February 9, 2016

Perspectives on Helping Low-Income Californians Afford Housing

Summary

California has a serious housing shortage. California’s housing costs, consequently, have been rising rapidly for decades. These high housing costs make it difficult for many Californians to find housing that is affordable and that meets their needs, forcing them to make serious trade–offs in order to live in California.

In our March 2015 report, California’s High Housing Costs: Causes and Consequences, we outlined the evidence for California’s housing shortage and discussed its major ramifications. We also suggested that the key remedy to California’s housing challenges is a substantial increase in private home building in the state’s coastal urban communities. An expansion of California’s housing supply would offer widespread benefits to Californians, as well as those who wish to live in California but cannot afford to do so.

Some fear, however, that these benefits would not extend to low–income Californians. Because most new construction is targeted at higher–income households, it is often assumed that new construction does not increase the supply of lower–end housing. In addition, some worry that construction of market–rate housing in low–income neighborhoods leads to displacement of low–income households. In response, some have questioned whether efforts to increase private housing development are prudent. These observers suggest that policy makers instead focus on expanding government programs that aim to help low–income Californians afford housing.

In this follow up to California’s High Housing Costs, we offer additional evidence that facilitating more private housing development in the state’s coastal urban communities would help make housing more affordable for low–income Californians. Existing affordable housing programs assist only a small proportion of low–income Californians. Most low–income Californians receive little or no assistance. Expanding affordable housing programs to help these households likely would be extremely challenging and prohibitively expensive. It may be best to focus these programs on Californians with more specialized housing needs—such as homeless individuals and families or persons with significant physical and mental health challenges.

Encouraging additional private housing construction can help the many low–income Californians who do not receive assistance. Considerable evidence suggests that construction of market–rate housing reduces housing costs for low–income households and, consequently, helps to mitigate displacement in many cases. Bringing about more private home building, however, would be no easy task, requiring state and local policy makers to confront very challenging issues and taking many years to come to fruition. Despite these difficulties, these efforts could provide significant widespread benefits: lower housing costs for millions of Californians.

Various Government Programs Help Californians Afford Housing

Federal, state, and local governments implement a variety of programs aimed at helping Californians, particularly low–income Californians, afford housing. These programs generally work in one of three ways: (1) increasing the supply of moderately priced housing, (2) paying a portion of households’ rent costs, or (3) limiting the prices and rents property owners may charge for housing.

Various Programs Build New Moderately Priced Housing. Federal, state, and local governments provide direct financial assistance—typically tax credits, grants, or low–cost loans—to housing developers for the construction of rental housing. In exchange, developers reserve these units for lower–income households. (Until recently, local redevelopment agencies also provided this type of financial assistance.) By far the largest of these programs is the federal and state Low Income Housing Tax Credit (LIHTC), which provides tax credits to affordable housing developers to cover a portion of their building costs. The LIHTC subsidizes the new construction of around 7,000 rental units annually in the state—typically less than 10 percent of total public and private housing construction. This represents a significant majority of the affordable housing units constructed in California each year.

Vouchers Help Households Afford Housing. The federal government also makes payments to landlords—known as housing vouchers—on behalf of about 400,000 low–income households in California. These payments generally cover the portion of a rental unit’s monthly cost that exceeds 30 percent of the household’s income.

Some Local Governments Place Limits on Prices and Rents. Some local governments have policies that require property owners charge below–market prices and rents. In some cases, local governments limit how much landlords can increase rents each year for existing tenants. About 15 California cities have these rent controls, including Los Angeles, San Francisco, San Jose, and Oakland. In 1995, the state enacted Chapter 331 of 1995 (AB 1164, Hawkins), which prevented rent control for properties built after 1995 or properties built prior to 1995 that had not previously been subject to rent control. Assembly Bill 1164 also allowed landlords to reset rents to market rates when properties transferred from one tenant to another. In other cases, local governments require developers of market–rate housing to charge below–market prices and rents for a portion of the units they build, a policy called “inclusionary housing.”

Need For Housing Assistance Outstrips Resources

Many Low–Income Households Receive No Assistance. The number of low–income Californians in need of assistance far exceeds the resources of existing federal, state, and local affordable housing programs. Currently, about 3.3 million low–income households (who earn 80 percent or less of the median income where they live) rent housing in California, including 2.3 million very–low–income households (who earn 50 percent or less of the median income where they live). Around one–quarter (roughly 800,000) of low–income households live in subsidized affordable housing or receive housing vouchers. Most households receive no help from these programs. Those that do often find that it takes several years to get assistance. Roughly 700,000 households occupy waiting lists for housing vouchers, almost twice the number of vouchers available.

