Despite improving revenues, California policymakers continued to face significant fiscal challenges in preparing the 2005-06 budget. Although the projected budget shortfall for 2005-06 was considerably smaller than in the three prior years, the state’s ongoing structural budget problem remained a major concern. In this chapter, we (1) briefly review the factors behind the state’s ongoing budget shortfall, (2) highlight the major budget solutions included in the 2005-06 budget package, and (3) provide preliminary estimates of how the actions adopted in the 2005-06 budget will affect the fiscal outlook for 2006-07 and beyond.

California has faced large structural budget shortfalls-that is, persistent operating deficits where annual expenditures have exceeded revenues-since 2001-02, when revenues plunged following the recession and the steep decline in the stock market. Although revenues subsequently improved and some progress was made toward addressing the structural shortfall in the 2002-03 through 2004-05 budgets, policymakers were not able to agree on a sufficient amount of ongoing solutions to eliminate the structural problem. Instead, the 2002-03 through 2004-05 budgets relied heavily on one-time or limited-term solutions-such as borrowing, spending deferrals, and funding shifts-to achieve temporary balance. In addition to providing only temporary savings, many of these solutions resulted in additional future expenditures, as deferred spending and loan repayments come due. At the beginning of the current budget cycle, the state faced repayments on budget-related debt totaling $2 billion in 2005-06 and about $4 billion annually over the period 2006-07 through 2008-09.

Size of Budget Problem. In our November 2004 fiscal forecast, we estimated that the state faced a year-end shortfall in its 2005-06 General Fund budget of nearly $6.7 billion. We also estimated an operating deficit of around $7.3 billion in 2005-06, increasing to $10 billion in 2006-07 as various temporary savings expire and deferred obligations start coming due. In its January 2005 budget proposal, the administration identified an even-larger $8.6 billion projected year-end shortfall in 2005-06. These projected shortfalls declined in the subsequent months due to stronger-than-expected revenues realized in the spring of 2005 (related to both improved economic activity and large amnesty-related tax collections). As a result, by the time the budget was adopted, the projected year-end 2005-06 shortfall had narrowed to around $3.4 billion, and the ongoing structural shortfall in 2006-07 had dropped to slightly under $9 billion.

The 2005-06 budget package contains about $5.9 billion in solutions. These solutions are expected to eliminate the $3.4 billion budget shortfall and establish a $1.3 billion year-end reserve, while at the same time enabling the state to prepay the $1.2 billion vehicle license fee (VLF) “gap loan” from local governments (due in 2006-07). As shown in Figure 1, the solutions fall into four major categories-namely, program savings, fund shifts, loans and borrowing, and revenues from improved tax compliance.

|

Figure 1 Solutions in 2005‑06 Budget |

|

|

(In Millions) |

|

|

|

|

|

Program Savings |

|

|

Proposition 98a |

$2,994 |

|

Social services |

455 |

|

State operations |

100 |

|

Property tax administration |

60 |

|

Employee compensation |

40 |

|

Other |

496 |

|

Subtotal, Program Savings |

($4,145) |

|

Funding Shifts |

|

|

Retain Public Transportation Account spillover |

$380 |

|

Federal funds for certain prenatal care |

192 |

|

Tideland oil revenues |

157 |

|

Subtotal, Funding Shifts |

($728) |

|

Loans and Borrowing |

|

|

Refinance tobacco bonds |

$525 |

|

Loan from Merrill Lynch for Paterno lawsuit settlementb |

361 |

|

Subtotal, Loans and Borrowing |

($886) |

|

Revenues |

|

|

Increased tax compliance |

$94 |

|

Total |

$5,853 |

|

|

|

|

Detail may not total due to rounding. |

|

|

a Consists of $1.823 billion in savings in 2004‑05 and $1.171 billion in savings in 2005‑06. |

|

|

b This amount is net of 2005‑06 General Fund repayments on the $428 million loan. |

|

Program Savings. About $4.1 billion of the solutions involve program savings. Nearly three-quarters of this total is from holding Proposition 98 funding for 2004-05 at the level provided in the 2004-05 budget, instead of providing additional funding to reflect revenue improvements since the budget’s enactment. Another $455 million is in social services, mostly related to the suspension of cost-of-living adjustments for California Work Opportunity and Responsibility to Kids and Supplemental Security Income/State Supplementary Program grants. The balance of the savings is from a variety of areas, including state operations, local property tax administration, and employee compensation.

Funding Shifts. About $728 million in General Fund savings are from funding shifts. These include $380 million from retaining certain sales taxes on gasoline (so-called “spillover funds”) in the General Fund instead of using them for public transit purposes. Other funding redirections include a shift of tideland oil revenues from special funds to the General Fund, and the use of federal funds instead of General Fund for certain prenatal care provided under the Medi-Cal Program.

Loans and Borrowing. Although the budget does not use additional deficit-financing bonds beyond those that already have been issued, it does include budget-related borrowing from two sources. First, it relies on a $428 million loan from Merrill Lynch to finance the settlement costs of flood-related litigation (the Paterno case) against the state. The first repayment of this loan occurs in 2005-06, resulting in net General Fund savings of $361 million from the loan. Second, the budget assumes the refinancing of previously issued tobacco settlement-backed bonds, raising $525 million.

Revenues. Although the budget does not include any new General Fund taxes, it does anticipate additional revenues of $94 million related to increased tax compliance efforts.

The 2005-06 budget contains roughly $2 billion in ongoing budgetary savings. We estimate that these savings, coupled with the prepayment of the VLF gap loan, will reduce the projected 2006-07 operating shortfall between annual current law revenues and expenditures by roughly one-third-from around $9 billion to around $6 billion.

We will be updating our projections for 2005-06 and future years to reflect actions taken in the final month of the legislative session, as well as expenditure and revenue-related developments, in our annual publication entitled California’s Fiscal Outlook, scheduled to be released in November 2005.

