Recently, the Legislature enacted a package of changes known as the “fuel tax swap” to achieve General Fund relief. However, the passage of ballot measures in November 2010 potentially undoes portions of the tax swap package. In response to these ballot measures, the Governor’s January 2011–12 budget proposes statutory changes to recapture the use of transportation funds to help balance the state’s budget. In this brief we describe and evaluate these recent changes and the Governor’s proposal. We also provide additional options that the Legislature may wish to consider that offer more solutions to achieve General Fund relief.

State Funds Various State and Local Programs. The state funds a variety of state and local transportation programs. Figure 1 summarizes these major transportation programs and indicates whether the state or local agencies are the program’s primary beneficiary.

Figure 1

The State Funds Various Transportation Programs

|

Program

|

Description

|

State Funding Source

|

Responsibility and Primary Beneficiary

|

|

State Highway Maintenance

|

Routine and minor maintenance of the state’s highway system.

|

Fuel excise tax revenues and vehicle weight fees in the SHA.

|

State

|

|

SHOPP—Highway Replacement

|

Major repairs and replacement of the state’s highway system.

|

Fuel excise tax revenues and vehicle weight fees in the SHA.

|

State

|

|

STIP—Regional (75 percent)

|

Formula funding provided to counties for transportation projects that relieve congestion, expand and improve the state’s transportation system (mainly state highways).

|

Fuel excise tax revenues in the SHA.

|

State and local

|

|

STIP—Interregional (25 percent)

|

Funding to Caltrans for highway and rail projects to build out the planned transportation system and connect the state’s regions.

|

Mainly fuel excise tax revenues in the SHA.

|

State and local

|

|

Local Streets and Roads

|

Formula funding provided to cities and counties for local streets and roads.

|

Fuel excise tax revenues in the HUTA.

|

Local

|

|

STA—Local Transit

|

Formula funding provided to subsidize local transit operations.

|

Diesel sales tax revenues in PTA.

|

Local

|

|

State Intercity Rail

|

Existing subsidized rail service that operates within and between various regions of the state.

|

Diesel sales tax revenues in PTA.

|

State and local

|

|

Transportation Development Act

|

Funding provided to counties generally for local transit programs.

|

One–quarter cent statewide sales tax deposited into Local Transportation Funds.

|

Local

|

Generally, state programs are managed by the California Department of Transportation (Caltrans), and are intended to benefit the state as a whole. For example, the highway system maintained by the state provides for the safe and efficient movement of people and goods throughout the state. Local programs are generally implemented by local agencies, such as cities and counties, and primarily benefit the specific communities in which they operate. One example is the State Transit Assistance (STA) program, which subsidizes local bus and rail operations.

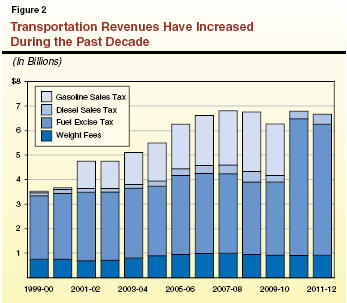

Funding for These Programs Has Grown Over the Last Decade. Historically, ongoing sources of state transportation funding generally came from dedicated transportation revenues including: (1) excise taxes on gasoline and diesel fuel, (2) vehicle weight fees, (3) a one–quarter cent statewide sales tax, and (4) a portion of the sales tax on diesel fuel. In response to growing demands for funding, the Legislature and voters increased funding for transportation programs over the last ten years. For example, a significant increase in funding was provided through the commitment of revenues from the sales tax on gasoline to certain transportation programs instead of to the General Fund, as was previously the case. The level of funding available from ongoing transportation revenues during this period is shown in Figure 2. In recent years, the state has received around $6.5 billion from these revenues.

The effort to increase funding beyond the amount generated by historical funding sources is also reflected in the state’s commitment of additional bond funding to transportation purposes. The Legislature approved, and the voters ratified, two large general obligation bond measures in 2006 and 2008 dedicating nearly $30 billion for transportation projects. General obligation bonds are typically repaid from the state’s General Fund.

State Has a History of Sharing Transportation Funds

with Local Agencies. For decades the state has shared funds and some aspects of decision making for transportation projects with local agencies. Specifically, the state has given a considerable amount of funding to local agencies— including one–third of the excise tax revenues, all funds generated from the one–quarter cent statewide sales tax, and the bulk of the revenues from the sales taxes on gasoline and diesel.

Early last year, the Legislature and Governor enacted a package of major statutory and budgetary changes to transportation funding. These changes increased the Legislature’s flexibility over the use of transportation funds, resulting in ongoing General Fund relief by paying the debt service on highway and road bonds from fuel excise tax revenues. This package of changes, known as the fuel tax swap, is described in more detail below.