Majority of Low–Income Households Spend More Than Half of Their Income on Housing. Around 1.7 million low–income renter households in California report spending more than half of their income on housing. This is about 14 percent of all California households, a considerably higher proportion than in the rest of the country (about 8 percent).

Challenges of Expanding Existing Programs

One possible response to these affordability challenges could be to expand existing housing programs. Given the number of households struggling with high housing costs, however, this approach would require a dramatic expansion of existing government programs, necessitating funding increases orders of magnitude larger than existing program funding and far–reaching changes in existing regulations. Such a dramatic change would face several challenges and probably would have unintended consequences. Ultimately, attempting to address the state’s housing affordability challenges primarily through expansion of government programs likely would be impractical. This, however, does not preclude these programs from playing a role in a broader strategy to improve California’s housing affordability. Below, we discuss these issues in more detail.

Expanding Assistance Programs Would Be Very Expensive

Extending housing assistance to low–income Californians who currently do not receive it—either through subsidies for affordable units or housing vouchers—would require an annual funding commitment in the low tens of billions of dollars. This is roughly the magnitude of the state’s largest General Fund expenditure outside of education (Medi–Cal).

Affordable Housing Construction Requires Large Public Subsidies. While it is difficult to estimate precisely how many units of affordable housing are needed, a reasonable starting point is the state’s current population of low–income renter households that spend more than half of their income on housing—about 1.7 million households. Based on data from the LIHTC, housing built for low–income households in California’s coastal urban areas requires a public subsidy of around $165,000 per unit. At this cost, building affordable housing for California’s 1.7 million rent burdened low–income households would cost in excess of $250 billion. This cost could be spread out over several years (by issuing bonds or providing subsidies to builders in installments), requiring annual expenditures in the range of $15 billion to $30 billion. There is a good chance the actual cost could be higher. Affordable housing projects often receive subsidies from more than one source, meaning the public subsidy cost per unit likely is higher than $165,000. It is also possible the number of units needed could be higher if efforts to make California’s housing more affordable spurred more people to move to the state. Conversely, there is some chance the cost could be lower if building some portion of the 1.7 million eased competition at the bottom end of the housing market and allowed some low–income families to find affordable market–rate housing. Nonetheless, under any circumstances it is likely this approach would require ongoing annual funding at least in the low tens of billions of dollars.

Expanding Housing Vouchers Also Would Be Expensive. Housing vouchers would be similarly expensive. According to American Community Survey data, around 2.5 million low–income households in California spend more than 30 percent of their income on rent. These households’ rents exceed 30 percent of their incomes by $625 each month on average, meaning they would require an annual subsidy of around $7,500. This suggests that providing housing vouchers to all of these households would cost around $20 billion annually. By similar logic, a less generous program that covered rent costs exceeding 50 percent of household income would cost around $10 billion annually. There is, however, good reason to believe the cost of expanding voucher programs would be significantly higher than these simple estimates suggest. As we discuss in the next section, a major increase in the number of voucher recipients likely would cause rents to rise. Higher rent costs, in turn, would increase the amount government would need to pay on behalf of low–income renters. This effect is difficult to quantify but probably would add several billion to tens of billions of dollars to the annual cost of a major expansion of vouchers.

Existing Housing Shortage Poses Problems for Some Programs

Many housing programs—vouchers, rent control, and inclusionary housing—attempt to make housing more affordable without increasing the overall supply of housing. This approach does very little to address the underlying cause of California’s high housing costs: a housing shortage. Any approach that does not address the state’s housing shortage faces the following problems.

Housing Shortage Has Downsides Not Addressed by Existing Housing Programs. High housing costs are not the only downside of the state’s housing shortage. As we discussed in detail in California’s High Housing Costs, California’s housing shortage denies many households the opportunity to live in the state and contribute to the state’s economy. This, in turn, reduces the state’s economic productivity. The state’s housing shortage also makes many Californians—not only low–income residents—more likely to commute longer distances, live in overcrowded housing, and delay or forgo homeownership. Housing programs such as vouchers, rent control, and inclusionary housing that do not add to the state’s housing stock do little to address these issues.