The state spending plan for 2005-06 includes total budget expenditures of $113 billion. This includes $90 billion from the General Fund and $23 billion from special funds. As Figure 1 shows, the combined spending total from these funds is up $9.3 billion (9 percent) from 2004-05.

|

Figure 1 The 2005-06 Budget

Package |

|||||

|

(Dollars in Millions) |

|||||

|

|

|

|

|

Change From 2004-05 |

|

|

Fund Type |

Actual |

Estimated |

Enacted |

Amount |

Percent |

|

General Fund |

$76,333 |

$81,728 |

$90,026 |

$8,298 |

10.2% |

|

Special funds |

18,892 |

22,286 |

23,333 |

1,047 |

4.7 |

|

Budget Totals |

$95,225 |

$104,014 |

$113,359 |

$9,345 |

9.0% |

|

Selected bond funds |

6,986 |

14,607 |

4,004 |

-10,603 |

-72.6 |

|

Totals |

$102,211 |

$118,621 |

$117,363 |

-$1,258 |

-1.1% |

The figure also shows that spending of bond proceeds jumped from $7 billion in 2003-04 to $14.6 billion in 2004-05, before falling back to $4 billion in 2005-06. Bond-fund expenditures reflect the use of bond proceeds on capital outlay projects in a given year (or, in the case of education bonds, the allocation of the bond authority to specific local projects by the State Allocation Board). The costs associated with debt service on the bonds are included in the General Fund and special funds spending totals. The one-time jump in bond spending in 2004-05 largely reflects the allocation of K-12 education bonds (approved by voters in 2004) to specific projects.

The General Fund Condition

Figure 2 summarizes the estimated General Fund condition for 2004-05 and 2005-06 that results from the adopted spending plan.

|

Figure 2 The 2005‑06 Budget

Package |

|||

|

(Dollars in Millions) |

|||

|

|

2004‑05 |

2005‑06 |

Percent |

|

Prior-year fund balance |

$7,279 |

$7,498 |

— |

|

Revenues and transfers |

79,935 |

84,471 |

5.7% |

|

Deficit-financing bond |

2,012 |

— |

— |

|

Total resources available |

$89,226 |

$91,969 |

— |

|

Expenditures |

$81,728 |

$90,026 |

10.2% |

|

Ending fund balance |

$7,498 |

$1,943 |

— |

|

Encumbrances |

641 |

641 |

— |

|

Reserve |

$6,857 |

$1,302 |

|

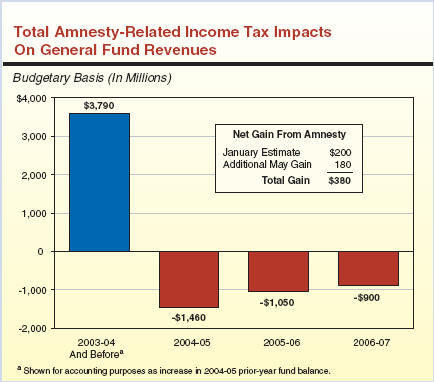

2004-05. The figure shows that 2004-05 began with a prior-year balance of $7.3 billion. This large balance was boosted by a net of $3.8 billion in receipts directly and indirectly related to the tax amnesty program adopted in conjunction with the 2004-05 budget (see box below). These payments were received in the spring of 2005, but since they were related to tax liabilities in 2002 and prior years, they were accrued back to the earlier years and reflected as an increase to the 2004-05 carry-in balance. All but $380 million of the $3.8 billion increase is expected to be offset by lower collections related to audits during the 2004-05 through 2006-07 period. A more complete discussion of the fiscal impacts of the amnesty program is included in the box.

Amnesty-Related RevenuesOne of the key developments during the spring of 2005 was the unexpectedly large amount of cash receipts that resulted directly and indirectly from a tax amnesty program that had been adopted as part of the previous year’s budget. The amnesty filing time frame ran from February 1, 2005 to March 31, 2005, and applied to tax years before 2003. When the program was enacted in 2004-05 it was expected to result in $600 million in cash payments from personal income and corporate taxpayers. Of this total, $200 million was expected to be new revenues and the remainder was expected to represent an acceleration of payments what would otherwise have been received through the state’s ongoing audit process. The actual amount of cash payments received by the Franchise Tax Board dramatically exceeded the original estimates. Total amnesty-related receipts were around $4.4 billion. Of this total, over $800 million was filed by amnesty participants, and another $3.6 billion was largely from nonamnesty participants who filed so-called “protective claims” to avoid the possibility of being charged high post-amnesty penalties if their tax challenges are not upheld or if they receive future audit assessments. The great majority of these new payments are expected to be offset by lower net collections in the future. Specifically, the 2005-06 budget is based on the assumption that, of the $4.4 billion in total amnesty-related collections, about $4 billion either represents an acceleration of future tax payments that have already been projected, or amounts that will have to be refunded in the future because they will exceed what taxpayers owe. These cash offsets are estimated to total roughly $600 million in 2004-05, $1.5 billion in 2005-06, $1.1 billion in 2006-07, and $900 million in 2007-08. Taking into account both the cash payments and the expected offsets, the net gain from the amnesty program is expected to be $380 million, or $180 million more than originally anticipated when the 2004-05 budget was enacted. Budgetary Impacts. California uses an accrual method of accounting for state revenues. In theory, under an accrual system, all of the $4.4 billion in payments should be attributed back to the individual tax years before 2003 to which they apply. However, under California’s method of accounting, the state does not go back and change revenue totals for past years that have been “closed” for accounting purposes. Rather, it shows such amounts as an adjustment to the prior-year’s incoming balance. With regard to expected changes in future payments or refunds associated with the amnesty program, the state’s accounting methodology recognizes revenue that is expected to be received within 12 months. Taking into account these factors, the budgetary impact of the amnesty program is shown in the accompanying figure. It shows that the net impact on budgetary revenues is:

|

The figure also shows that revenues totaled $79.9 billion, or about $1.8 billion less than the $81.7 billion in expenditures, during the year. In addition, the state used $2 billion of deficit-financing bond proceeds. (To date, the state has sold $11.3 billion of the $15 billion in deficit bonds authorized by California voters in March 2004.) After accounting for $641 million in encumbrances (that is, contracts and other spending commitments made in 2004-05 which will be liquidated in 2005-06), the year closed with a reserve of $6.9 billion.

2005-06. Figure 2 shows that revenues are projected to increase by 5.7 percent in 2005-06, to $84.5 billion, while expenditures are projected to increase by 10 percent, to $90 billion during the year. This results in an operating deficit of $5.6 billion. This, in turn, lowers the projected 2005-06 year-end reserve to $1.3 billion.

