LAO Contact

- Luke Koushmaro

- Overarching Comments

- Motor Vehicle Account

- Frank Jimenez

- Hazardous Waste Control Account

- Department of Pesticide Regulation Fund

- Helen Kerstein

- Environmental License Plate Fund

- Harbors and Watercraft Revolving Fund

- State Parks and Recreation Fund

- Sarah Cornett

- Energy Resources Programs Account

Report in PDF

Report in PDFLAO Report

February 27, 2024The 2024‑25 Budget

Insolvency Risks for Environmental and Transportation Special Funds

- Executive Summary

- Introduction

- Overarching Comments

- Overarching Recommendations

- Special Funds at Risk of Insolvency

- Hazardous Waste Control Account

- Motor Vehicle Account

- Environmental License Plate Fund

- Harbors and Watercraft Revolving Fund

- Energy Resources Programs Account

- State Parks and Recreation Fund

- Conclusion

Executive Summary

Multiple Funds at Risk of Insolvency. Current projections suggest that various special funds which support transportation, environmental protection, and natural resources programs likely will become insolvent in the near future (meaning that they will not have sufficient revenues and fund balances to cover expenditures). These include: the Department of Pesticide Regulation (DPR) Fund, the Energy Resources Program Account (ERPA), Environmental License Plate Fund, Harbors and Watercraft Revolving Fund, Hazardous Waste Control Account (HWCA), Motor Vehicle Account, and State Parks and Recreation Fund. The Governor’s budget proposes actions to address two of the fund conditions—the DPR Fund and ERPA—and the administration indicates that it plans to propose solutions for HWCA at the May Revision.

General Causes and Solutions for Fund Condition Problems. Fund deficits occur when expenditures exceed revenues. When left unaddressed, deficits put funds at an increased risk of insolvency. The state generally has four key approaches it can utilize to address deficits and bring revenues and spending back into balance—each of which comes with varying trade‑offs. The first—and, generally, easiest—is to draw down reserves or fund balances to temporarily cover a share of expenditures. The state also can pursue approaches to supplement a fund’s revenues to ensure it has sufficient resources to cover expenditures by providing funding from other sources or increasing revenues. The fourth option is to reduce expenditures. The state can deploy these strategies in isolation or in combination.

Specific Circumstances and Considerations Vary by Fund. While each of the funds we discuss in the report are at risk of insolvency, their individual circumstances vary—including the reasons for their deficits and the urgency of the need for legislative action. In addition, the specific trade‑offs associated with options to address fund conditions differ by fund.

Simultaneous General Fund and Special Fund Deficits Complicate Potential Solutions. Both the administration and our office anticipate that the state faces significant General Fund problems over the next several years—which coincide with the timing of the deficits and potential insolvencies of the identified special funds. These circumstances reduce the ability of these special funds to help address the General Fund condition. Similarly, the General Fund shortfall makes addressing the special fund deficits more challenging by constraining available options such as loans or transfers.

Recommend Legislature Begin Taking Actions, Making Plans to Address Special Fund Deficits. As noted, the Governor’s January budget proposes solutions for the DPR Fund and ERPA and the administration indicates that it plans to address HWCA as part of the May Revision. We recommend that the Legislature take actions this year to implement ongoing solutions for all three of these funds. Specifically, for ERPA we recommend the Legislature adopt the Governor’s proposal, but constrain expenditure growth (and the resulting impacts to the surcharge applied to ratepayers) by continuing to closely monitor both future requests for increases to ERPA spending as well as the need for and cost‑effectiveness of existing expenditures. For the DPR Fund, we recommend adopting the overall framework of the Governor’s proposals but making modifications as needed to ensure the department is well‑positioned to implement the Legislature’s priorities. (We discuss this proposal in a separate report, The 2024‑25 Budget: Sustainable Funding for the Department of Pesticide Regulation.) For HWCA, we note that the May Revision gives the Legislature little time to review the proposal and consider alternatives. As such, we recommend the Legislature begin this spring to weigh various options for addressing the HWCA fund condition. For the remaining funds, we recommend the Legislature begin developing plans to address the problematic fund conditions before they become insolvent. We also offer specific suggestions regarding time lines and considerations for addressing each individual fund.

Introduction

Current projections suggest that various special funds that support transportation, environmental protection, and natural resources programs likely will become insolvent in the near future (meaning that they will not have sufficient revenues and fund balances to cover their planned expenditures). This report provides information on specific funds at risk of insolvency and issues and recommendations for the Legislature to consider.

The report begins with overarching comments about these funds including (1) an overview of the environmental and transportation special funds we have identified as facing current or forthcoming deficits, (2) general causes and options for addressing special fund insolvencies, (3) a discussion about how circumstances and considerations vary by fund, (4) implications of General Fund and special fund deficits happening at the same time, and (5) overarching recommendations for the Legislature to consider.

We then provide a more detailed description of each of the funds listed below, including a discussion about the specific circumstances regarding each fund’s insolvency risks and recommendations for legislative action. (In addition to the funds listed below, we discuss issues related to the Department of Pesticide Regulation Fund in a forthcoming separate report, The 2024‑25 Budget: Sustainable Funding for the Department of Pesticide Regulation.)

- Hazardous Waste Control Account.

- Motor Vehicle Account.

- Environmental License Plate Fund.

- Harbors and Watercraft Revolving Fund.

- Energy Resources Programs Account.

- State Parks and Recreation Fund.

Overarching Comments

Multiple Funds at Risk of Insolvency

Several Transportation and Environmental Funds at Risk of Insolvency. As shown in Figure 1, current estimates project that various special funds that support transportation, environmental protection, and natural resources programs likely will become insolvent in the near future (meaning that they will not have sufficient fund balances to cover their planned expenditures). These include the following funds: the Department of Pesticide Regulation (DPR) Fund, Hazardous Waste Control Account (HWCA), Motor Vehicle Account (MVA), Environmental License Plate Fund (ELPF), Harbors and Watercraft Revolving Fund (HWRF), Energy Resources Programs Account (ERPA), and State Parks and Recreation Fund (SPRF). We note that while the figure includes the major funds we have identified as having significant fund condition challenges, it does not necessarily represent an exhaustive list of all environmental and transportation special funds at risk of insolvency.

Figure 1

Select Environmental and Transportation Special Funds at Risk of Insolvency

(Dollars in Millions)

|

Fund |

Administering Department |

Primary Revenue Sources |

Expected Expenditures in 2024‑25 |

Year Projected to Become Insolvent |

|

Department of Pesticide Regulation Funda |

DPR |

Tax on pesticide sales and pesticide registration and licensing fees |

$157b |

2024‑25 |

|

Hazardous Waste Control Accountc |

DTSC |

Hazardous waste generator fee and hazardous waste facility fees |

124 |

2024‑25 |

|

Motor Vehicle Account |

DMV |

Vehicle registration fees |

4,904 |

2025‑26 |

|

Environmental License Plate Fund |

CNRA |

Fees on personalized and specialty license plates |

76 |

2025‑26 |

|

Harbors and Watercraft Revolving Fund |

Parks |

Vessel registration and renewal fees, as well as transfers from the MVFA |

49d |

2026‑27 |

|

Energy Resources Programs Accounta |

CEC |

Surcharge on retail electricity sales |

96 |

2027‑28 |

|

State Parks and Recreation Fund |

Parks |

Park entrance fees, overnight camping fees, and transfers from the MVFA |

272 |

2028‑29 |

|

aGovernor’s budget includes related proposal. bGovernor’s budget proposal increases revenues above structural deficit to support programmatic expansions. Amount displayed does not include proposed increases related to this proposal. cGovernor’s proposal expected as part of the May Revision. dDoes not include General Fund transfers. |

||||

|

DPR = Department of Pesticide Regulation; DTSC = Department of Toxic Substances Control; DMV = Department of Motor Vehicles; CNRA = California Natural Resources Agency; Parks = Department of Parks and Recreation; MVFA = Motor Vehicle Fuel Account; and CEC = California Energy Commission. |

||||

Governor’s Budget Includes Proposals to Address Two Funds. As part of the January budget proposal, the Governor includes actions to address fund conditions for the DPR Fund and ERPA. We assess the ERPA proposal later in this report, and the DPR Fund proposal in our forthcoming report, The 2024‑25 Budget: Sustainable Funding for the Department of Pesticide Regulation. The administration also indicates that it plans to address the HWCA deficit as part of the May Revision. The administration has not yet put forth proposals—or indicated a time line for plans to do so—for any of the other funds we discuss in this report.