Scarcity of Housing Undermines Housing Vouchers. California’s tight housing markets pose several challenges for housing voucher programs which can limit their effectiveness. In competitive housing markets, landlords often are reluctant to rent to housing voucher recipients. Landlords may not be interested in navigating program requirements or may perceive voucher recipients to be less reliable tenants. One nationwide study conducted in 2001 found that only two–thirds of voucher recipients in competitive housing markets were able to secure housing. This issue likely would be amplified if the number of voucher recipients competing for housing were increased significantly. In addition, some research suggests that expanding housing vouchers in competitive housing markets results in rent increases, which either offset benefits to voucher holders or increase government costs for the program. One study looking at an unusually large increase in the federal allotment of housing vouchers in the early 2000s found that each 10 percent increase in vouchers in tight housing markets increased monthly rents by an average of $18 (about 2 percent). This suggests that extending vouchers to all of California’s low–income households (a several hundred percent increase in the supply of vouchers) could lead to substantial rent inflation. If this were to occur, the estimates in the prior section of the cost to expand vouchers to all low–income households would be significantly higher.

Housing Costs for Households Not Receiving Assistance Could Rise. Expansion of voucher programs also could aggravate housing challenges for those who do not receive assistance, particularly if assistance is extended to some, but not all low–income households. As discussed above, research suggests that housing vouchers result in rent inflation. This rent inflation not only effects voucher recipients but potentially increases rents paid by other low– and lower–middle income households that do not receive assistance.

Housing Shortage Also Creates Problems for Rent Control Policies. The state’s shortage of housing also presents challenges for expanding rent control policies. Proposals to expand rent control often focus on two broad changes: (1) expanding the number of housing units covered—by applying controls to newer properties or enacting controls in locations that currently lack them—and (2) prohibiting landlords from resetting rents to market rates for new tenants. Neither of these changes would increase the supply of housing and, in fact, likely would discourage new construction. Households looking to move to California or within California would therefore continue to face stiff competition for limited housing, making it difficult for them to secure housing that they can afford. Requiring landlords to charge new tenants below–market rents would not eliminate this competition. Households would have to compete based on factors other than how much they are willing to pay. Landlords might decide between tenants based on their income, creditworthiness, or socioeconomic status, likely to the benefit of more affluent renters.

Barriers to Private Development Also Hinder Affordable Housing Programs

Local Resistance and Environmental Protection Policies Constrain Housing Development. Local community resistance and California Environmental Quality Act (CEQA) challenges limit the amount of housing—both private and subsidized—built in California. These factors present challenges for subsidized construction and inclusionary housing programs. Subsidized housing construction faces the same, in many cases more, community opposition as market–rate housing because it often is perceived as bringing negative changes to a community’s quality or character. Furthermore, subsidized construction, like other housing developments, often must undergo the state’s environmental review process outlined in CEQA. This can add costs and delay to these projects. Inclusionary housing programs rely on private housing development to fund construction of affordable housing. Because of this, barriers that constrain private housing development also limit the amount of affordable housing produced by inclusionary housing programs.

Home Builders Often Forced to Compete for Limited Development Opportunities. With state and local policies limiting the number of housing projects that are permitted, home builders often compete for limited opportunities. One result of this is that subsidized construction often substitutes for—or “crowds out”—market–rate development. Several studies have documented this crowd–out effect, generally finding that the construction of one subsidized housing unit reduces market–rate construction by one–half to one housing unit. These crowd–out effects can diminish the extent to which subsidized housing construction increases the state’s overall supply of housing.

Other Unintended Consequences

“Lock–In” Effect. Households residing in affordable housing (built via subsidized construction or inclusionary housing) or rent–controlled housing typically pay rents well below market rates. Because of this, households may be discouraged from moving from their existing unit to market–rate housing even when it may otherwise benefit them—for example, if the market–rate housing would be closer to a new job. This lock–in effect can cause households to stay longer in a particular location than is otherwise optimal for them.

Declining Quality of Housing. By depressing rents, rent control policies reduce the income received by owners of rental housing. In response, property owners may attempt to cut back their operating costs by forgoing maintenance and repairs. Over time, this can result in a decline in the overall quality of a community’s housing stock.