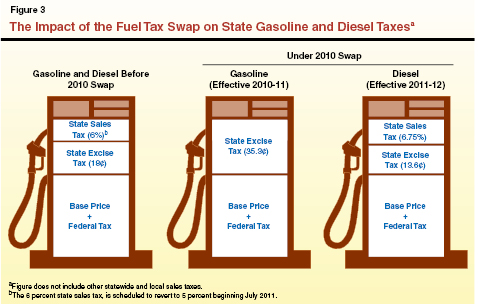

Swap Made Significant Changes to the Way the State Taxes Fuels. In March 2010, the Legislature enacted the fuel tax swap to provide the state with greater flexibility over the long run in how it uses taxes on fuels for the state’s spending priorities. Changes made to the state’s fuel tax rates are shown in Figure 3 (see next page). Prior to this legislation, the state charged an 18 cents per gallon excise tax on gasoline and diesel fuel. The state also charged a 6 percent sales tax on the purchase of these fuels. Under the tax swap the state no longer charges a sales tax on gasoline, and instead imposes an additional excise tax (17.3 cents per gallon in 2010–11) on gasoline to generate an amount equivalent to what would have been collected from the sales tax. The rate of the new excise tax imposed by the swap legislation is to be adjusted annually to ensure that the amount of revenues collected equals the loss of the sales tax on gasoline.

Fuel Tax Swap Provided Flexibility and Permanent Help to the General Fund. The bulk of gasoline sales tax revenues are required by past ballot measures to be given to local transportation agencies for local roads and transit systems. Paying debt service on state transportation bonds from gasoline sales taxes, including bonds that benefit local transportation programs, is not allowed. However, the State Constitution did allow the use of fuel excise tax revenues to pay transportation debt service costs. Mindful of these limitations, the Legislature adopted the 2010 fuel swap package to decrease the revenues collected from the sales tax and increase the revenues collected from the more flexible excise tax.

This, in turn, meant that additional transportation monies were available to pay debt service on highway and road bonds. The 2010–11 Budget Act assumed that $778 million (including $491 million from fuel excise tax revenues) would be used in this way to achieve commensurate General Fund savings and help balance the state budget. The tax swap legislation, along with the 2010–11 Budget Act, also provided one–time loans from fuel excise tax revenues to the General Fund of $762 million in 2010–11. In total, this combination of actions was expected to provide roughly $1.6 billion in help to the General Fund in 2010–11, and $727 million more in 2011–12, as well as ongoing solutions of about $1 billion per year in the future.

Tax Swap Maintained Funding Levels for Local Roads and Highway Projects…In addition to providing General Fund relief, the new excise tax revenues from the swap also provided funding to “backfill” gasoline sales tax revenues that would have been provided under the old funding system to local agencies for their streets and roads programs. Funding for the State Transportation Improvement Program, which previously came from the sales tax, was also maintained at approximately the same levels that had previously been provided.

…But Impacted Funding for Transit Programs. The Public Transportation Account (PTA)—the state’s mass transportation special fund—received a large share of the gasoline sales tax revenues prior to the swap. A portion of the funds in the PTA were provided to the STA program, which subsidizes local bus and rail operations, and to the state’s intercity rail program. Changes were also made to the way the state taxes diesel fuel, beginning in 2011–12. Specifically, the swap increases the sales tax on diesel fuel by 1.75 percent, and reduces the excise tax by a corresponding amount. Because the sales tax on diesel is deposited into the PTA, this change provides a partial backfill of gasoline sales tax funding that would have flowed to the PTA. In addition, the Legislature increased the share of PTA funding for STA to 75 percent of the revenues going to the account. In total these changes were estimated to provide about $300 million per year in STA subsidies, a level significantly higher than had been historically provided.

In November 2010, voters passed two initiative measures that potentially undo portions of the tax swap package. These measures, Proposition 22 and Proposition 26, and their impacts are discussed below.

Proposition 22. Proposition 22 is a complex ballot measure that restricts the state’s use of certain state and local funds. Among other provisions, the proposition significantly restricts the state from using fuel excise tax revenues for General Fund relief, which was previously allowed. While the full impacts of the measure remain unknown, it is widely agreed by transportation and legal experts that the measure:

- Restricts the state’s ability to pay for transportation debt service using fuel excise tax revenues.

- Prohibits borrowing of fuel excise tax revenues as well as certain other transportation funds.

- Requires gasoline sales tax revenues (if such a tax were ever to be reinstated in the future) to be used for transportation purposes, regardless of the state’s fiscal condition.