General Causes and Solutions for Fund Condition Problems

Fund Deficits and Pending Insolvency Primarily Due to Expenditure Growth Outpacing Revenues. Fund deficits occur when expenditures exceed revenues. When left unaddressed, deficits put funds at an increased risk of insolvency. In some cases, deficits are temporary in nature and can be addressed by tapping into reserves or by receiving loans or transfers from other sources to keep the fund solvent until the deficit is addressed. However, if a fund’s deficit is structural—meaning that its ongoing expenditures exceed its ongoing revenues—then it eventually will exhaust any limited‑term reliance on reserves, loans, or transfers and become insolvent. A fund also can become insolvent if past actions to balance revenues and expenditures have not fully addressed the gap. For example, a fee that was established in 2021 to address an operating imbalance within HWCA has generated less revenue than expected. As a result, the fund is now at risk of insolvency again.

Four Key Options for Addressing Fund Deficits. The state generally has four primary approaches it can utilize to address deficits and bring revenues and spending back into balance. The first—and, generally, easiest—is to draw down reserves or fund balances to temporarily cover a share of expenditures. The state also can pursue approaches to supplement the fund’s revenues to ensure it has sufficient resources to cover expenditures by providing funding from other sources or increasing revenues. The other option is to reduce expenditures. The state can adopt these strategies in isolation or in combination. Depending on which approach is deployed and in what manner, it might help address the fund deficit on a short‑term or permanent basis. Each of these options, however, comes with varying trade‑offs.

- Use Reserves or Fund Balances. In many cases, funds carry reserves or balances that can be used to cover deficits on a temporary basis. These balances may have accrued from previous one‑time transfers or periods when revenue exceeded expenditures, such as when funds experienced lower‑than‑expected expenditures or short‑term revenue surges. However, this is not a viable long‑term approach to addressing fund imbalances. The fund will continue to be at risk of insolvency in the future if and when these reserves or balances are depleted and not replenished.

- Use Funding From Other Sources. Other fund sources can be used to bolster a problematic fund condition and help address cost pressures. For example, a fund can receive loans or transfers from the General Fund or a different special fund to increase its resources on a one‑time or ongoing basis. Alternatively, expenditures for specific programs can be shifted away from the struggling fund to instead be supported by a different fund source temporarily or permanently. While these approaches can provide immediate relief for addressing the fund’s deficit, they impact the availability of resources for the other fund source that provides the loan or transfer or absorbs the expenditure. For example, a transfer from the General Fund means there are fewer resources available for the Legislature to allocate from the General Fund for other purposes. In addition, obligations to repay loans can create additional cost pressures for the special fund in future years. Moreover, if the underlying cause of the deficit is not addressed, the fund could still be at risk of eventually becoming insolvent when expenditures continue to outpace revenues in future years.

- Increase Revenues. To address the imbalance on an ongoing basis, the state can take action to increase the revenues that support the fund. Typically, doing so requires increasing existing taxes or fees or establishing a new revenue stream. In some circumstances, fee or tax increases must be approved by the Legislature or by voters. In other cases, the Legislature has granted the administration statutory authority to increase charges, sometimes up to a threshold or according to a schedule.

- Reduce or Control Expenditures. Reducing expenditures can alleviate cost pressures and help bring a fund’s expenditures back into alignment with its level of revenues. This strategy can be employed on a short‑term basis as a temporary solution or permanently to address an ongoing imbalance. However, doing so typically requires reducing activities or service levels, which can be difficult to implement and may result in the state failing to achieve some of its intended programmatic outcomes. Constraining expenditure increases to keep them from growing at a faster rate than revenues can be somewhat easier to implement and can help a deficit from worsening, but usually does not address existing operating imbalances.

Specific Circumstances and Considerations Vary by Fund

While each of the funds highlighted in Figure 1 is at risk of insolvency, their individual circumstances—including the reasons for their deficits, urgency for legislative action, and specific trade‑offs associated with options to address their fund conditions—all differ somewhat.

Funds Display Varying Revenue Trends. While all of the funds discussed in this report currently maintain expenditure levels that exceed their ongoing revenues, the associated revenue trends vary by fund. For example, the main revenue sources for some funds generally have kept pace with inflation, such as for MVA (which relies on vehicle registration fees that are adjusted annually for inflation) and the DPR Fund (which relies on a sales tax on pesticides). However, despite these revenue increases, expenditures for these funds still are increasing at a faster rate. In contrast, several charges, such as those providing revenues for ERPA, HWRF, and SPRF, have not been systematically updated for many years, even to adjust for inflation. As a result, the revenues for these funds have remained relatively flat while facing increased cost pressures. Revenues for ELPF are highly dependent on vehicle owners’ choices about purchasing specialty license plates, which can be difficult to predict. Recent actions were taken to restructure and increase the fees that support HWCA but the resulting revenues have come in significantly lower than anticipated. These distinctions will be important considerations as the Legislature considers the most appropriate avenues for addressing each fund condition.

Some Funds Require More Urgent Action Than Others. Some of the projected funds are at risk of becoming insolvent within the next year or two—and as such require more immediate action—while the state may be able to wait a few years before addressing certain other funds. For example, the DPR Fund and HWCA are projected to become insolvent within the budget year and therefore require urgent intervention. In contrast, ELPF and MVA likely will be able to use reserves to support anticipated expenditures through 2024‑25 but could become insolvent the following year. Other funds, such as HWRF, ERPA, and SPRF likely have sufficient reserves to remain solvent for a few more years.

Trade‑Offs of Options to Address Deficits Vary by Fund. Given the diverse characteristics of each fund—and the differing circumstances that contributed to their deficits—the trade‑offs associated with the options for addressing them also vary. For example, raising vehicle registration fees to increase MVA revenues would impact a large share of California households and businesses. On the other hand, the main revenue source for the DPR Fund is a tax on pesticide sales that affects a relatively small subset of businesses in the state. As another example, fees that support HWRF have not been raised since 2005, whereas HWCA fees were increased substantially as recently as 2021. Moreover, while for every fund the option of reducing expenditures would have implications for state department activities and programs, the nature of these impacts would vary notably. For instance, depending on the fund, reduced expenditures could affect amenities at state parks, staffing levels for the California Highway Patrol (CHP), state oversight of hazardous waste, or state‑level activities related to the clean energy transition.

Implications of General Fund and Special Fund Deficits Happening at Same Time

State Faces a Multiyear, Multibillion‑Dollar Budget Problem. Both the administration and our office anticipate that the state faces significant General Fund deficits over the next several years—which coincides with the timing of the deficits and potential insolvencies of the identified special funds. Estimates of the magnitude of the General Fund deficit in 2024‑25 differ based on how “baseline” spending is defined—the administration estimates a $38 billion deficit whereas, in January, our office estimated that the Governor’s budget addresses a $58 billion deficit—as well as somewhat different revenue projections. More recent fiscal data we summarize in our February publication, The 2024‑25 Budget: Deficit Update, indicate the budget outlook continues to worsen—we now estimate the state has a $73 billion deficit to address with the 2024‑25 budget. Moreover, both our office and the administration estimate that the state will face significant operating deficits in subsequent fiscal years. Specifically, in January, the administration projected that even if the Governor’s proposals were adopted, the state would confront General Fund deficits of $37 billion in 2025‑26, $30 billion in 2026‑27, and $28 billion in 2027‑28.

Special Fund Deficits Complicate Addressing General Fund Condition… Historically, one of the ways the state has helped bolster the General Fund is through making transfers or loans from special funds to the General Fund. For example, MVA transferred around $90 million per year to the General Fund from 2009‑10 through 2018‑19. Additionally, special funds can help ease General Fund pressures by absorbing certain expenditures. For instance, ELPF funded new staff at the Truth and Healing Council and Forest Management Task Force in 2021‑22. These activities likely would have been funded by the General Fund absent the availability of ELPF. When special funds also have deficits, however, they are not available to contribute to these kinds of General Fund budget solutions.

…And General Fund Condition Complicates Addressing Special Fund Deficits. The current General Fund condition also makes addressing the special fund deficits more challenging by constraining available options. On many occasions, the state has used General Fund resources to backfill shortfalls in special funds. For example, over the past few years, when the General Fund had large surpluses, the state has transferred General Fund to help cover deficits in HWCA, HWRF, and SPRF. Additionally, when certain special funds are facing deficits, the state has used the General Fund to cover some costs that the funds might otherwise have paid. For instance, in 2021‑22 and 2022‑23, the state used General Fund rather than MVA to pay for office replacements at the Department of Motor Vehicles (DMV) and CHP. When the state also has an overall budget problem, however, the General Fund is less able to contribute to addressing special fund deficits through transfers or expenditure shifts. Moreover, other special funds with surpluses that the state might otherwise use to support a struggling special fund likely will face calls to instead assist the General Fund condition. For example, in 2023‑24 the budget authorized a loan from the Beverage Container Recycling Fund to HWCA to evade its insolvency. Now that the state budget picture has worsened, however, the Governor proposes relying on the Beverage Container Recycling Fund—along with other special funds—for loans to the General Fund in 2024‑25, reducing its availability to help special funds facing insolvency.