Programmatic Spending in 2005-06

Figure 3 shows General Fund spending by major program area for the 2003-04 through 2005-06 period. It shows that K-12 spending is the single largest area, accounting for nearly 40 percent of the General Fund total. Higher education, health, social services, and criminal justice spending account for most of the balance of all spending.

|

|

Figure 3 The 2005‑06 Budget

Package |

||||||

|

|

(Dollars in Millions) |

||||||

|

|

|

|

|

|

Change From 2004‑05 |

||

|

|

|

Actual |

Estimated |

Enacted |

Amount |

Percent |

|

|

|

K-12 Educationb |

$29,197 |

$32,527 |

$34,987 |

$2,460 |

7.6% |

|

|

|

Higher Education |

8,789 |

9,302 |

10,185 |

882 |

9.5 |

|

|

|

Health |

13,911 |

16,024 |

17,861 |

1,836 |

11.5 |

|

|

|

Social Services |

8,851 |

8,973 |

9,254 |

281 |

3.1 |

|

|

|

Criminal Justice |

7,333 |

9,161 |

9,663 |

502 |

5.5 |

|

|

|

Transportation |

482 |

352 |

1,673 |

1,321 |

375.6 |

|

|

|

Vehicle license fee (VLF) subventionsc |

3,125 |

— |

1,186 |

— |

— |

|

|

|

All other |

4,645 |

5,388 |

5,144 |

-245 |

-4.5 |

|

|

|

Totals |

$76,333 |

$81,728 |

$90,026 |

$8,298 |

10.2% |

|

|

|

|

||||||

|

a General obligation bond and lease-revenue bond debt service is allocated by program area. |

|

||||||

|

b Includes both Proposition 98 and non-Proposition 98 funding. |

|

||||||

|

c 2005‑06 amount reflects repayment of VLF “gap loan” covering subventions not paid in 2002‑03 and 2003‑04. |

|

||||||

The figure shows that, despite the savings actions adopted in the budget (and discussed in “Chapter 1”), expenditures are still projected to increase by over 10 percent in 2005-06-about double the rate of population growth and inflation in the state. As discussed below, this large increase reflects both

(1) ongoing growth in key state programs and (2) a variety of special factors.

Ongoing Program Growth. We estimate that roughly one-half of the total General Fund spending growth is the result of significant spending increases for a variety of state programs. For example, the budget increases per-pupil funding for both K-12 and community college education. It also funds the Governor’s compact for University of California (UC) and California State University (CSU), and provides a 6 percent general cost-of-living adjustment (COLA) for trial courts. The budget also reflects increased costs and utilization in the state’s ongoing Medi-Cal and related health care programs.

Special Factors. The other half of the spending increase is related to such factors as restorations in spending that had been deferred or suspended in 2004-05, and the payment of obligations incurred in prior years. These factors include:

Proposition 42 Transfer. This transfer of sales taxes on gasoline to transportation special funds was deferred in 2003-04 and 2004-05 but is fully funded in 2005-06. This results in an added cost to the General Fund of $1.3 billion in the current year.

Prepayment of Vehicle License Fee (VLF) “Gap Loan.” The budget provides $1.2 billion in one-time funds to prepay a loan from local governments that was due in 2006-07. The loan is related to state VLF “backfill” payments to local governments (that is, payments that were made to local governments to compensate them for the reduction in revenues that occurred when the state lowered the rate on vehicle license fees). A portion of these backfill payments had been deferred in late 2002-03 and early 2003-04.

Mandate Payments. The budget funds about $239 million in mandates, substantially more than provided in 2004-05. About one-half of the total is related to two mandates requiring services for special education pupils, and is included in the Department of Mental Health’s budget.

“One-Time” Payments Related to Property Tax Shifts. A part of the 2004-05 budget package was a “swap” between the state and local governments, whereby the state stopped funding VLF backfill payments in return for a shift of property taxes from schools to local governments (the school property taxes are replaced with General Fund payments). Payments related to this swap are resulting in a one-time increase in General Fund spending for K-14 education, anticipated in the budget to be over $300 million in 2005-06.

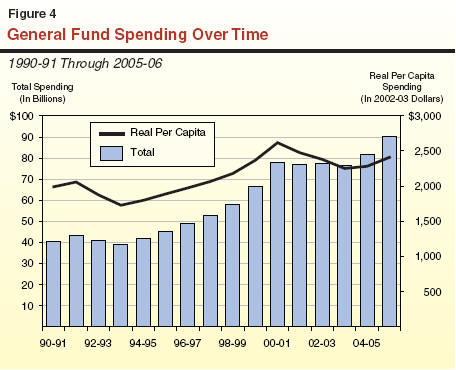

General Fund Spending Over Time

Figure 4 shows General Fund expenditures from 1990-91 through 2005-06 both in current dollars and as adjusted for population and inflation (that is, in real per capita terms). The figure indicates that after growing rapidly in the late 1990s, General Fund spending fell modestly during the 2001-02 through 2003-04 period, before resuming an upward trend in 2004-05. Total spending in 2005-06, is now 15 percent higher than the peak reached in 2000-01. Adjusted for inflation and population, however, real per capita spending is 8 percent below the 2000-01 peak.

In this section, we highlight the major developments in the evolution of the 2005-06 budget, beginning with the original Governor’s January budget proposal and ending in July 2005, when the budget was signed into law.

Governor’s January Proposal for 2005-06

In January 2005, the Governor proposed a 2005-06 General Fund budget which contained about $9.1 billion in solutions in order to both cover an estimated budget shortfall of $8.6 billion and maintain a $500 million reserve. This budget plan would also have reduced the state’s ongoing structural budget shortfall by roughly one-half-from $10 billion to under $5 billion per year. Figure 5 outlines the key savings contained in the original January budget plan.

