2009-10 Budget Analysis Series: General Government

General Fund Retirement Costs Budgeted to Grow by 10 Percent in 2009–10

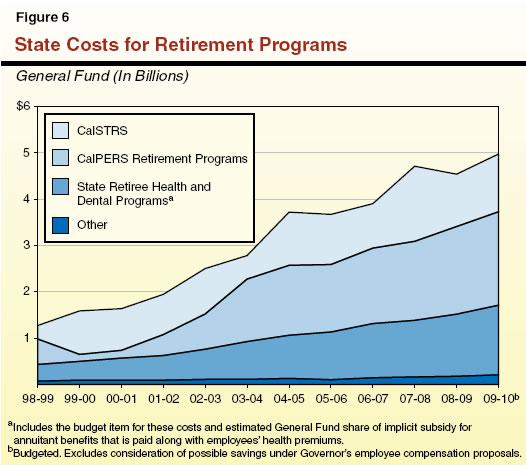

Retiree Health Is the Fastest–Growing Retirement Cost Category in the Budget. Figure 6 shows the budgeted General Fund contributions to various employee retirement programs—including California State Teachers’ Retirement System (CalSTRS) pension benefits, CalPERS pension programs for state employees and judges, state retiree health and dental benefits, and other programs. As shown in Figure 6, General Fund payments to these programs are expected to total $5 billion in 2009–10—up 10 percent from 2008–09. (In addition to General Fund payments, special funds, and other state funds are expected to pay about $1.3 billion for CalPERS pension benefits in 2009–10.) The fastest–growing cost category (in terms of dollars) is that related to retiree health and dental benefits, which are administered through CalPERS and DPA, respectively. The General Fund line item for retiree health and dental costs is budgeted to grow by $139 million—up 12 percent from 2008–09—due to growth in premiums and enrollment. The “other” programs include a proposed appropriation of $20 million to UC’s pension program, which comes after a nearly two–decade period when neither the state nor UC nor employees contributed to the plan. (We discuss the UC pension proposal in the 2009–10 Budget Analysis Series: Higher Education.) Payments to CalSTRS are budgeted to increase by $115 million—up 10 percent. About one–half of this increase results from a $57 million interest payment (the first of four annual payments) under a 2007 court order that required the state to make previously withheld contributions to the system.

Few Options for Savings in the Short Run…but Savings Options Exist in the Long Run. While the Legislature is contemplating cuts in many major program areas to address the state’s budget deficit, Figure 6 shows that budgeted General Fund retirement costs increase by 10 percent in 2009–10. Unlike most other areas of the budget, the Legislature has very little control over these costs in the short run. Case law establishes that the bulk of these payments—principally those for CalPERS and CalSTRS pension programs—are enforceable contractually by retirement systems and their members. While the legal status of the state’s contributions for retiree health and dental benefits has never been litigated, efforts to alter those benefits in order to reduce contributions substantially would likely result in litigation against the state. While these increased costs are difficult or impossible to avoid in the short run, the Legislature has several options to reduce future state costs in the long run, including:

- Altering future pension or retiree health benefits for state employees, teachers, and university employees (particularly for new hires).

- Spending more in the near term to address unfunded retiree health liabilities of the state and UC, which would help limit annual cost increases over the long term.

Grim Outlook for State’s Pension Contributions in 2010–11 and Beyond

Pension Systems Worldwide Experienced Huge Losses in 2008. The large drop in the stock market during 2008—as well as broad–based difficulties in real estate and other segments of the investment markets—has strained pension systems worldwide, including CalPERS and CalSTRS. As of January 2009, the value of CalPERS’ entire investment portfolio was under $180 billion, or about 25 percent below its value at the beginning of 2008–09. As of November 2008, the value of CalSTRS’ investment portfolio also was down over 20 percent. While actuaries of both systems reported that their respective accrued liabilities were just under 90 percent funded as of their last valuations the pension systems’ investment declines in 2008–09 probably will be so large that substantial state contribution increases cannot be avoided beginning in 2010–11. This is despite the fact that pension plans employ various techniques to avoid adjusting employer contribution rates upward or downward based on temporary fluctuations in the stock market. These contribution increases will be needed to begin addressing new unfunded liabilities that will emerge because of this year’s investment losses.

Increased Costs in the Hundreds of Millions of Dollars Appear Likely for 2010–11. Actuaries at CalPERS have disclosed that, under existing system policies for setting state contribution rates, if the system’s portfolio experiences a 20 percent loss in investment value during 2008–09, employer contribution rates may increase by about 2 percent to 5 percent of payroll. For the state, these increases would take effect beginning in 2010–11. While the precise state contribution increases will not be known until May 2010, we can make a rough estimate that a 20 percent or greater investment decline for CalPERS in 2008–09 could increase General Fund costs by hundreds of millions of dollars, with proportional increases for special funds. Under case law, the CalPERS Board of Administration has the exclusive power—relying on advice from its actuaries—to determine the state’s pension contribution rates. By contrast, state contribution rates to CalSTRS are set by the Legislature in statute. This usually limits the year–over–year increase in regular state contributions to CalSTRS but the 2008–09 investment losses may be so large that state contributions to CalSTRS could rise sharply as well. This is because the Education Code (Sections 22955[b] and [c]) provide that the state is required to provide additional funding to CalSTRS if the actuarial value of its assets associated with benefit provisions in effect as of 1990 is less than the actuarial liability for those benefits. In recent years, the state has not had to contribute any funds for this purpose. A substantial drop in CalSTRS’ asset value in 2008–09, however, could trigger this requirement beginning in 2010–11. While it is difficult to predict the cost impact for the General Fund, due to this provision, it could be in the hundreds of millions of dollars annually.

Return to General Government Table of Contents, 2009-10 Budget Analysis SeriesReturn to Full Table of Contents, 2009-10 Budget Analysis Series