Legislature Could Need to Address Multiple Fund Conditions at Same Time. Not only do concurrent deficits keep special funds and the General Fund from being able to contribute to each other’s potential solutions, they also magnify challenges related to the Legislature’s other available options. For example, if the Legislature wanted to increase revenues to address deficits for the General Fund and special funds, it might have to consider raising multiple fees or taxes simultaneously—which could create burdens for the households and businesses who pay them. Similarly, the Legislature might need to consider reducing services supported by special funds at the same time it is making reductions to other state programs funded by the General Fund, compounding negative impacts for Californians.

Overarching Recommendations

Begin Taking Actions to Address Some Special Fund Problems This Year. The Governor’s January budget includes proposals related to two of the funds we highlight in this report (the DPR Fund and ERPA) and the administration indicates plans to address HWCA as part of the May Revision. As we discuss in more detail in this and our companion DPR report, we recommend the Legislature take actions this year to implement ongoing solutions for all three of these funds. For ERPA we recommend the Legislature adopt the Governor’s proposal, but constrain expenditure growth (and the resulting impacts to the surcharge applied to ratepayers) by continuing to closely monitor both future requests for increases to ERPA spending as well as the need for and cost‑effectiveness of existing expenditures. For the DPR Fund, we recommend adopting the overall framework of the Governor’s proposals but making modifications as needed to ensure the department is well‑positioned to implement the Legislature’s priorities. For HWCA, we note that the May Revision gives the Legislature little time to review the proposal and consider alternatives. As such, we recommend the Legislature begin this spring to weigh various options for addressing the HWCA fund condition.

Begin Developing Plans to Address Looming Insolvency in Remaining Funds. The Governor does not offer proposals or plans to address the other four imbalanced special funds we discuss in this report. The overlapping projected time frames for their insolvencies could result in a need to address multiple special fund problems simultaneously. This scenario both complicates and is complicated by the current and projected General Fund budget condition. Beginning now to develop plans to address the remaining problematic fund conditions before they become insolvent would afford the Legislature more time to develop and review solutions that align with its priorities.

Specifically, for each fund at risk of insolvency, we recommend the Legislature consider what option or combination of options for bringing the fund into balance on an ongoing basis (including using funding from other sources, revenue increases, and reducing expenditures) is appropriate and best aligns with its priorities. In order to help inform these decisions, the Legislature could consider holding hearings to get more information about the nature of the fund deficits, any actions the administration is considering to address these issues, and the potential implications and trade‑offs of options to address the fund conditions. In particular, the Legislature will want to consider potential effects on fee payers and on service‑levels—with a particular focus on potential impacts for lower‑income and vulnerable Californians—as well as how readily solutions can be implemented. In some cases, the Legislature may want to consider a combination of solutions to help mitigate potential impacts. In determining which funds to prioritize for more near‑term action, we recommend the Legislature consider how soon the funds might become insolvent, the magnitude of the potential insolvencies, potential near‑term implications for spending and service levels, and how long it will take to implement the option or set of options. In the subsequent sections of this report we offer specific comments regarding time lines and considerations for addressing each individual fund.

Special Funds at Risk of Insolvency

In the sections below, we discuss each of the major funds that we have identified as being at risk of insolvency in more detail, including relevant background, details on the fund condition, and comments and recommendations for the Legislature to consider when it weighs its options for addressing these funds. (As noted previously, we discuss the DPR Fund proposal and associated recommendations in a separate publication.)

Hazardous Waste Control Account

Background

HWCA Funds Support the Regulation of Hazardous Waste. HWCA primarily supports activities the Department of Toxic Substances Control (DTSC) conducts related to regulating the generation, storage, transportation, and disposal of hazardous waste through permitting, compliance monitoring, and enforcement of noncompliance.

HWCA Restructured as Part of a Larger DTSC Reform Package. Budget trailer legislation adopted as part of the 2021‑22 budget package, Chapter 73 of 2021 (SB 158, Committee on Budget and Fiscal Review), restructured and increased the charges that support DTSC’s two major fund sources: HWCA and the Toxic Substances Control Account (TSCA). The resulting revenues were intended to (1) solve longstanding structural deficits in HWCA and TSCA, (2) support a new Board of Environmental Safety (BES) (discussed below), (3) support programmatic expansions that would better enable DTSC to protect people and the environment from toxic substances, and (4) build sufficient reserves in both accounts. For HWCA specifically, SB 158 replaced several prior fees with a new generation and handling fee and also increased existing facility fees. (We discuss these fees in greater detail in the section below.) While the legislation was enacted as part of the 2021‑22 budget package, the state did not begin to receive additional revenues until 2022‑23 due to the timing of how charges for both accounts are collected.

Senate Bill 158 also established BES within the department. Besides hearing permit appeals for hazardous waste facilities and providing strategic guidance to the department, beginning in 2023‑24 the five‑member board is responsible for setting charge levels for HWCA and TSCA. Specifically, the board is responsible for setting charges annually to align revenues from both accounts with the amount of expenditures authorized by the Legislature through the annual budget act.

HWCA Revenues Primarily Come From Two Major Regulatory Fees. Funding for HWCA primarily comes from the generation and handling fee (established in SB 158) and facility fees. The generation and handling fee is charged on a per‑ton basis to all entities that generate five or more tons of hazardous waste in a calendar year, while facility fees are annual charges levied on permitted facilities that treat, store, or dispose of hazardous waste. Senate Bill 158 set rates for both fees for 2022‑23, but authorized BES to adjust rates each year starting in 2023‑24.

Lower‑Than‑Projected Generation and Handling Fee Revenues Reestablished HWCA Deficit in 2022‑23. During the enactment of SB 158, the new generation and handling fee was set at $49.25 per ton and was projected to generate approximately $81 million in total revenues in 2022‑23. However, in the middle of 2022‑23, DTSC indicated that these revenues were coming in significantly below what had been anticipated and would only generate about $40 million that year. The lower‑than‑projected revenues reestablished the structural deficit within HWCA in 2022‑23 and set the fund on a path to insolvency in 2023‑24. The department’s preliminary analysis of the issue indicated the shortfalls were attributable to a combination of three primary factors: (1) a reduction in the amount of hazardous waste generated; (2) a higher utilization of government fee exemptions, such as related to a government entity removing or remediating hazardous waste caused by another entity; and (3) nonpayment or low payment of fee amounts owed.

2023‑24 Budget Package Authorized Special Fund Loans for HWCA. To address the revenue shortfall, the 2023‑24 budget provided $55 million in special fund loans—$15 million from TSCA and $40 million from the Beverage Container Recycling Fund—to support HWCA. (Budget bill language currently requires DTSC to repay both loans by June 30, 2026.) The loans were intended to allow HWCA to cover its planned expenditures in both 2022‑23 and 2023‑24. The loans also avoided the need for BES to increase the generation and handling fee in 2023‑24. This approach was adopted to provide DTSC with additional time to conduct a more in‑depth analysis of the revenue shortfalls and to identify a potential solution. The department was authorized to use a small portion of the loans to support this analysis and to improve fee administration and data collection.

Insolvency Projected in 2024‑25

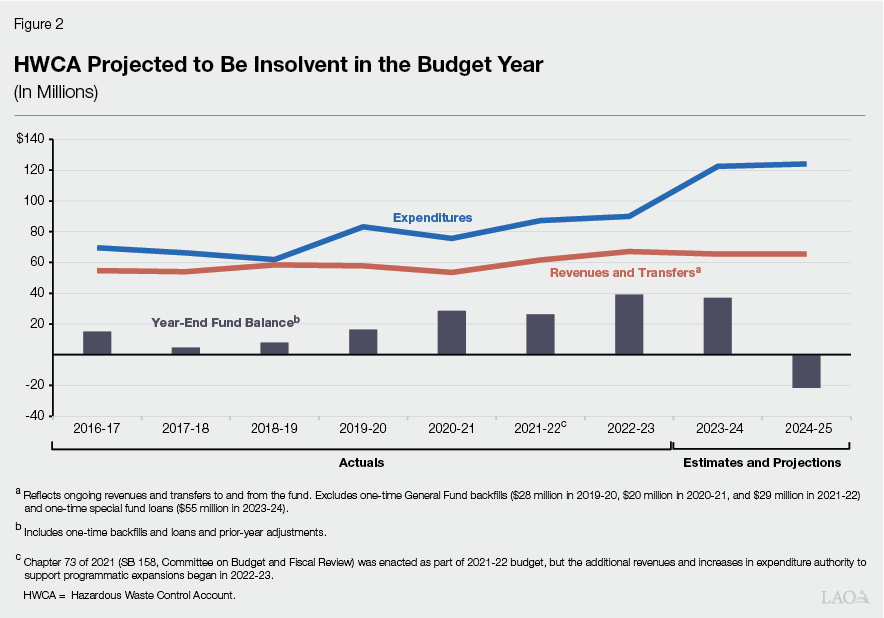

HWCA Projected to Be Insolvent in the Budget Year. As shown in Figure 2, HWCA has experienced a longstanding structural deficit between its ongoing revenues and expenditures. The state has responded by providing a series of one‑time General Fund backfills to keep the fund solvent, which is primarily how the fund balance has remained positive. The reform package was intended to address the structural deficit and generate additional ongoing revenues for HWCA to support both existing services and programmatic expansions. However, the lower‑than‑projected generation and handling fee revenues have prevented this from being accomplished. Under the administration’s estimates, HWCA is projected to become insolvent in the budget year, absent any corrective action. We note that the department is in the process of gathering revenue data from generation and handling fees that are currently being collected, which could change this projection—potentially for the better or for the worse. Accordingly, uncertainty still exists around the exact magnitude of shortfall that the state will need to address both in the budget year and on an ongoing basis. For instance, higher‑than‑expected revenues and/or lower‑than‑expected spending levels in the current year could shrink the anticipated deficit and reduce the magnitude of solutions needed in the budget year.