|

Figure 5 Savings in the January 2005 Budget Plan |

|

|

|

Program Savings ($4.7 Billion) |

|

� Proposition 98 ($2.3 billion). |

|

� Social services cost-of-living adjustments and grant reductions ($0.7 billion). |

|

� In-Home Supportive Services wage contributions ($0.2 billion). |

|

� State employee compensation ($0.4 billion). |

|

� Local mandate suspensions ($0.2 billion). |

|

� Senior citizens’ tax assistance ($0.1 billion). |

|

� Other ($0.8 billion). |

|

Funding Shifts ($0.9 Billion) |

|

� State Teachers’ Retirement System contributions ($0.5 billion). |

|

� Transit “spillover” funds ($0.2 billion). |

|

� Federal funds ($0.2 billion). |

|

Loans and Borrowing ($3.4 Billion) |

|

� New deficit-financing bond sales ($1.7 billion). |

|

� Paterno settlement judgment bond ($0.5 billion). |

|

� Proposition 42 transfer ($1.3 billion). |

|

Tax Compliance ($0.1 Billion) |

|

� Tax gap proposals ($0.1 billion). |

Program Savings ($4.7 Billion). Of this total, about $2.3 billion was related to the two-year effect of holding the 2004-05 funding level for K-14 education at the level included in the 2004-05 Budget Act. Roughly $1 billion was related to reductions in social services. This included: (1) a 6.5 percent reduction in California Work Opportunity and Responsibility to Kids (CalWORKs) grants, (2) the elimination of CalWORKs grant COLAs, (3) the suspension of the state COLA for Supplemental Security Income/State Supplementary Program (SSI/SSP) (including no pass-through of the federal COLA), and

(4) the reduction in the state’s contribution to the wages of In-Home Supportive Services (IHSS) workers. Other savings included an increase in state employee pension contributions and other compensation-related savings, the suspension of various local mandates, the elimination of the senior citizens’ property tax assistance program, and a reduction in the senior citizens’ renters assistance program.

Funding Shifts ($0.9 Billion). The budget included three proposals in this area. First, the budget proposed that the state no longer fund annual base program contribution costs for the State Teachers’ Retirement System (STRS). Instead, these costs would be borne by the schools districts or their employees. Second, the budget proposed to retain Public Transportation Account “spillover” funds in the General Fund in 2005-06, instead of using them for public transit purposes. Third, the budget proposed to replace General Fund support for certain prenatal care services with new federal funds.

Loans and Borrowing ($3.4 Billion). The budget proposed to use $1.7 billion in deficit-financing bonds-about one-half of the amount remaining from the $15 billion authorized by voters in March 2004. It proposed to suspend the $1.3 billion Proposition 42 transfer of sales taxes on gasoline from the General Fund to transportation funds. The suspended amount would be paid over a

15-year period. It also assumed that the state would issue a “judgment bond” to finance a $464 million settlement of flood-related litigation (the Paterno case) against the state.

Tax Compliance ($0.1 Billion). The budget assumed a net gain of about $94 million related to tax compliance measures.

Other Features. In other areas, the budget provided increased funding for UC and CSU consistent with the Governor’s compact with higher education. It also included a series of changes to the Medi-Cal Program, including expansion of managed care for families and kids as well as the aged and disabled, new premiums for certain beneficiaries, and an imposition of a cap on adult dental services. It also included significant funding increases for judiciary and criminal justice areas.

May Revision

In the months following the release of the January budget plan, the state revenue picture improved significantly. The May Revision used these revenues to reduce borrowing and increase spending in a limited number of areas. The key changes incorporated in the May Revision plan are highlighted in Figure 6.

|

Figure 6 May Revision—Key Changes From January Proposal |

|

|

|

New Revenues ($4.2 Billion) |

|

�Increased revenues related to economy—$4 billion. |

|

� Increased revenues related to amnesty—$0.2 billion. |

|

New Proposals ($4.2 Billion) |

|

�Reduced borrowing ($2.3 billion). |

|

— Eliminate new deficit-financing bond sales ($1.7 billion). |

|

— Prepay one-half of vehicle license fee “gap loan” due in 2006‑07 ($0.6 billion). |

|

�New/restored spending ($1.8 billion). |

|

— Proposition 42 transfer to transportation ($1.3 billion). |

|

— Proposition 98 “settle-up” payments ($0.2 billion). |

|

— Senior citizens’ property tax and renters’ assistance programs ($0.1 billion). |

|

— Other ($0.2 billion). |

Improved Revenues. The May Revision assumed a $4.2 billion improvement in the revenue outlook. Of this total, about $4 billion was related to higher-than-expected tax liabilities, mostly from the personal income tax. The balance-$180 million-was related to an increase in the amount of net proceeds from the tax amnesty programs that had been adopted with the 2004-05 budget.

New Proposals. The May Revision reduced borrowing in two key areas. First, it eliminated the sale of $1.7 billion in deficit-financing bonds proposed in January. Second, it proposed to prepay one-half of the outstanding VLF gap loan from local governments. The key spending proposals were

(1) a restoration of the $1.3 billion Proposition 42 transfer, (2) $250 million in Proposition 98 “settle-up” payments (related to underpayments of the minimum funding guarantee in prior years), and (3) restoration of funds for the senior citizens’ property tax and renters’ assistance programs.

The May Revision retained most of the other January savings proposals, including those related to Proposition 98 education funding, CalWORKs and SSI/SSP grants, IHSS wages, employee compensation, and the STRS contributions. Within Proposition 98, it used the settle-up funds along with savings related to lower enrollment to fund a modest expansion of class-size reduction and a variety of other initiatives. It also retained most of the January proposals related to limited Medi-Cal reform, as well as funding increases for higher education and the judiciary.

Following the May Revision, the Conference Committee met in June to reconcile the budget differences of the two legislative houses. Following conference actions and subsequent negotiations between the Governor and legislative leadership, an agreement regarding the budget was reached in early July. The resulting budget was passed by both houses of the Legislature on July 7. After using his line-item veto authority to delete about $320 million ($114 million General Fund) in spending, the Governor signed the budget on July 11, 2005.

Comparison to the May Revision. The final budget package reflects a number of elements of the Governor’s May Revision plan. It funds Proposition 98 at the May Revision level, contains funding increases for CSU and UC which are consistent with May Revision, and incorporates some of the Medi-Cal changes proposed by the Governor.