Because of these restrictions, the state is no longer able to use fuel excise tax revenues to help the General Fund by offsetting debt service costs and providing loans to the General Fund.

Proposition 26. Proposition 26 effectively makes any state tax increase enacted by the Legislature through a majority vote of the two houses between January 1, 2010 and November 2, 2010 (the date Proposition 26 was approved by voters) subject to reenactment with a two–thirds vote of both houses of the Legislature. If such statutory changes are not reenacted by November 3, 2011, Proposition 26 would likely repeal the tax provisions of that statute.

The tax changes enacted by the Legislature in the fuel tax swap are subject to this provision of Proposition 26. This means that if the Legislature does not reenact the tax provisions of the tax swap with a two–thirds vote, they would be repealed November 3, 2011. Absent legislative action to reenact the tax swap, the state would most likely return to taxing fuels the way it did prior to the swap legislation. This would mean the state would reduce the excise tax on gasoline to 18 cents per gallon, and resume charging a sales tax on that fuel.

Such a reversal in the state’s approach for taxation of fuels would have important implications for the way this transportation funding stream could be used. Because of the restrictions on the use of gasoline sales tax revenues established by various propositions, the majority of these revenues (which total about $2.5 billion) would have to be given to local transportation agencies for bus and rail subsidies and capital projects selected by local road agencies. For example, the PTA would receive about $1.5 billion each year for at least the near term. This would be significantly higher than the level of funding historically provided for transit and mass transportation programs.

Alternatively, it is possible (but less likely) that, absent legislative action to reenact the swap, Proposition 26 could be interpreted as eliminating the new excise tax enacted by the tax swap, but not reinstating the sales tax on gasoline. In this case, the state would collect about $2.5 billion less in fuel tax revenues for transportation programs than it currently does.

General Fund Impact. Absent legislative action to address the passage of these two measures, a large portion of the $1.6 billion in General Fund relief assumed in the 2010–11 Budget Act will probably be undone. Similarly, General Fund relief anticipated in 2011–12 and future years would also not occur.

The Governor’s January 2011–12 budget proposes to use transportation funds to help the General Fund by providing loans and offsetting debt service costs. We discuss the Governor’s proposal in more detail below.

Proposal Would Reenact the Provisions of the Tax Swap. The Governor’s budget proposes statutory changes to ensure that the General Fund receives about the same level of benefit from transportation as was planned for the current and budget years from the tax swap and the 2010–11 Budget Act. Specifically, the Governor proposes to reenact the fuel tax swap provisions with a two–thirds vote to prevent the swap from being repealed under Proposition 26 in November 2011. His proposal also maintains about the same level of funding for transit programs, including providing $330 million to STA in 2011–12 by directing new diesel sales tax revenues from the tax swap to this program.

However, reenactment of the tax swap alone will not recapture the benefits to the General Fund. This is because, as noted above, Proposition 22 prevents the state from using fuel excise tax revenues for General Fund relief. Thus, as described below, the Governor proposes additional statutory changes that would transfer the fuel excise tax revenues generated by the tax swap to the State Highway Account (SHA) and instead use other SHA funds to pay transportation debt service and make loans to the General Fund.

Governor Proposes Using Weight Fees for General Fund Relief. The Governor’s budget plan proposes using vehicle weight fees in the SHA, rather than fuel excise tax revenues, to provide General Fund relief. While the use of excise taxes to offset debt service costs or provide loans is restricted under Proposition 22, the use of vehicle weight fees for these same purposes is not explicitly prohibited. In the absence of this proposal, the weight fee revenue would otherwise be used to fund highway repair projects and the administration of Caltrans. Therefore, the Governor proposes to keep these programs whole by “backfilling” the SHA with the fuel excise tax revenues that had been planned for General Fund relief under the tax swap.

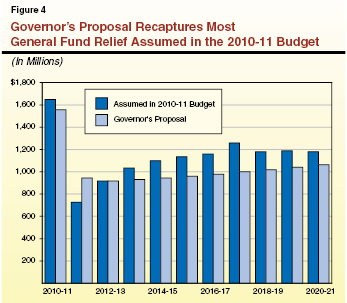

General Fund Benefit Achieved by Paying Debt Service and Borrowing. The Governor’s package would provide substantial help to the General Fund. Specifically, it would allow $262 million in vehicle weight fees to be used to pay transportation–related debt in the current year, and permit roughly $800 million in SHA monies (primarily from vehicle weight fees) to pay transportation debt service in 2011–12. The budget also proposes loaning some transportation funds to the General Fund. Altogether, these actions are expected to achieve roughly $1.6 billion in General Fund relief in the current year and $943 million in 2011–12 under this proposal. As shown in Figure 4, the Governor’s proposals would allow the state to realize comparable savings in 2010–11 and 2011–12 relative to what had been assumed under the original fuel tax swap and the 2010–11 budget.