Administration Indicates Proposal Forthcoming at May Revision. DTSC indicates that it still is in the process of completing its analysis of the causes of the HWCA revenue shortfall, along with collecting updated revenue information. The department has stated that it will use this analysis as the basis for a proposal to address the 2024‑25 revenue gap that will be included as part of the May Revision.

LAO Comments

Reducing HWCA Expenditures Could Have Negative Implications for Health and Safety. As discussed earlier, generally the Legislature has two key categories of ongoing options for addressing structural fund imbalances: increase revenues (including by raising charges or through loans and transfers) or reduce expenditures. In the case of HWCA, the latter option could raise some concerns. In addition to addressing the structural deficits within HWCA and TSCA, a central component of the recent governance and fiscal reform package the Legislature enacted was to ensure that funding levels in both accounts were sufficient to support DTSC in better delivering on its mission and statutory authorities. For activities supported by HWCA, this included improving hazardous waste generator inspections and enhancing criminal enforcement investigations. Given that the Legislature recently identified the department’s current HWCA expenditure levels as being essential to protecting the public and environment from hazardous waste, this suggests that reducing them could result in a resumption of the safety concerns that initially led to the reform. This does not mean that opportunities for some savings do not exist. For example, the Legislature potentially could direct the department to implement program efficiencies that reduce cost pressures on HWCA and still allow for important services and protections. However, the Legislature likely will want to proceed with caution in considering any reductions to the activities supported by HWCA and ensure they do not result in increased hazards for Californians. Moreover, identifying enough efficiencies to fully address the fund’s structural deficit and maintain essential activities is highly unlikely.

Legislature Has Several Options to Provide Support for HWCA. Given concerns about reducing DTSC’s expenditures and activities, the Legislature might instead want to consider (1) increasing HWCA revenues and/or (2) identifying other fund sources to backfill HWCA. Two primary pathways exist for increasing revenues. First, the Legislature could defer to BES to use its statutory authority to raise the generation and handling fee and align revenues with the amount of 2024‑25 expenditures authorized for HWCA. Second, the Legislature could begin to develop its own proposal to increase the amount of revenues collected from the generation and handling fee. For instance, one factor leading to the shortfalls is a higher utilization of government fee exemptions. The Legislature could reduce these exemptions and thereby apply the fee to more payers and generate additional revenues. In addition to raising revenues, the Legislature could identify other fund sources to backfill HWCA, similar to the approach it took in the 2023‑24 budget. We note that utilizing this option may be more difficult given the overall budget problem with which the state is grappling. Furthermore, the Governor’s budget already proposes using special fund loans—such as from the Beverage Container Recycling Fund—to support the General Fund, which limits the ability to utilize such sources to support HWCA.

Recommendation

Use Spring Budget Process to Consider Options. The administration plans to propose a solution for HWCA as part of the Governor’s May Revision. While a solution is needed, this schedule limits the time the Legislature has to (1) weigh the benefits and trade‑offs of the administration’s proposal and (2) develop a proposal that aligns with its own priorities. Given these constraints, we recommend the Legislature begin this spring to weigh the various options it has for addressing the HWCA revenue shortfall. Considering the merits and trade‑offs associated with these options now would put the Legislature in a better position to evaluate the Governor’s proposal and alternative solutions in May when the budget deadline and need for action are more pressing.

Motor Vehicle Account

Background

MVA Supports Various State Programs. MVA is the primary funding source for CHP and DMV. The account also provides some funding for the California Air Resources Board. The uses of most MVA revenues are constitutionally limited to the administration and enforcement of laws regulating the use of vehicles on public highways and roads, as well as certain transportation activities.

Revenues Mainly Come From Vehicle Registration Fees. For 2023‑24, MVA revenues are estimated to total about $4.7 billion. Of this amount, nearly $4.1 billion (87 percent) is projected to come from vehicle registration fees. The remainder largely is generated by other DMV fees such as driver license fees. (We note that DMV also collects various other fees at the time of vehicle registration that are not deposited into MVA, such as vehicle license fees, truck weight fees, and an additional registration fee charged to owners of zero‑emission vehicles.)

Fund Rapidly Heading for Insolvency

Expenditures Outpacing Revenues. Between 2018‑19 and 2023‑24, MVA revenues have increased by $714 million (18 percent) while expenditures have increased by about $1 billion (26 percent). Since 2021‑22, annual expenditures have exceeded yearly revenues, resulting in a structural imbalance. Some of the major expenditure cost drivers have included (1) replacement of older CHP area offices and DMV field offices, (2) increased employee compensation costs—which have been driven by both increases to staffing levels and growing salary and benefit costs at CHP, (3) workload related to the issuance of new driver licenses and ID cards that comply with federal standards—commonly referred to as “REAL IDs,” and (4) supplemental pension plan repayments that began in 2019‑20. (These payments are related to a 2017‑18 budget action that borrowed from the General Fund for a large one‑time contribution to the state employee pension fund, requiring future repayment from all relevant funds that make employer pension contributions, including MVA. Over the next 30 years, MVA is expected to receive savings that outweigh these near‑term loan repayment expenditures due to slower growth in employer pension contributions.) Despite this gap between revenues and expenditures, MVA has remained solvent thus far due to the state actions described in the next paragraph and by relying on its reserves. However, these reserves are rapidly declining. MVA entered 2021‑22 with $585 million in reserves but its year‑end balance is projected to drop to $130 million by the beginning of 2024‑25.

State Has Undertaken Previous Efforts to Address Deficits and Delay Insolvency. Over the last couple of decades, MVA has experienced periodic deficits and risks of insolvency. In response, the state has taken various actions to shore up the fund. Some of these past solutions provided temporary relief, such as the state making a one‑time repayment of loans that previously were provided from MVA to the General Fund and delaying supplemental pension plan repayments to the General Fund (which temporarily reduced MVA expenditures but created additional out‑year liabilities). Other solutions provided longer‑term solutions, including (1) ending a previous practice of transferring about $90 million annually from MVA to the General Fund; (2) authorizing vehicle registration fees to be adjusted annually based on the percent change in the California Consumer Price Index (CPI) to account for inflation; (3) shifting certain programs from MVA to other fund sources; and, as we discuss in more detail below, (4) the state recently has shifted away from using up‑front cash from MVA to pay for CHP’s and DMV’s facility needs.

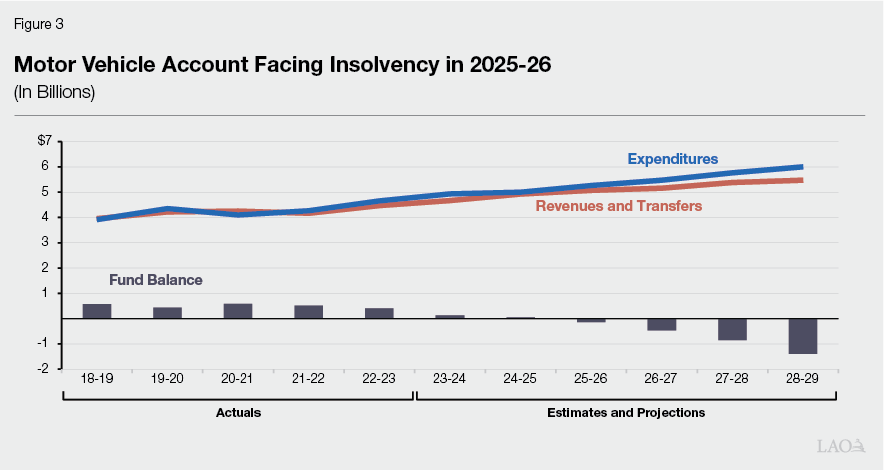

Due to Ongoing Structural Imbalance, MVA Projected to Become Insolvent in 2025‑26. Despite the previous efforts to address MVA’s condition, the severity of the fund’s imbalance is expected to become worse in the near term, with expenditures growing about 1 percent faster than revenues over the next several years. Due to this imbalance, MVA is expected to fully exhaust its reserves and become insolvent in 2025‑26, as shown in Figure 3. Specifically, the administration projects expenditures will exceed available resources by roughly $140 million in 2025‑26. If left unaddressed, expenditures would continue to outpace revenues, resulting in a negative fund balance of $1.4 billion in 2028‑29. For context, total MVA revenues are projected to be about $5 billion in 2024‑25. By 2028‑29, these revenues are only projected to increase by about $500 million while expenditures are projected to increase by roughly $1 billion.