However, the final budget also contained some significant changes from the May Revision (see Figure 7). Specifically, it provides for full versus one-half repayment of the VLF gap loan, fully funds the General Fund contribution to STRS, contains only modest reductions related to employee compensation, and includes smaller reductions in social services spending than proposed by the Governor. In the social services area, while the budget suspends state COLAs for both CalWORKs and SSI/SSP grants in 2005-06 and 2006-07, it does not include the Governor’s proposed 6.5 percent reduction in CalWORKs grant levels. Nor does it include the Governor’s proposal to permanently eliminate the statutory CalWORKs COLA or reduce the state’s IHSS wage contribution. The enacted budget also passes-through the federal COLA for SSI/SSP, but with a three-month delay.

|

Figure 7 Final Budget—Key Differences From May Revision |

|

|

|

�Full (instead of one-half) repayment of vehicle license fee gap loan. |

|

�State Teachers’ Retirement System contribution funded. |

|

�Reduced employee compensation savings. |

|

�Smaller reductions in social services: |

|

— No 6.5 percent California Work Opportunity and Responsibility to Kids (CalWORKs) grant reduction. |

|

— Federal pass-through of federal Supplemental Security Income/State Supplementary Program cost-of-living adjustment (COLA) delayed three months instead of suspended. |

|

— COLA’s for CalWORKs grants suspended (for two years) instead of eliminated. |

|

— No reduction in state In-Home Supportive Services wage contributions. |

In Medi-Cal, the budget expands managed care to additional counties, but generally rejects the administration’s proposal to require the enrollment of aged and disabled beneficiaries in managed care. It also does not include the administration’s proposal to require certain Medi-Cal beneficiaries to pay monthly premiums.

Finally, the final budget does not include $250 million in settle-up payments to schools. These funds were redirected to support the state’s contribution to the STRS program.

How Added Spending Relative to May Revision Was Financed. The additional spending resulting from the changes in the final budget noted above was partly supported by funding redirections. For example, the budget does not include $250 million in settle-up payments to schools that had been proposed in the May Revision. These funds were redirected to support the state’s contribution to the STRS program. Other financing sources included: (1) an increase in the 2004-05 revenue estimate, reflecting stronger-than-expected cash receipts in May; (2) a higher local property tax estimate, which lowers the General Fund spending requirement for Proposition 98; and

(3) a slightly lower 2005-06 year-end reserve.

Background. Article XIII B of the State Constitution places limits on the appropriation of taxes for the state and each of its local entities. Certain appropriations, however, such as for capital outlay and subventions to local governments, are specifically exempted from the state’s limit. As modified by Proposition 111 in 1990, Article XIII B requires that any revenues in excess of the limit that are received over a two-year period be split evenly between taxpayer rebates and increased school spending.

State’s Position Relative to Its Limit. As a result of the previous sharp decline in revenues, the level of state spending is now well below the spending limit. Specifically, state appropriations were $7.6 billion below the limit in 2004-05 and, based on the revenue and expenditure estimates incorporated in the 2005-06 budget, are expected to be $11.3 billion below the limit in 2005-06.

In addition to the 2005-06 Budget Act, the budget package includes a number of related measures enacted to implement and carry out the budget’s provisions. Figure 8 lists these bills at the time of budget enactment. The Legislature also considered various cleanup bills at the end of session, including SB 65 (Committee on Budget and Fiscal Review)-related to education.

|

Figure 8 2005‑06 Budget and Budget-Related Legislation |

|||

|

Bill Number |

Chapter |

Author |

Subject |

|

SB 77 |

38 |

Committee on Budget and Fiscal Review |

Budget (conference report) |

|

SB 80 |

39 |

Committee on Budget and Fiscal Review |

Budget revisions |

|

|

|

Trailer Bills |

|

|

AB 131 |

80 |

Budget Committee |

Health |

|

AB 138 |

72 |

Budget Committee |

Mandates |

|

AB 139 |

74 |

Budget Committee |

General government |

|

AB 145 |

75 |

Budget Committee |

Uniform civil filing fees |

|

SB 62 |

76 |

Committee on Budget and Fiscal Review |

Transportation |

|

SB 63 |

73 |

Committee on Budget and Fiscal Review |

Education |

|

SB 64 |

77 |

Committee on Budget and Fiscal Review |

Boards and commissions |

|

SB 68 |

78 |

Committee on Budget and Fiscal Review |

Social services |

|

SB 71 |

81 |

Committee on Budget and Fiscal Review |

Resources |

|

SB 76 |

91 |

Committee on Budget and Fiscal Review |

Hydrogen highway/PIER |

The budget package includes $50 billion in Proposition 98 spending in 2005-06 for K-14 education. This represents an increase of $3 billion, or 6.4 percent, from the revised 2004-05 spending level. Figure 1 summarizes the budget package for K-12 schools, community colleges, and other affected agencies. As discussed later, the enacted budget package also includes an additional $407 million in one-time funds for K-14 education ($382 million for K-12 and $25 million for community colleges) needed to meet prior-year Proposition 98 obligations.

|

Figure 1 Proposition 98 Budget Summary |

||||

|

(Dollars in Billions |

||||

|

|

Revised |

|

Change |

|

|

|

2004-05 |

2005-06 |

Amount |

Percent |

|

K-12 Proposition 98 |

|

|

|

|

|

General Fund |

$30.9 |

$33.1 |

$2.2 |

7.1% |

|

Local property taxes |

11.2 |

11.6 |

0.4 |

3.4 |

|

Subtotals, K-12 |

($42.1) |

($44.6) |

($2.6) |

(6.1%) |

|

Average Daily Attendance (ADA) |

5,990,309 |

6,031,404 |

41,095 |

0.7 |

|

Amount per ADA (in dollars) |

$7,023 |

$7,402 |

$378.9 |

5.4% |

|

California Community Colleges |

|

|

||

|

General Fund |

$3.0 |

$3.4 |

$0.4 |

12.4% |

|

Local property taxes |

1.7 |

1.8 |

0.1 |

3.7 |

|

Subtotals, Community Colleges |

($4.8) |

($5.2) |

($0.4) |

(9.3%) |

|

Other Agencies |

$0.1 |

$0.1 |

— |

— |

|

Totals, Proposition 98 |

$46.9 |

$50.0 |

3.0 |

6.4% |

|

General Fund |

$34.0 |

$36.6 |

2.6 |

7.6% |

|

Local property taxes |

12.9 |

13.4 |

0.4 |

3.4 |

General Fund Share of Proposition 98 Driven by Property Tax Shifts. As shown in Figure 1, the budget assumes that $13.4 billion, or approximately 27 percent of overall 2005-06 Proposition 98 spending, will be funded by local property taxes. The remaining 73 percent is supported by the General Fund. This is essentially the same proportional split between Proposition 98 funding sources as the prior year. The nearby box explains the impact that recent property tax shifts have had on the General Fund share of school funding in recent years.