More Private Home Building Could Help

Most low–income Californians receive little or no assistance from existing affordable housing programs. Given the challenges of significantly expanding affordable housing programs, this is likely to persist for the foreseeable future. Many low–income households will continue to struggle to find housing that they can afford. Encouraging more private housing development seems like a reasonable approach to help these households. But would it actually help? In this section, we present evidence that construction of new, market–rate housing can lower housing costs for low–income households.

Increased Supply, Lower Costs

Lack of Supply Drives High Housing Costs. As we demonstrate in California’s High Housing Costs, a shortage of housing results in high and rising housing costs. When the number of households seeking housing exceeds the number of units available, households must try to outbid each other, driving up prices and rents. Increasing the supply of housing can help alleviate this competition and, in turn, place downward pressure on housing costs.

Building New Housing Indirectly Adds to the Supply of Housing at the Lower End of the Market. New market–rate housing typically is targeted at higher–income households. This seems to suggest that construction of new market–rate housing does not add to the supply of lower–end housing. Building new market–rate housing, however, indirectly increases the supply of housing available to low–income households in multiple ways.

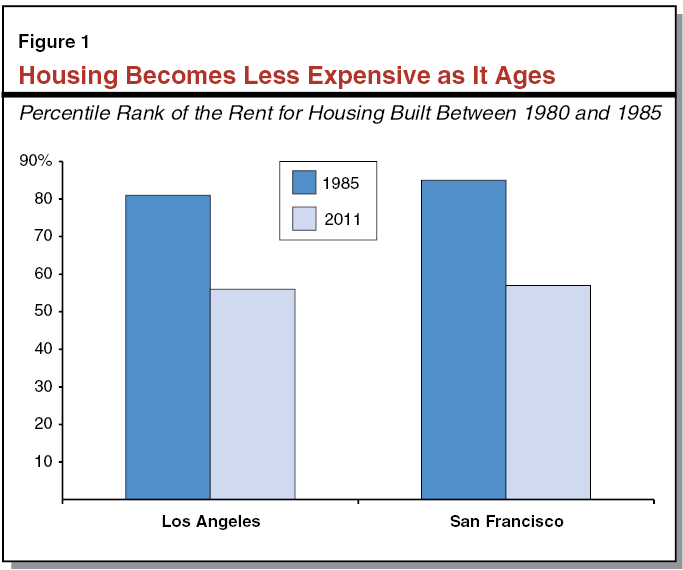

Housing Becomes Less Desirable as It Ages . . . New housing generally becomes less desirable as it ages and, as a result, becomes less expensive over time. Market–rate housing constructed now will therefore add to a community’s stock of lower–cost housing in the future as these new homes age and become more affordable. Our analysis of American Housing Survey data finds evidence that housing becomes less expensive as it ages. Figure 1 shows the average rent for housing built between 1980 and 1985 in Los Angeles and San Francisco. These housing units were relatively expensive in 1985 (rents in the top fifth of all rental units) but were considerably more affordable by 2011 (rents near the median of all rental units). Housing that likely was considered “luxury” when first built declined to the middle of the housing market within 25 years.

. . . But Lack of New Construction Can Slow This Process. When new construction is abundant, middle–income households looking to upgrade the quality of their housing often move from older, more affordable housing to new housing. As these middle–income households move out of older housing it becomes available for lower–income households. This is less likely to occur in communities where new housing construction is limited. Faced with heightened competition for scarce housing, middle–income households may live longer in aging housing. Instead of upgrading by moving to a new home, owners of aging homes may choose to remodel their existing homes. Similarly, landlords of aging rental housing may elect to update their properties so that they can continue to market them to middle–income households. As a result, less housing transitions to the lower–end of the housing market over time. One study of housing costs in the U.S. found that rental housing generally depreciated by about 2.5 percent per year between 1985 and 2011, but that this rate was considerably lower (1.8 percent per year) in regions with relatively limited housing supply.

New Housing Construction Eases Competition Between Middle– and Low–Income Households. Another result of too little housing construction is that more affluent households, faced with limited housing choices, may choose to live in neighborhoods and housing units that historically have been occupied by low–income households. This reduces the amount of housing available for low–income households. Various economic studies have documented this result. One analysis of American Housing Survey data by researchers at the Federal Reserve Bank of New York found that “the more constrained the supply response for new residential units to demand shocks, the greater the probability that an affordable unit will filter up and out of the affordable stock.” Other researchers have found that low–income neighborhoods are more likely to experience an influx of higher–income households when they are in close proximity to affluent neighborhoods with tight housing markets.