LAO Comments

Governor Proposes New Spending From MVA. The Governor’s budget does not include a proposal to address MVA’s fund condition or structural deficit. In contrast, the January budget includes various proposals for DMV and CHP that would increase cost pressures for MVA. Specifically, the Governor proposes $18 million in 2024‑25 (including $10 million ongoing) from MVA for various DMV programs. In addition, the Governor proposes $4 million annually in ongoing spending from MVA for outside counsel to represent CHP and its officers in civil litigation cases related to officer‑involved shootings.

Debt Service for Infrastructure Projects Could Create Additional MVA Cost Pressures. CHP and DMV both operate large numbers of facilities across the state, many of which have significant needs. Traditionally, CHP’s and DMV’s facility projects—such as office replacements—have been funded up front with cash from MVA. However, due to concerns about MVA’s condition, over the past several years, the state has explored alternative ways to fund CHP and DMV facilities. In 2019‑20, this included issuing lease revenue bonds with plans to repay the debt service from MVA, in an effort to spread the costs of the projects over time and limit near‑term pressures on the fund. In 2021‑22 and 2022‑23, when the state was experiencing a budget surplus, the state provided cash from the General Fund to support such projects. However, as the General Fund condition has worsened, funding for recent projects has been shifted to lease revenue bonds. While this approach reduces costs to move forward with the projects in the near term, repaying the bonds will create cost pressures in future years. Whether the General Fund or MVA will bear the burden of these future costs currently is unclear, as the fund source for repaying the bonds has not yet been determined. The administration indicates that these decisions will be made during annual budget deliberations beginning in 2025‑26.

Automatic Pay Increases for CHP Officers Could Impact MVA Cost Pressures. The impact future employee compensation costs will have on MVA’s fund condition is somewhat uncertain and depends on future pay trends decided upon by select local governments. For more than 40 years, statute has based highway patrol officers’ compensation on an average of specified elements of compensation provided to peace officers employed by five local jurisdictions. The five jurisdictions are Los Angeles County and the Cities of Los Angeles, Oakland, San Diego, and San Francisco. Because these statutory pay increases are wholly dependent on decisions made by the five local governments, actual pay increases for CHP officers could be higher or lower than current assumptions—potentially impacting MVA cost pressures in future years.

Temporary Actions Could Delay, but Not Prevent, Insolvency. The Legislature has a couple of options for actions that could temporarily delay insolvency for MVA. First, the Legislature could direct the administration to make a loan or transfer to MVA from another fund source such as the General Fund. However, the current General Fund condition and overall budget problem would make this challenging. Second, the administration could temporarily suspend supplemental pension plan repayment requirements. Doing so, however, would result in higher cost pressures for MVA in the near future because the principal and interest for the loan still would need to be repaid by June 30, 2030. Moreover, suspending these repayments would only delay MVA’s insolvency by a few months.

Legislature Could Address MVA Fund Condition Through Reducing or Constraining Costs… As noted, MVA’s expenditures are outpacing revenue growth and cost pressures could be higher than projected depending on future lease revenue bond debt service decisions and employee compensation trends. To help address the fund condition, the Legislature could take steps to reduce or constrain expenditures. For example, the Legislature could reduce overall employee compensation costs by cutting the number of positions at DMV and CHP. However, such actions would result in a decrease in the level of service the departments would be able to offer, which could affect both public satisfaction (in the case of DMV) and safety (with regard to CHP). Going forward, the Legislature also could consider MVA’s fund condition when it is evaluating agreements negotiated between the administration and the employee unions that represent the majority of DMV and CHP employees pertaining to pay and other benefits. Specifically, the Legislature could take into consideration the level of costs the fund can support as one of the factors it weighs when considering whether to approve these draft agreements. As we noted previously, the state currently has limited control over CHP officer pay because it is determined based on a formula. However, the Legislature could consider changing this methodology to regain more decision‑making power and the ability to align costs with what MVA can afford to support.

…And/Or Through Increasing Revenues. The Legislature also could help MVA remain solvent by taking steps to increase its revenues. One option would be to raise vehicle registration fees—either through a base increase or by changing the methodology for annual fee adjustments such that they exceed changes in the CPI. A strong policy rationale exists for raising fees in that it would continue to task vehicle owners with paying to support the services from which they benefit. Based on the number of vehicles currently registered in California, we estimate that every $1 increase in vehicle registration fees would increase MVA revenues by about $36 million. However, one key trade‑off to consider is that increasing fees would result in additional costs to households and businesses that own vehicles. This could be particularly burdensome for lower‑income households. As of January 1, 2024, base vehicle registration fees were $74 but once other fees (such as weight fees and vehicle license fees) are factored in, the average cost vehicle owners pay when registering a vehicle is $329.

Recommendations

Consider MVA Cost Pressures When Evaluating New Spending Proposals. As noted, the Governor’s budget includes proposals that would increase expenditures from MVA by roughly $22 million in 2024‑25 and $14 million ongoing. Regardless of the merits of these specific proposals—and absent actions to address the MVA fund condition—approving them will make the structural deficit worse and hasten the time line for MVA going insolvent. Until a plan is put in place to address MVA’s structural deficit, we recommend the Legislature set a high bar for considering approval of any proposals that create additional MVA cost pressures and accelerate the risk of insolvency.

Develop Plan to Ensure Fund Remains Solvent. In order to remain solvent, MVA expenditures and revenues must be brought into balance. As such, we recommend that the Legislature develop a plan to address MVA’s structural deficit on an ongoing basis. To achieve ongoing sustainability for the fund, the state will need to reduce MVA’s costs, increase the fund’s revenues, or adopt some sort of combination of these strategies. To help determine which options best align with legislative priorities, the Legislature could hold hearings to get a better understanding of the fund condition, any actions the administration is considering to address the problem, and the trade‑offs associated with options such as raising fees or reducing positions at CHP and DMV.

Consider Cost Pressure Impacts From Employee Compensation. Even if the Legislature takes action to address MVA’s current deficit, the fund could be at risk of future insolvency if expenditures related to employee compensation outpace revenues in the future. When addressing the MVA fund condition, the Legislature will want to consider how the fund could absorb future increases in employee compensation. The Legislature also might want to consider whether changes to the methodology for setting CHP officer pay could be needed to increase the state’s flexibility for controlling MVA expenditures. Similarly, the Legislature might want to consider MVA’s fund condition and impact of employee compensation costs when evaluating future memoranda of understanding negotiated between the administration and the employee unions that represent the majority of DMV and CHP employees. While the state currently has limited discretion over the formula that determines CHP officer pay, the Legislature could change this methodology to regain more decision‑making power.

Environmental License Plate Fund

Background

Fund Supports Specific Resources and Environmental Protection Activities. ELPF was established in 1979 to fund various natural resources and environmental protection‑related programs. Existing state law restricts the use of ELPF monies to program administration and the following purposes:

- Control and abatement of air pollution.

- Acquisition, preservation, and restoration of natural areas or ecological reserves.

- Purchase of real property for park purposes and addressing deferred maintenance at state parks.

- Environmental education.

- Protection of nongame species and threatened and endangered plants and animals.

- Protection, enhancement, and restoration of fish and wildlife habitat, and related water quality.

- Reduction of the effects of soil erosion and the discharge of sediment into the waters of the Lake Tahoe region.

- Scientific research on the impacts of climate change on California’s natural resources and communities.

Fund Supported Primarily by License Plate Sales. The fund is primarily supported from the sale and renewal of personalized motor vehicle license plates, as well as a portion of fees on the sale and renewal of certain specialty plates (such as “Whale Tail” and 1960s Legacy plates).

ELPF Fund Condition Continues to Deteriorate

Structural Imbalance Has Arisen as Expenditures Have Been Added to the Fund and Revenues Have Not Kept Pace. ELPF has experienced periodic fund condition challenges in the past. Most recently, a structural imbalance has emerged related to both expenditures and revenues:

- Increasing Expenditures. First, ELPF supports operating activities at various departments, and these costs have increased over time due to rising employee compensation and other factors. Second, numerous new or expanded one‑time and ongoing activities have been funded using ELPF in recent years. These include a K‑12 access program, a water data access program, a beaver restoration program, the Bolsa Chica Lowlands restoration project, and the Clear Lake rehabilitation project. ELPF also has been used to support new staff at the Truth and Healing Council and Forest Management Task Force, as well as to cover increases in administrative support for a few conservancies, among other activities.