Impact of the 2004-05 Property Tax Shifts On Proposition 98As part of the 2004-05 budget package and the implementation of Proposition 1A and Proposition 57, the state authorized several transfers of local property tax revenues between schools (K-12 school districts and community colleges) and local governments (cities, counties, and special districts). The figure below shows that in 2004-05 and 2005-06 the state reallocated a net of $3.9 billion and $5.2 billion in local property tax revenues from schools to local governments, respectively. These transfers were backfilled by the state providing additional General Fund revenues to schools to meet the Proposition 98 spending levels for those years.

The 2004-05 budget package provided local governments $4.1 billion in higher local property tax revenues in exchange for no longer receiving an equivalent amount of vehicle license fee (VLF) backfill. Because the estimated VLF backfill, which would have otherwise occurred, was higher than anticipated in the 2004-05 budget, the 2005-06 budget provides a $324 million settle-up payment (additional local property tax revenues) to local governments. In addition, the size of the property tax shift is budgeted to grow to $4.8 billion for 2005-06. Because of the significant fiscal impact of the VLF-related property tax transfer and legislative concerns with the backfill calculation, the Legislature asked the Bureau of State Audits to investigate the issue. The audit is to be concluded by October 1, 2005. The state dedicated a portion of the sales tax revenues that previously went to local governments to finance the deficit-financing bonds authorized by Proposition 57. In exchange, local governments received property tax revenues that previously went to schools, and schools received additional General Fund revenues instead of local property tax revenues. This set of transfers, referred to as the “triple flip,” transferred $1.1 billion from schools to local governments in 2004-05 and $1.4 billion in 2005-06. The 2005-06 budget also includes $33 million in settle-up costs for the triple flip for 2004-05. Finally, as part of the 2004-05 budget package, local governments agreed to receive $1.3 billion less local property tax revenues for the 2004-05 and 2005-06 budget years, allowing these funds to be used by schools to meet the state’s Proposition 98 obligations. This shift will end in 2006-07, resulting in schools receiving less local property tax revenues and the General Fund contribution to overall Proposition 98 spending increasing by $1.3 billion. |

|||||||||||||||||||||||||||

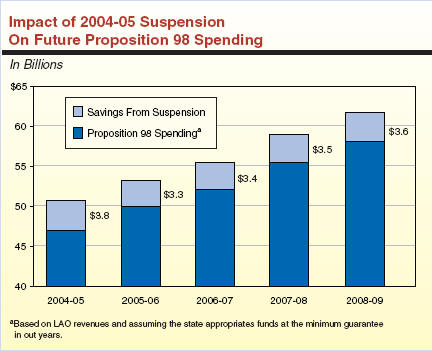

Unanticipated Revenue Growth in 2004-05 Results in Greater Savings From the Proposition 98 Suspension. Chapter 213, Statutes of 2004 (SB 1101, Budget Committee) suspended the Proposition 98 guarantee for 2004-05 (see box below). When the 2004-05 Budget Act was adopted, the impact of the suspension was a $2 billion savings to the state. During the 2004-05 fiscal year, the California economy experienced better-than-expected revenue growth. Indeed, the per capita General Fund revenues used to calculate the Proposition 98 minimum guarantee grew by 9.1 percent from 2003-04 to 2004-05. The higher-than-expected revenue growth in 2004-05 resulted in

a $1.8 billion increase in the minimum guarantee from the level assumed

in the 2004-05 budget (after adjusting for technical changes resulting mainly from lower-than-expected K-12 enrollment). Because the minimum guarantee increased and the spending level remained the same, the higher General Fund revenue growth led to the state realizing an even greater savings from the suspension. Specifically, the savings increased from $2 billion to $3.8 billion.

Effects of the 2004-05 Proposition 98 SuspensionIn most years, Proposition 98 minimum funding levels, or guarantees, are determined by a constitutional formula based on three factors: (1) growth in K-12 attendance, (2) growth in per capita personal income, and (3) growth in per capita General Fund revenues. However, the Constitution also allows the Legislature to suspend this formula-driven minimum guarantee in any given fiscal year and to set Proposition 98 funding at whatever level it chooses for that year. Suspension of the Minimum Guarantee in 2004-05. Last year, given California’s continuing structural imbalance between revenues and expenditures, the state suspended the minimum Proposition 98 guarantee for 2004-05. The legislation authorizing the suspension-Chapter 213, Statutes of 2004 (SB 1101, Committee on Budget and Fiscal Review)-established a target funding level for K-14 education that was $2 billion lower than the amount called for by the guarantee. Over the course of the 2004-05 fiscal year, an improving economy led to the state receiving approximately $3.4 billion in additional General Fund revenues over what was projected when the 2004-05 Budget Act was enacted. Because the Proposition 98 guarantee is partially determined by growth in per capita General Fund revenues, the increase in revenues from the budget act forecast would have resulted in a significant increase to the K-14 minimum guarantee in 2004-05, had the state not suspended Proposition 98. Specifically, the minimum guarantee would have increased an additional $1.8 billion above what was estimated at the time of the budget act. Correspondingly, the target funding level set by Chapter 213 (the minimum guarantee less $2 billion) also increased by $1.8 billion as a result of the additional revenues received by the state. Ultimately, in order to realize an additional $1.8 billion in savings, the Legislature decided to maintain the Proposition 98 appropriation level that was set at the time of the 2004-05 Budget Act (adjusted downward slightly due to less-than-anticipated growth in K-12 attendance). That is, the overall Proposition 98 spending level for 2004-05 was set at approximately $46.9 billion, or $3.8 billion less than what the minimum guarantee would have been absent suspension. Current law requires the $3.8 billion in state savings resulting from the suspension to be tracked as maintenance factor and restored to the K-14 funding base in future years when General Fund revenues grow faster than the economy. Long-Run Impact of Suspension on K-14 Spending. The decision regarding the 2004-05 appropriation level for Proposition 98 is significant because it determines what the minimum guaranteed funding level will be in future years. The lower appropriation levels that result from suspending the Proposition 98 minimum guarantee in 2004-05 likely will yield savings to the state in future budgets. The Figure shows our estimate of the annual savings to the state from the 2004-05 Proposition 98 suspension. The figure also shows that the $3.8 billion of savings from 2004-05 decreases to $3.3 billion in 2005-06 due to an appropriation over the minimum guarantee (as discussed in the text). Annual savings from the suspension will continue in the future until the state fully restores the outstanding maintenance factor over the next several years.

|

Slow Revenue Growth in 2005-06 Will Result in Small Growth in the Proposition 98 Guarantee. The 2005-06 budget assumes that per capita General Fund revenues, a key factor in determining the Proposition 98 guarantee, will grow at a moderate rate of 3.7 percent over 2004-05 levels. This moderate growth results in the minimum guarantee being determined by Test 3 for 2005-06, the formula used when General Fund revenues grow slower than the economy (as measured by growth in personal income). This leads to the minimum guarantee growing by only $2.3 billion.