Long–Term General Fund Benefit Less Than Under 2010 Swap. While the Governor’s proposal achieves similar near–term savings, the longer–term benefit to the General Fund would be less than would have been the case under the original fuel tax swap. This is because highway and road debt service costs are expected to increase above the amount of weight fee revenue that would be available to the state to pay these costs.

Adopt Governor’s Proposal. We think the Governor’s proposal to address the state’s short–term transportation budget issues is reasonable. Specifically, by reenacting the fuel tax swap along with the use of weight fee revenues, the Legislature could recapture much of the General Fund benefit that would otherwise be lost due to Propositions 22 and 26. In addition, even with new restrictions on the use of fuel excise taxes under Proposition 22, the Legislature would still have more discretion over the use of these revenues than it does on the use of gasoline sales tax revenues.

Take Advantage of All Weight Fees. In addition, our analysis suggests that as much as $194 million ($150 million in 2010–11 and $44 million in 2011–12) in additional benefit to the General Fund could be achieved by maximizing the use of available weight fee revenues. The Legislature could achieve this by adopting budget–related statutory changes to achieve additional General Fund savings from weight fees to the extent possible given the need to maintain a reasonable fund balance in the SHA.

The Legislature will face significant challenges as it tries to balance the 2011–12 budget. To the extent that it rejects or modifies some of the Governor’s proposed budget solutions, it will need to consider significant reductions not proposed as part of the Governor’s budget. Below, we present two alternative options that would achieve additional General Fund relief in the short term and the long term. These options are on top of the $194 million in additional General Fund relief from weight fees noted above.

As part of the 2009–10 budget package, the Legislature suspended the STA program for four years. However, funding for the program was restored in the fuel tax swap. In light of the past suspension of this program, we think the Legislature may wish to again consider options to reduce or eliminate funding for STA. The first option presented below would reduce STA funding, while the second option would eliminate all funding for the program. As such, these options are mutually exclusive and cannot be combined with each other.

Under the fuel tax swap, the state increased the diesel sales tax by 1.75 percent beginning in 2011–12, and decreased the excise tax by a corresponding amount. Our understanding is that the new diesel sales tax revenues from the 1.75 percent rate are not governed by the provisions of Proposition 22. This means that the Legislature has the ability to use these revenues for any General Fund purpose, not just for providing transit subsidies as the Governor has proposed. In 2011–12, this new diesel sales tax is projected to generate $110 million. The Legislature could adopt statutory language to allow the use of these funds for General Fund purposes and achieve up to $110 million in General Fund benefit. This would result in a corresponding reduction in STA funding. Under this option, STA would continue to receive about $150 million to $200 million each year.

Alternatively, the state could achieve a greater level of General Fund relief without changing the overall level of transportation revenues. As with the tax swap, a more flexible revenue source could be substituted for a less flexible funding source. This would involve two steps and would result in the elimination of all funding for the PTA, including the STA program.

Eliminate the Sales Tax on Diesel and STA Program... In order to eliminate STA funding, the Legislature would first need to eliminate the sales tax on diesel fuel. Doing so would halt the flow of about $400 million in funding to the PTA in 2011–12, including over $300 million for the STA program and about $100 million for intercity rail. Ending this state subsidy for transit operators would have some impacts on bus and rail services. However, because STA funding is a relatively small percentage of operators’ total budgets (about 3 percent) we believe that most transit services would continue to operate without an extensive disruption of transit services. In addition to the STA funds, one–quarter cent of the statewide sales tax revenues is directed to transit purposes. This funding source, which generates about $1.5 billion per year, would not be impacted under this option.

. . .And Increase Weight Fees. In order to achieve General Fund relief by eliminating STA, the Legislature would also need to enact a statute with a two–thirds vote to increase funding from another revenue source. The Legislature could increase vehicle weight fees to generate an additional $400 million in revenue and maintain the same level of overall transportation funding. We believe increasing vehicle weight fees makes sense on a policy basis because the heavy trucks that pay weight fees are responsible for the majority of the wear and tear on the state’s roadways. These funds could provide additional General Fund relief in the near term through debt service offsets and loans. Assuming the Legislature wished to maintain current support of the state’s intercity rail program, it would need to backfill about $100 million in these costs. The remaining $300 million would be available annually in the short term to provide additional relief to the General Fund.