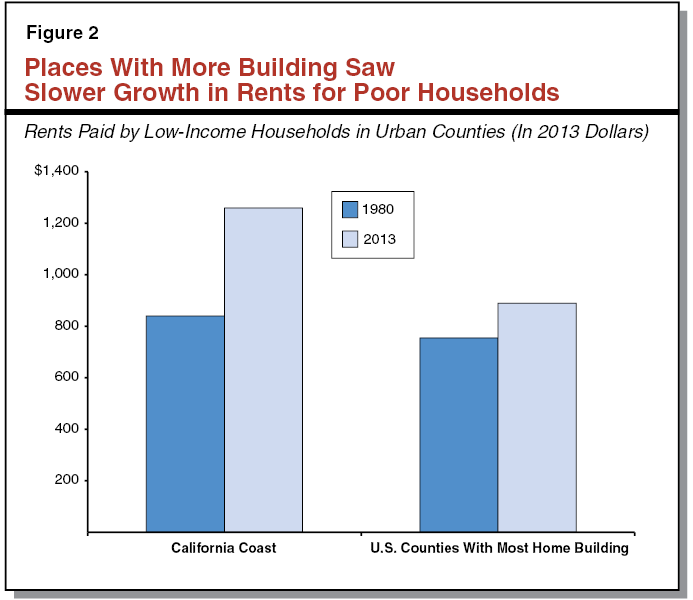

More Supply Places Downward Pressure on Prices and Rents. When the number of housing units available at the lower end of a community’s housing market increases, growth in prices and rents slows. Evidence supporting this relationship can be found by comparing housing expenditures of low–income households living in California’s slow–growing coastal communities to those living in fast–growing communities elsewhere in the country. Between 1980 and 2013, the housing stock in California’s coastal urban counties (counties comprising metropolitan areas with populations greater than 500,000) grew by only 34 percent, compared to 99 percent in the fastest growing urban counties throughout the country (top fifth of all urban counties). As figure 2 shows, over the same time period rents paid by low–income households grew nearly three times faster in California’s coastal urban counties than in the fastest growing urban counties (50 percent compared to 18 percent). As a result, the typical low–income household in California’s costal urban counties now spends around 54 percent of their income on housing, compared to only 43 percent in fast growing counties. This difference—11 percentage points—is roughly equal to a typical low–income household’s total spending on transportation.

Lower Costs Reduce Chances of Displacement

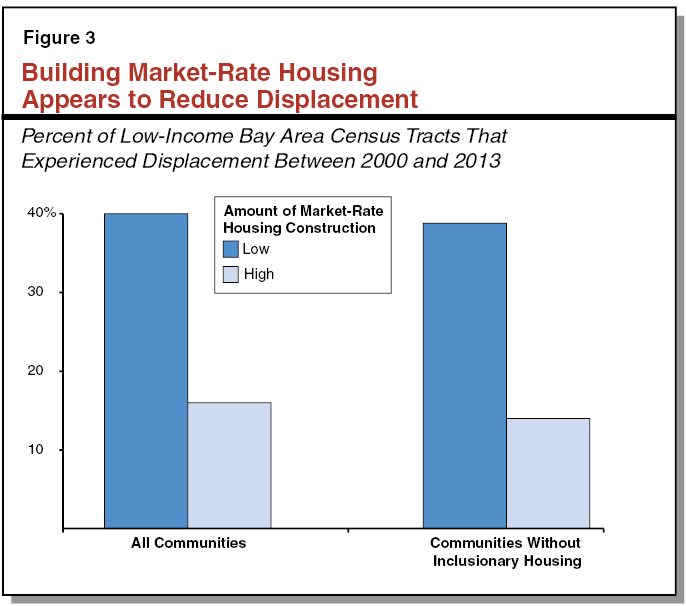

More Private Development Associated With Less Displacement. As market–rate housing construction tends to slow the growth in prices and rents, it can make it easier for low–income households to afford their existing homes. This can help to lessen the displacement of low–income households. Our analysis of low–income neighborhoods in the Bay Area suggests a link between increased construction of market–rate housing and reduced displacement. (See the technical appendix for more information on how we defined displacement for this analysis.) Between 2000 and 2013, low–income census tracts (tracts with an above–average concentration of low–income households) in the Bay Area that built the most market–rate housing experienced considerably less displacement. As Figure 3 shows, displacement was more than twice as likely in low–income census tracts with little market–rate housing construction (bottom fifth of all tracts) than in low–income census tracts with high construction levels (top fifth of all tracts).