Education Spending in the 2005-06 Budget Act Is Above the Proposition 98 Minimum Guarantee. Between January 2005 and the adoption of the final budget, the 2004-05 revenue estimates increased dramatically (as discussed earlier); however, the General Fund revenue estimates for 2005-06 changed very little. Because the 2005-06 revenue assumptions did not change much, the May Revision maintained the same dollar amount for Proposition 98 spending as proposed by the Governor in the January budget. The final budget maintains spending at this level despite the lower guarantee resulting from the Test 3 calculation. This results in the appropriation level contained in the 2005-06 Budget Act being approximately $741 million more than the Test 3 minimum guarantee requires. This spending level is also above the Test 2 level for 2005-06 by $216 million, and helps to restore a portion of the “maintenance factor” created as a result of suspending the minimum guarantee in 2004-05. After accounting for this $741 million overappropriation, the state continues to realize around $3.3 billion in savings in 2005-06 due to last year’s suspension of Proposition 98.

K-14 Education Credit Card Update

Starting in 2001-02, the Legislature opted to defer significant education program costs to the subsequent fiscal year rather than make additional spending cuts. Additionally, for several years the state has not provided funding for reimbursement of education mandate costs. Combined with ongoing revenue limit reductions made in 2003-04, we have referred to these outstanding debts as the education “credit card,” to reflect the amounts the state has borrowed from schools and community colleges. Figure 2 shows that the budget continues to defer approximately $3.1 billion in K-14 costs to the future. As discussed later, the budget package does provide $406 million to partially eliminate the revenue limit deficit factor, and about $71 million in one-time Proposition 98 funds to pay outstanding education mandate costs for districts and community colleges. However, since the budget does not fund the ongoing costs of education mandates (estimated to be about $250 million annually), cumulative deferrals remain at about $3.1 billion in 2005-06.

|

Figure 2 Update on the K-14 Education Credit Card Balance |

||||

|

Year-End Balances |

||||

|

|

2002-03 |

2003-04 |

2004-05 |

2005-06 |

|

One-Time Costs |

|

|

|

|

|

Revenue limit and categorical deferrals |

$2,158 |

$1,097 |

$1,083 |

$1,103 |

|

Community college deferral |

— |

200 |

200 |

200 |

|

Cumulative mandate deferrals |

690 |

960 |

1,205 |

1,460 |

|

Ongoing Costs |

|

|

|

|

|

Revenue limit deficit factor (including basic aid) |

— |

$906 |

$663 |

$290 |

|

Totals |

$2,848 |

$3,163 |

$3,151 |

$3,053 |

As shown in Figure 1, spending on 2005-06 K-12 Proposition 98 totals $44.6 billion, an increase of about $2.6 billion, or 6 percent, from the revised 2004-05 spending level. This net change consists primarily of increased funding for enrollment growth and cost-of-living adjustments (COLA), funding restorations to ongoing programs, and a limited number of new programs.

Per Pupil Spending

The revised 2004-05 budget yields a K-12 per pupil funding level of $7,023. The 2005-06 budget results in per pupil funding of $7,402, an increase of $379, or 5.4 percent, above the 2004-05 level.

In 2001-02 through 2003-04, the state deferred expenses from one year to another (as discussed above). In past years, these deferrals-which pay districts for program services that were provided in the previous year-have made cross-year per pupil funding comparisons difficult. This is because the “programmatic” funding, or the level reflecting districts’ actual services and expenditures for a given year, have tended to differ from budgeted funding, or the amount districts technically received in that fiscal year. Figure 3 shows these differences.

|

Figure 3 K-12 Proposition 98

Spending Per Pupil |

||||

|

|

2002‑03 |

2003‑04 |

Revised 2004‑05 |

Proposed 2005‑06 |

|

Budgeted Funding |

|

|

|

|

|

Amount per ADAa |

$6,598 |

$7,018 |

$7,023 |

$7,402 |

|

Percent growth |

— |

6.4% |

0.1% |

5.4% |

|

Programmatic Fundingb |

|

|

|

|

|

Amount per ADA |

$6,786 |

$6,874 |

$7,021 |

$7,405 |

|

Percent growth |

— |

1.3% |

2.1% |

5.5% |

|

a Average daily attendance. |

||||

|

b To adjust for the deferrals, we counted funds toward the fiscal year in which school districts had programmatically committed the resources. The deferrals meant, however, that the districts technically did not receive the funds until the beginning of the next fiscal year. |

||||

While the state continued the practice of deferring some payments to districts in both 2004-05 and 2005-06, the amount of deferrals remained relatively the same in these two years. Thus, as shown in Figure 3, the year-to-year growth comparison between 2004-05 and 2005-06 is relatively equivalent for both programmatic and budgeted per pupil spending. That is, K-12 Proposition 98 per pupil spending increased roughly 5.5 percent from 2004-05 both considering how much is actually provided in the 2005-06 budget and the level of resources that districts will programmatically commit this year.

Major K-12 Funding Changes

Figure 4 displays major K-12 funding changes from the revised 2004-05 budget. The budget package provides about $2.6 billion in new ongoing K-12 expenditures. In general, the budget fully funds base programs adjusted for growth and COLA. In addition, the budget provides an additional $406 million in general purpose funds to restore reductions and foregone COLAs from prior years.

|

Figure 4 Major K-12

Proposition 98 Changes From |

|

|

(In Millions) |

|

|

Revenue Limit |

|

|

Cost-of-living adjustment (COLA) |

$1,301.9 |

|

Growth |

189.7 |

|

Public Employees’ Retirement System and |

-116.1 |

|

Deficit factor reduction (including basic aid) |

406.2 |

|

Subtotal |

($1,781.8) |

|

Categorical Programs |

|

|

COLA |

$420.0 |

|

Growth |

138.5 |

|

Restore categoricals funded with one-time funds |

151.5 |

|

Special education augmentations |

70.8 |

|

Veto set-asides |

22.0 |

|

High school exit exam—student assistance |

20.0 |

|

Other |

-31.0 |

|

Subtotal |

($791.8) |

|

Total Changes |

$2,573.6 |

|

|

|

|

a Assumes enactment of

SB 65 (Committee on Budget and Fiscal Review), an education budget

|

|

Major funding changes include:

Growth and COLA ($2.05 Billion). The budget provides $1.7 billion to fund a 4.23 percent COLA for revenue limits and most categorical programs (including statutory and discretionary COLAs). The budget provides $328 million to fund growth (0.7 percent) for revenue limit and most categorical programs.