- Revenues Have Not Kept Pace With Increasing Expenditures. ELPF revenues have been relatively flat over the past few years. Notably, the administration indicates that when it proposed augmentations in expenditures to the fund in recent years, it assumed that revenues from additional license plates would increase sufficiently to support both those new costs and the rising costs of existing activities. However, the revenue growth the administration had anticipated has not yet materialized.

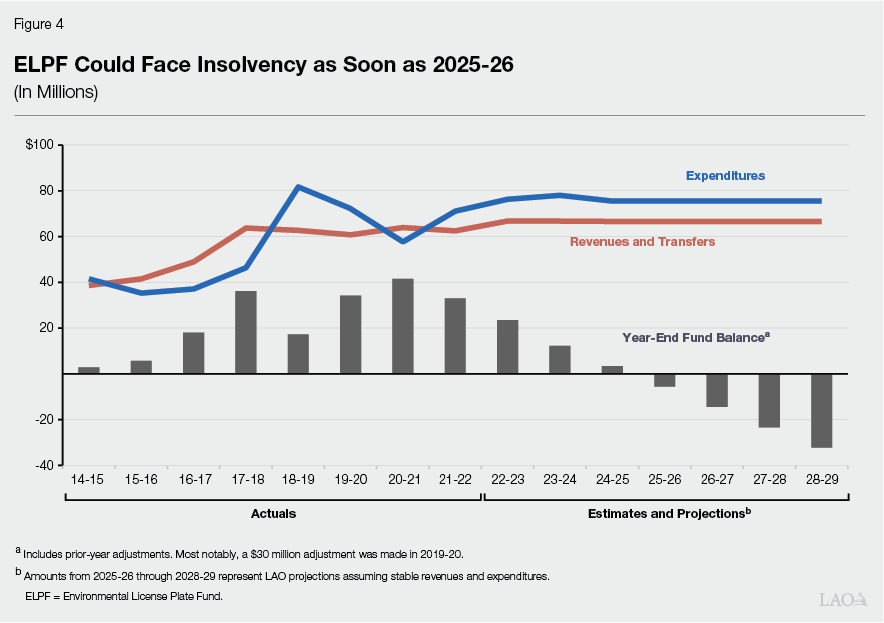

ELPF Could Become Insolvent by 2025‑26. Over the budget window, the administration estimates the fund will have an annual gap of approximately $9 million between existing revenues (roughly $67 million) and current expenditures (roughly $76 million). Given this structural imbalance, under the administration’s estimates, ELPF will maintain a reserve of just $3 million at the end of 2024‑25. Based on these trends, we estimate the fund will be insolvent by 2025‑26 if revenues and expenditures remain stable and corrective actions are not taken. We highlight these estimates in Figure 4. (While the administration has not provided a fund condition projection for ELPF, it indicates it expects revenues and expenditures to be stable in the coming years.)

Administration Indicates It Is Taking Current‑Year Actions, Monitoring Fund Condition, and Considering Future Options. The California Natural Resources Agency (CNRA) indicates it is relying on one‑time savings—including $2 million from the Department of Fish and Wildlife—as a mechanism to help ensure the fund balance is not depleted in the current year. The agency also is working on expanding the pool of available license plates—such as through partnerships with National Football League team foundations on specialized plates—to attract additional customers who do not yet have a specialized plate and thereby generate additional revenue for ELPF. The agency states that it also is monitoring ELPF’s fund condition and considering potential additional options. The administration did not provide a proposal to address ELPF’s fund condition as part of the January budget.

LAO Comments

Given Potential Near‑Term Insolvency, Prompt Action Makes Sense. As discussed above, ELPF could face insolvency as soon as 2025‑26, absent corrective actions or an unexpected increase in revenues. Accordingly, actions to address the condition of the fund are likely to be needed within roughly the next two years.

Legislature Has Various Options for Addressing Condition of ELPF. Some of the types of actions that the Legislature has considered when ELPF has encountered shortfalls in the past include (1) increasing license plate fees; (2) reducing the number of programs funded by ELPF; (3) requiring departments funded by ELPF to achieve certain levels of targeted savings (such as by holding positions vacant); and (4) shifting the costs of some activities that were previously funded by ELPF to other accounts, such as SPRF. The various options come with trade‑offs, such as which programs to maintain and who will bear the associated costs—whether personalized and specialized license plate holders, general taxpayers, or fee payers associated with other funds. Moreover, as discussed later, SPRF also currently faces a structural imbalance, along with several other special funds across the resources and environmental protection areas highlighted in this report. The structural imbalances within these funds currently would make it difficult for them to support additional costs. Additionally, while in principle some costs could be shifted to the General Fund—as has also been done in the past—this also would be difficult given its current condition.

Additional Information on Options Would Help Inform Legislative Decision‑Making. Obtaining more details on the options CNRA is considering and the associated trade‑offs and impacts would be helpful for the Legislature as it begins to grapple with how it might address deficits within ELPF. For example, any estimates the administration has for the amount that could be raised by various license plate fee increases could help inform legislative decision‑making. Additionally, the Legislature would benefit from additional details on the myriad of programs currently funded by ELPF so it can prioritize across them and determine if any could be good candidates for reductions or shifts to other fund sources.

Recommendation

Adopt a Solution to ELPF Imbalance No Later Than 2025‑26, Informed by Information From the Administration. Given our ELPF projections, we recommend that the Legislature adopt a solution to bring long‑term stability to the fund no later than 2025‑26. We recommend the Legislature request additional information from the administration as part of the spring budget hearing process—such as on the estimated revenues from potential license plate fee increases and about programs currently supported by the fund—to help it begin to craft its preferred solution.

Harbors and Watercraft Revolving Fund

Background

Fund Supports Boating‑Related Activities. State departments use HWRF to support various boating‑related activities, including the management of invasive aquatic plants and species, as well as local assistance grants for boat safety programs. The administration estimates that a total of $53 million will be spent from the fund in the current year, primarily by four departments—the Department of Parks and Recreation (Parks), the Department of Fish and Wildlife, the California Department of Food and Agriculture, and DMV.

Most Revenue Generated From Vessel Registration Fees and Fuel Taxes. HWRF receives a significant portion of its revenues from vessel registration and renewal fees, as well as a transfer of gas tax revenues from the Motor Vehicle Fuel Account (MVFA). Vessel registration renewals in California are conducted on a biennial basis. As a result, fee revenue for HWRF fluctuates predictably each year. The current fee rates are:

- Initial Registration Fees. The state charges an initial registration fee of $20 for most vessels that are registered in odd years and $10 for those registered in even years (the second year of the two‑year cycle).

- Renewal Fees. The state also charges a registration renewal fee that is due every two years in odd‑numbered years totaling $20 for most vessels.

Fund Imbalance Continues to Present a Challenge, Despite Recent Actions

HWRF Has Faced Fund Condition Issues for a Few Years. In recent years, HWRF has faced fund condition challenges, as its annual expenditures have exceeded its typical level of revenues. As we discussed in our February 2021 analysis, this imbalance arose in part because expenditures grew over time, driven by rising employee compensation, a growing prevalence of aquatic invasive species, and because new activities were shifted onto the fund. Meanwhile, revenues into the fund from vessel registration and renewal fees across the two‑year fee cycle have remained largely stable, as registrations have remained mostly flat and the state has not increased existing vessel registration and renewal fee levels (even for inflation) since 2005. Additionally, the 2019‑20 budget made a technical correction to how gas taxes are allocated that resulted in a significant reduction in the amount of annual revenues that are transferred from MVFA into HWRF, thus leading to a decline in overall revenue to the fund.

Legislature Has Taken Some Steps to Address HWRF’s Fund Condition in Recent Years. Initially, Parks covered the HWRF shortfall primarily by depleting its reserves (including savings from underutilized grant programs). However, in 2021‑22, the administration proposed a package of solutions to address the HWRF fund condition, which included (1) a one‑time increase in the existing biennial fees charged for vessel registrations and renewals from $20 to $70 (and from $10 to $35 for new registrations in even years), (2) $20 million in reductions to various funded programs, and (3) $10 million in one‑time General Fund support. This proposal would have provided temporary stability to the fund, but it would not have implemented a permanent solution as the deficit was expected to reemerge by 2024‑25. Ultimately, the Legislature modified the administration’s proposed package of solutions in 2021‑22 to (1) reject the proposed fee increase, (2) approve the proposed reductions to programs, and (3) provide an augmented level of temporary General Fund support compared to the Governor’s proposal—$30 million in 2021‑22, $30 million in 2022‑23, and $21 million in both 2023‑24 and 2024‑25. To facilitate the development of a permanent solution, the Legislature also adopted budget bill language requiring Parks, in consultation with stakeholders and staff of the relevant fiscal and policy committees of the Legislature, to develop a new proposal that included a combination of fee increases, expenditure reductions, and other actions designed to keep HWRF in structural balance on an ongoing basis. The budget bill language further required Parks to provide the proposal no later than January 2023.