Results Do Not Appear to Be Driven by Inclusionary Housing Policies. One possible explanation for this finding could be that many Bay Area communities have inclusionary housing policies. In communities with inclusionary housing policies, most new market–rate construction is paired with construction of new affordable housing. It is possible that the new affordable housing units associated with increased market–rate development—and not market–rate development itself—could be mitigating displacement. Our analysis, however, finds that market–rate housing construction appears to be associated with less displacement regardless of a community’s inclusionary housing policies. As with other Bay Area communities, in communities without inclusionary housing policies, displacement was more than twice as likely in low–income census tracts with limited market–rate housing construction than in low–income census tracts with high construction levels.

Relationship Remains After Accounting for Economic and Demographic Factors. Other factors play a role in determining which neighborhoods experience displacement. A neighborhood’s demographics and housing characteristics probably are important. Nonetheless, we continue to find that increased market–rate housing construction is linked to reduced displacement after using common statistical techniques to account for these factors. (See the technical appendix for more details.)

Conclusion

Addressing California’s housing crisis is one of the most difficult challenges facing the state’s policy makers. The scope of the problem is massive. Millions of Californians struggle to find housing that is both affordable and suits their needs. The crisis also is a long time in the making, the culmination of decades of shortfalls in housing construction. And just as the crisis has taken decades to develop, it will take many years or decades to correct. There are no quick and easy fixes.

The current response to the state’s housing crisis often has centered on how to improve affordable housing programs. The enormity of California’s housing challenges, however, suggests that policy makers look for solutions beyond these programs. While affordable housing programs are vitally important to the households they assist, these programs help only a small fraction of the Californians that are struggling to cope with the state’s high housing costs. The majority of low–income households receive little or no assistance and spend more than half of their income on housing. Practically speaking, expanding affordable housing programs to serve these households would be extremely challenging and prohibitively expensive.

In our view, encouraging more private housing development can provide some relief to low–income households that are unable to secure assistance. While the role of affordable housing programs in helping California’s most disadvantaged residents remains important, we suggest policy makers primarily focus on expanding efforts to encourage private housing development. Doing so will require policy makers to revisit long–standing state policies on local governance and environmental protection, as well as local planning and land use regimes. The changes needed to bring about significant increases in housing construction undoubtedly will be difficult and will take many years to come to fruition. Policy makers should nonetheless consider these efforts worthwhile. In time, such an approach offers the greatest potential benefits to the most Californians.

References

Early, D. W. (2000). Rent Control, Rental Housing Supply, and the Distribution of Tenant Benefits. Journal of Urban Economics, 48(2), 185–204.

Eriksen, M. D., & Rosenthal, S. S. (2010). Crowd out effects of place–based subsidized rental housing: New evidence from the LIHTC program. Journal of Public Economics, 94(11), 953–966.

Eriksen, M. D., & Ross, A. (2014). Housing Vouchers and the Price of Rental Housing. American Economic Journal: Economic Policy.

Finkel, M., & Buron, L. (2001). Study on Section 8 Voucher Success Rates. Volume I. Quantitative Study of Success Rates in Metropolitan Areas. Prepared by Abt Associates for the U.S. Department of Housing and Urban Development, 2–3.

Glaeser, E. L., & Luttmer, E. F. (2003). The Misallocation of Housing Under Rent Control. The American Economic Review, 93(4).

Guerrieri, V., Hartley, D., & Hurst, E. (2013). Endogenous Gentrification and Housing Price Dynamics. Journal of Public Economics, Volume 100 (C), 45–60.

Gyourko, J., & Linneman, P. (1990). Rent Controls and Rental Housing Quality: A Note on the Effects of New York City’s Old Controls. Journal of Urban Economics, 27(3), 398–409.

Malpezzi, S., & Vandell, K. (2002). Does the low–income housing tax credit increase the supply of housing? Journal of Housing Economics, 11(4), 360–380.

Munch, J. R., & Svarer, M. (2002). Rent control and tenancy duration. Journal of Urban Economics, 52(3), 542–560.

Rosenthal, S. S. (2014). Are Private Markets and Filtering a Viable Source of Low–Income Housing? Estimates from a “Repeat Income” Model. The American Economic Review, 104(2), 687–706.

