislature to create a process and use it to review every state-funded program—whether managed by the state or local governments—at least once every five years. While conducting this oversight, the Legislature could not pass bills except for those that (1) take effect immediately (which generally require a two-thirds vote of both houses) or (2) override a Governor’s veto (which also require a two-thirds vote of both houses).

Imposes New State and Local Budgeting Requirements. Currently, state and local governments have broad flexibility in determining how to evaluate operations of their public programs. This measure imposes some general requirements for state and local governments to include new items in their budgets. Specifically, governments would have to evaluate the effectiveness of their programs and describe how their budgets meet various objectives. State and local governments would have to report on their progress in meeting those objectives.

Fiscal Effects

State and local governments would experience increased costs to set up systems to implement the new budgeting requirements and to administer the new evaluation requirements. These costs would vary based on how state and local officials implemented the requirements. Statewide, the costs would likely range from millions to tens of millions of dollars annually, moderating over time. These new budgeting and evaluation requirements could affect decision making in a variety of ways—such as, reprioritization of spending, program efficiencies, and additional investments in some program areas. The fiscal impact on governments cannot be predicted.

Summary of Measure’s Fiscal Effects

As summarized in Figure 2, the measure would shift some state sales tax revenues to counties that implement local plans. This shift would result in a decrease in state revenues of $200 million annually, with a corresponding increase of funding to local governments in those counties. The net effects of this measure’s other state and local fiscal changes generally would depend on future decisions by public officials and, therefore, are difficult to predict. Over the long term, these other changes in state and local spending or revenues could be more significant than the $200 million shift of sales tax revenues discussed above.

Return to Propositions

Return to Legislative Analyst's Office Home Page