In May 2023, the Governor proposed a second package of solutions to address HWRF’s fund condition, informed by a stakeholder process undertaken by Parks as required by statute. This revised proposal included (1) $11.3 million in additional reductions across two programs and (2) an increase in vessel registration fees from $20 to $80 biennially (and from $10 to $40 for new registrations in even years). This proposal would have provided temporary relief to the fund, but the administration still estimated that further adjustments would have been needed in 2029‑30 to retain solvency. Given the limited time to consider the proposal and some stakeholder concerns, the Legislature adopted the Governor’s proposed programmatic cuts but did not adopt any changes to the fee levels or structure.

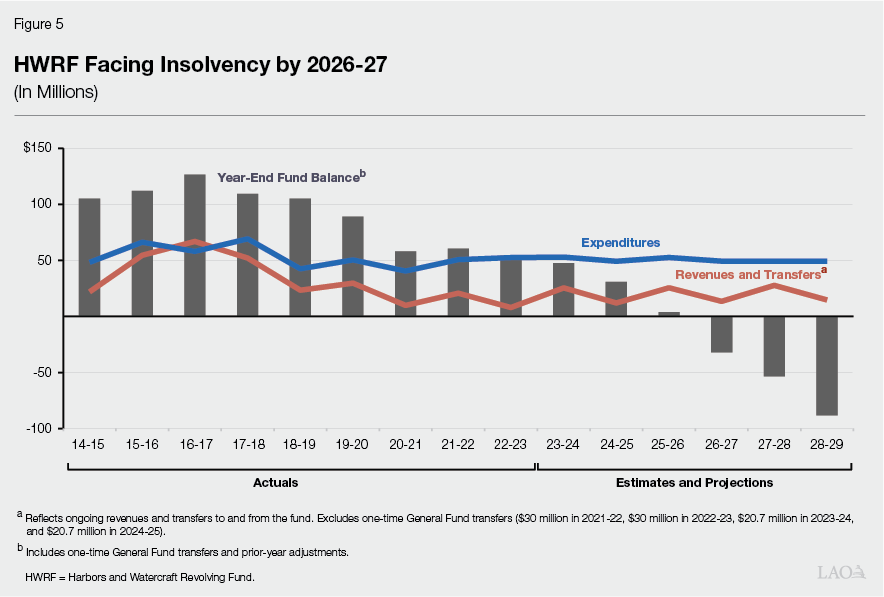

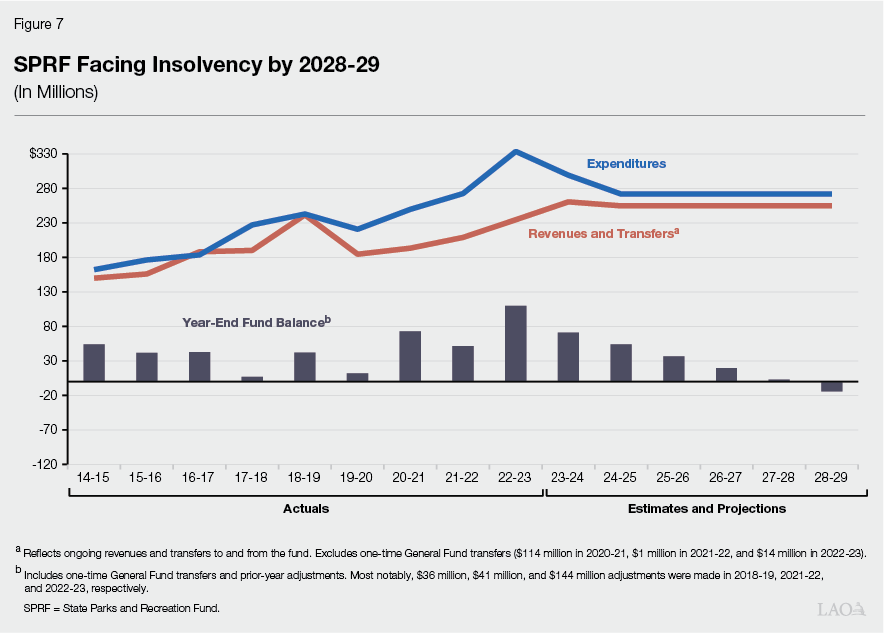

Despite These Actions, HWRF Still Has an Ongoing Structural Imbalance and Faces Insolvency by 2026‑27. The actions taken by the Legislature in recent years—namely the General Fund transfers and expenditure reductions—have improved the condition of HWRF on a short‑term basis. However, the fund still faces a structural imbalance. Specifically, the administration estimates that absent any corrective actions, the fund has an annual gap of approximately $30 million across its two‑year fee collection cycle between existing revenues of roughly $20 million and current annual expenditures of roughly $50 million. As shown in Figure 5, this imbalance is expected to result in HWRF depleting its remaining reserve and becoming insolvent by 2026‑27.

Administration Indicates It Is Monitoring Fund Condition and Considering Options. Parks indicates that it continues to explore options for addressing the condition of HWRF, including potentially increasing fees in the future. However, the Governor has not included a proposal to address HWRF’s structural imbalance as part of the January budget.

LAO Comments

Given Structural Imbalance, Prompt Action Makes Sense. We find that additional actions to provide long‑term stability for HWRF are important, and as such, taking action soon to provide this stability would make sense. Specifically, while the fund condition projection shows insolvency in 2026‑27, a solution likely will be needed no later than 2025‑26. This is because (1) Parks will need time to implement a fee increase once it has been adopted and (2) a lag exists before fee increases are fully reflected in revenues due to the fund’s two‑year fee cycle, which provides markedly more revenue in odd years. Additionally, if the Legislature were to take action in 2024‑25, it could potentially reduce the size of the planned budget‑year General Fund transfer of $21 million, thereby capturing the savings as a General Fund solution.

Reasonable to Include a Fee Increase as Part of a Permanent Solution. We find that a balanced approach to addressing HWRF’s deficit—one that reflects both expenditure reductions and increased revenues—makes sense. So far, the state has implemented significant reductions to the programs funded from HWRF and the General Fund has provided substantial one‑time support. However, continuing to rely exclusively on these two approaches would be problematic because (1) further expenditure reductions could have significant negative impacts on the programs that HWRF supports, (2) the General Fund is not in a position to continue providing support, and (3) boat users paying at a level commensurate with the benefits they receive through HWRF is appropriate. Accordingly, we think a fee increase should be a key part of a permanent solution. This would be consistent with the budget bill language adopted by the Legislature in 2021‑22, which envisioned a fee increase as a component of addressing the fund condition. Additionally, the fees that support HWRF have not been increased in nearly 20 years, so adjusting them to meet current costs and demands on the fund is warranted.

Recommendation

Adopt a Permanent Solution to Fund Imbalance—Including a Fee Increase—No Later Than 2025‑26. For the reasons cited above, we recommend the Legislature take action no later than 2025‑26, but ideally in 2024‑25, to address the condition of HWRF. While the Legislature could consider a mix of solutions, we recommend it rely more heavily on fee increases given that fees have not been adjusted in almost 20 years and significant programmatic cuts already have been made. The Legislature could adopt a new fee structure similar to the one proposed by the Governor in May 2023, or it could consider various other options for fee amounts and design, such as those we discussed in our February 2021 report. We also recommend that whatever solution the Legislature adopts be crafted to bring long‑term solvency to the fund, such as by incorporating a cost‑of‑living adjustment to enable fees to keep pace with inflation and emerging needs.

Energy Resources Programs Account

Background

Main Operating Account for the California Energy Commission (CEC). The state uses ERPA funds to support various energy programs and projects, including CEC’s operations. ERPA is funded through a surcharge on retail electricity sales, originally set at $0.0001 per kilowatt hour (kWh) back in 1974. It was then raised to $0.0002 sometime between 1984 and 2002. Subsequently, Chapter 1033 of 2002 (AB 3009, Committee on Budget) raised the maximum allowable surcharge from $0.0002 per kWh to $0.0003 per kWh and gave CEC the authority to adjust rates up to that statutory cap. CEC set the surcharge at the cap of $0.0003 per kWh in 2018. The ERPA surcharge currently costs the average residential ratepayer about 16 cents per month, or $2 annually. It generated about $72 million in revenue in 2022‑23 and similar amounts in recent prior years.