Sims, D. P. (2007). Out of control: What can we learn from the end of Massachusetts rent control? Journal of Urban Economics, 61(1), 129–151.

Sinai, T., & Waldfogel, J. (2005). Do low–income housing subsidies increase the occupied housing stock? Journal of Public Economics, 89(11), 2137–2164.

Somerville, C. T., & Mayer, C. J. (2003). Government Regulation and Changes in the Affordable Housing Stock. Economic Policy Review, 9(2), 45–62.

Susin, S. (2002). Rent vouchers and the price of low–income housing. Journal of Public Economics, 83(1), 109–152.

Technical Appendix

To examine the relationship between market–rate housing construction and displacement of low–income households we developed a simple econometric model to estimate the probability of a low–income Bay Area neighborhood experiencing displacement.

Data. We use data (.xlsx) on Bay Area census tracts (small subdivisions of a county typically containing around 4,000 people) maintained by researchers with the University of California (UC) Berkeley Urban Displacement Project. This dataset included information on census tract demographics, housing characteristics, and housing construction levels. We focus on data for the period 2000 to 2013.

Defining Displacement. Researchers have not developed a single definition of displacement. Different studies use different measures. For our analysis, we use a straightforward yet imperfect definition of displacement which is similar to the definition used by UC Berkeley researchers. Specifically, we define a census tract as having experienced displacement if (1) its overall population increased and its population of low–income households decreased or (2) its overall population decreased and its low–income population declined faster than the overall population.

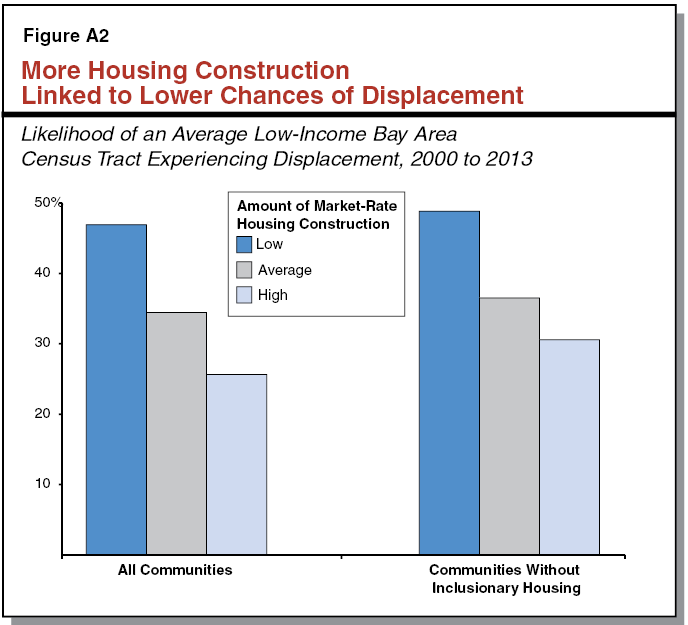

Our Model. We use probit regression analysis to evaluate how various factors affected the likelihood of a census tract experiencing displacement between 2000 and 2013. This type of model allows us to hold constant various economic and demographic factors and isolate the impact of increased market–rate construction on the likelihood of displacement. The results of our regression are show in Figure A1. Coefficient estimates from probit regressions are not easily interpreted. While the fact that the coefficient for market–rate housing construction is statistically significant and negative suggests that more construction reduces the likelihood of displacement, the magnitude of this effect is not immediately clear. To better understand these results, we used the model to compare the probability that an average census tract would experience displacement when its market–rate construction was low (0 units), average (136 units), and high (243 units). As shown in Figure A2, with low construction levels, a census tract’s probability of experiencing displacement was 47 percent, compared to 34 percent with average construction levels, and 26 percent with high construction levels.

Figure A1

Regression Results

Dependent Variable: Did Displacement Occur (Yes=1 and No=0)?

|

Independent Variable |

Coefficient |

Standard Error |

|

Number of market–rate housing units built |

–0.00237 |

0.00043 |

|

Share of population that is low income |

1.74075 |

0.54137 |

|

Share of population that is nonwhite |

–0.61213 |

0.29151 |

|

Share of adults over 25 with a college degree |

1.90054 |

0.38599 |

|

Population density |

–0.00001 |

0.00000 |

|

Share of housing built before 1950 |

1.16506 |

0.22569 |

|

Constant |

–1.45886 |

0.33420 |