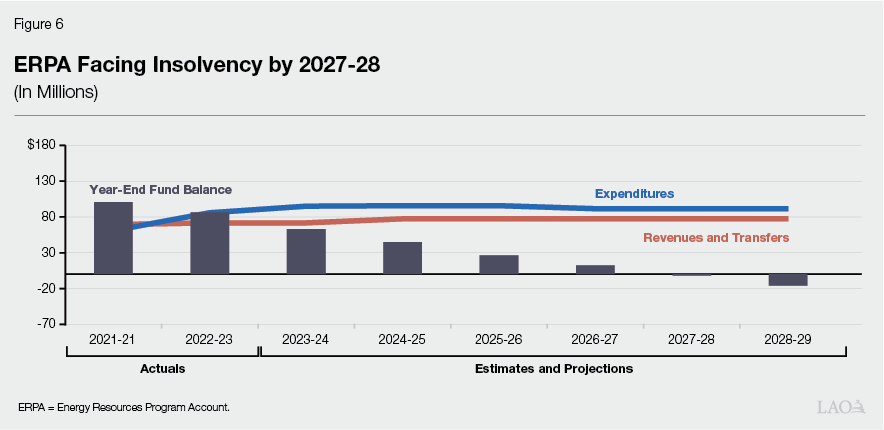

ERPA Projected to Go Insolvent in 2027‑28. As shown in Figure 6, ERPA is in a structural deficit, with its ongoing revenues failing to keep pace with its increasing expenditures. This imbalance is primarily resulting from: (1) the continued rise of expenditures due to salary and benefit costs for existing staff as well as growing costs to implement new chaptered legislation each year, (2) CEC being constrained by the current statutory cap from setting the surcharge at a level that would generate revenues that keep pace with inflation and statutorily required expenditures, and (3) the current exemption of behind‑the‑meter (BTM) solar generation from paying into ERPA. The growth of BTM solar in recent years has depressed ERPA revenues as numerous customers who formerly purchased traditional retail electricity (which carried with it an associated ERPA surcharge) have made the transition to solar panels (and therefore are now exempt from paying the surcharge). As shown in the figure, the fund’s reserves have helped keep it solvent since the structural deficit materialized and are projected to continue doing so for the next few years, but the administration estimates these balances will be exhausted by 2027‑28.

Administration Projects Increased Electricity Sales Will Be Insufficient to Cover Deficit. Residential electricity consumption is expected to increase over the next several years due to widespread adoption of electric vehicles and greater home electrification. However, CEC projects this increase (which it estimates will total 1.68 percent annually between 2022 and 2035) still will not generate enough additional revenue for ERPA to cover its structural deficit at the current surcharge rate.

Administration Has Proposed Raising ERPA Surcharge Each of the Past Two Years. The administration has proposed increasing the statutory cap for the ERPA surcharge as part of the budget process twice in the past two years—in April 2022 and May 2023. These proposals ultimately were rejected by the Legislature.

Governor’s Proposal

Increases the ERPA Surcharge Cap and Authorizes Future Inflationary Increases. The Governor proposes to more than double the current surcharge cap, increasing it to $0.00066 per kWh. This would give CEC the ability to raise the ERPA surcharge up to this amount, beginning January 1, 2025. The administration notes that the new proposed cap is equal to indexing the original surcharge ($0.0001) to inflation in the years since its creation. Beginning January 1, 2026, and annually thereafter, the surcharge rate cap would be adjusted in an amount equal to the CPI. If and when CEC sets the surcharge at the new statutory cap, it would more than double current ERPA revenues (not including inflationary adjustments). At the current rate of electricity usage, surcharges set at the proposed new cap amount for current users would generate about $150 million annually and cost an average household about 32 cents per month.

Extends Charge to BTM Solar Owners. The Governor also proposes extending the ERPA surcharge to BTM solar customers based on how much energy their systems generate, beginning January 1, 2025. The administration estimates this would provide about $9.8 million in additional ERPA revenues based on the current surcharge rate (and therefore more than twice that amount if and when the surcharge were to reach the proposed new statutory cap, not including inflationary adjustments). About $4.5 million of this new revenue would come from applying the surcharge to about 1.7 million existing residential BTM solar customers in the state. On average, these customers would experience a monthly bill increase of about 23 cents per month. The remaining revenue would come from applying the surcharge to nonresidential locations with solar generation and nonutility generation facilities. To enable CEC to apply this charge, the Governor’s proposal would update the Revenue and Taxation code to require electric utilities to use a specified methodology to calculate the amount of kWh of electricity generated by a solar energy system.

LAO Comments

Surcharge Not Likely to Reach Cap Anytime Soon. The administration has indicated that, should the proposal be adopted, it would not proceed with raising the ERPA surcharge all the way to the new cap immediately. Rather, CEC states that its annual process for considering adjustments to the surcharge would be to (1) forecast its projected, allowable ERPA expenditures as approved in the most recent budget act; (2) evaluate whether those projections show that the ERPA fund balance would drop below a $20 million reserve (the administration’s identified “prudent reserve”); if so, (3) the CEC would propose a surcharge increase sufficient to cover the associated expenditures; and (4) CEC commissioners would hold a vote on the proposed increase at their November business meeting. Under this practice, the surcharge increase is not likely to hit the maximum cap for several years. This is because the current cap of $0.0003 per kWh is nearly, but not entirely, sufficient to cover ERPA’s current expenditures, so CEC will not have justification to adjust the surcharge up to the maximum allowable cap unless the Legislature authorizes significant and unanticipated new near‑term spending from ERPA.

Existing Law Places Checks on ERPA Expenditures… Because ERPA is not continuously appropriated, in general, the administration must submit a budget change proposal for legislative approval should it wish to add new expenditures and increase its spending authority from the fund (for example, to add staff to implement new activities). Moreover, CEC is unable to use ERPA revenues for any spending beyond its statutorily required duties and obligations. These guardrails provide some limitations on how CEC can use ERPA and the rate at which it can increase its spending. Without significant increases in spending authority from the Legislature, CEC will not have justification to significantly increase the ERPA surcharge, even if a higher cap technically provides it with more room to do so. This can provide the Legislature with some comfort that even if it approves the Governor’s proposal to notably increase the cap, through helping to control ERPA expenditures, it also can help control surcharges for ratepayers. The requirement that CEC commissioners approve ERPA increases also provides an opportunity for the Legislature (and stakeholders) to weigh‑in through public comment prior to them raising the surcharge.

…But Legislature Will Want to Carefully Monitor Growth in and Effectiveness of Expenditures. The Governor’s proposal would give CEC authority to raise ERPA revenues if the added expenses fulfill CEC’s statutorily required obligations and fall within the fund’s statutory spending level as authorized by the annual budget act. The Legislature will want to be diligent about monitoring how CEC is using the revenues, whether the activities the fund is supporting seem justified, and how quickly the activities are expanding and expenditures are growing. As part of this oversight, monitoring how quickly the surcharge rate charged by CEC is growing over the next several years also will be important. Particularly given that any increases to the surcharge will have impacts for ratepayers—albeit minor ones, as discussed next—the Legislature will want to make sure ERPA spending is well‑justified, cost‑effective, and helping to meet state goals and fulfill statutory obligations.

Cost Increase to Customers Would Be Minor, but Still Worthy of Scrutiny. Any proposal that increases electricity rates should be considered carefully. California’s electricity rates have increased at a rate far surpassing inflation in recent years, with rates charged by the state’s investor‑owned utilities increasing by nearly 90 percent over the past decade. Lower‑income households spend a larger share of their income on energy costs as compared to higher‑income households. In addition, meeting the state’s climate goals will be dependent on increasing electricity usage and moving away from fossil fuels, and customers may be reluctant to make electrification transitions should associated prices be too high. The Governor’s proposal will increase electricity rates, and as such bears particular scrutiny. However, even with this in mind, the proposed increase for the average residential customer will be minor, resulting in additional costs for most households totaling only a few cents each month. Given the importance of making sure CEC is well‑positioned to help the state meet its aggressive clean energy goals, these minor increases seem justified and not overly burdensome.

Extending Surcharge to BTM Solar and Incorporating Inflationary Adjustments Are Reasonable. As described above, the growth of BTM solar has eroded ERPA revenues while expenses have continued to grow. A strong policy rationale exists for extending the surcharge to these customers so they pay their “fair share” of supporting CEC’s statutorily required activities. The resulting charges would be modest, adding an estimated 23 cents per month to bills for the typical household BTM solar customer. In addition, tying the surcharge to inflation is a sensible strategy to ensure future revenue is sufficient to accommodate normal growth in baseline costs. This also will help ensure that inflationary changes will not be responsible for reestablishing a structural deficit. Adding this annual adjustment also will limit the need for repeated action by the Legislature in future years.

Recommendation

Approve Governor’s Proposal, but Monitor Necessity and Effectiveness of Both Existing and Future ERPA Spending. The Governor’s proposal is a reasonable approach to addressing the structural deficit in ERPA, which is projected to go insolvent in 2027‑28 absent legislative action. Moreover, the resulting impacts on ratepayers will be minor and CEC is unlikely to have justification for making notable increases to the surcharge in the near term. We recommend the Legislature adopt the Governor’s proposal, but constrain expenditure growth (and the resulting impacts to the surcharge applied to ratepayers) by continuing to closely monitor both future requests for increases to ERPA spending, as well as the need for and cost‑effectiveness of existing expenditures. This can help ensure the funds are being used for essential and worthwhile activities and avoid levying undue or rapidly increasing charges on ratepayers.

State Parks and Recreation Fund

Background