Deficit Factor Reduction ($406 Million). The budget package provides $406 million in general purpose funds by reducing the revenue limit deficit factor for school districts and county offices of education. In 2003-04, the state reduced revenue limits and did not provide a COLA, creating a “deficit factor” of 3.02 percent that would eventually need to be restored. The revenue limit reduction was partially restored in 2004-05, and the 2005-06 budget package provides further deficit factor restoration. The remaining deficit factor for school districts is now .892 percent. The budget package requires that the remaining deficit factors for both districts and county offices (roughly $290 million) be restored in 2007-08.

Public Employees’ Retirement System (PERS) and Unemployment Insurance (-$116 Million). The Legislature fully funds PERS and Unemployment Insurance, but saves $116 million compared to 2004-05 because of reduced contribution rates for these two programs.

Restoration of Categorical Programs’ Funding Base ($152 Million). The 2004-05 budget used roughly $152 million in one-time funds to support ongoing programs. The 2005-06 budget provides ongoing support for those programs.

Special Education Augmentations ($71 Million). The budget package increases General Fund support for special education by $70.8 million as follows: (1) $52.6 million in ongoing funds for per pupil grants that may be used for any one-time costs (with first priority to help special education students pass the California High School Exit Examination) and (2) an $18.2 million augmentation to the new Out-of-Home Care funding formula. The budget also provides $12.8 million in federal funds as an increase in base special education per pupil grants. To address issues created in the reauthorization of federal special education law, the budget also revises the calculation of the annual COLA to provide an adjustment only on the state-funded portion of the special education budget. With this change, COLAs for the federally funded portion of the program will be considered as part of the annual budget process, relying first on increases in federal funds for special education.

High School Exit Exam-Student Assistance ($20 Million). The only new ongoing program included in the 2005-06 budget is an assistance program for high schools with large percentages of students failing the high school exit exam. These schools will receive $600 for each student who has failed one or both parts of the exam (assuming enactment of AB 128 [Committee on Budget], which amends the 2005-06 Budget Act and provides additional detail on how these funds are to be utilized). These additional resources may be used for a broad set of activities to help students in the class of 2006 pass the exit exam.

Other major budget actions include:

Teacher Retirement Costs. The budget does not include the Governor’s proposal to shift $469 million in teacher retirement costs from the General Fund (non-Proposition 98) to schools and/or teachers. The General Fund continues to fund the state’s contribution to the retirement program. The budget also includes a one-time augmentation of $31 million for a statutorily required payment to reduce the retirement system’s unfunded costs.

High Priority Schools New Cohort. The budget redirects $60 million in savings from schools exiting the state’s intervention programs to create a new cohort of High Priority Schools (Academic Performance Index [API] decile 1 and 2 schools). These schools will receive $400 per pupil to improve their academic performance. In exchange, these schools will have to meet specific achievement targets or potentially face state sanctions.

Child Care Reforms. The Legislature did not adopt the Governor’s proposed child care reforms, which would have changed eligibility for working poor and California Work Opportunity and Responsibility to Kids (CalWORKs) families and created a tiered reimbursement system.

Additional One-Time Funds

The budget provides an additional $382 million in one-time K-12 education funds needed to meet Proposition 98 obligations from prior years. (The Governor’s May Revision included an additional $235 million in one-time Proposition 98 funds, but during final budget negotiations these funds were shifted to help offset the General Fund cost of fully funding the state’s contribution to the teachers’ retirement program.) Figure 5 shows the uses of the one-time funds included in the final budget package.

|

Figure 5 K-12 Spending From One-Time Funds |

|

|

(In Millions) |

|

|

|

|

|

School facilities emergency repairs (Williams settlement) |

$196.0 |

|

Payment of prior K-12 mandate claims |

60.6 |

|

Low-Performing School Enrichment Block Grant |

49.5 |

|

Special Education |

26.0 |

|

Fruits and Vegetables Initiative |

18.2 |

|

Charter School Facilities Grants |

9.0 |

|

Other |

22.3 |

|

Total |

$381.6 |

The major one-time spending includes:

School Facilities Emergency Repairs ($196 Million). As part of the settlement of Williams v. California, the state is required to commit one-half of the funds in the Proposition 98 reversion account (funds appropriated for K-14 education in prior years, but not used) for emergency facility repairs. The 2005-06 budget meets this obligation by providing $196 million for this purpose.

K-12 Education Mandates ($61 Million). The budget provides $61 million in one-time funds to pay for mandate costs deferred from prior years.

Low-Performing School Enrichment Block Grant ($49.5 Million). The budget provides up to $49.5 million for grants to schools in API deciles 1 through 3 to improve the education culture and environment at those schools. Schools would have broad discretion to determine how these funds are used-including changes to facilities, safety, support services for students and teachers, and bonuses for recruitment and retention.

Special Education ($26 Million). The budget package reappropriates $26 million in order to meet the federal maintenance-of-effort requirements for the 2003-04 special education program. Of this amount, $3.2 million will augment the Out-of-Home Care program for 2004-05 and the remaining $22.8 million will be available for any local special education purpose.

K-12 Vetoes

The Governor vetoed $22 million in ongoing K-12 funding, including $20 million for instructional materials for English learners and $2 million for the Healthy Start program. The Governor set aside the funding for future legislation. The Legislature subsequently passed and sent to the Governor SB 72 (Committee on Budget and Fiscal Review), which restores the $20 million in vetoed funding for instructional materials for English learners. The Governor also vetoed $74 million in federal carryover funds from various programs, and set the funds aside in accordance with a May Revision proposal to redirect carryover funds to low performing schools and districts. The Legislature rejected this May Revision proposal.

The enacted budget provides a total of $9.7 billion in General Fund support for higher education in 2005-06 (see Figure 6). This reflects an increase of $882 million, or 10 percent, above the amount provided in 2004-05. In addition, student fee increases approved for the University of California (UC) and the California State University (CSU) will provide another $190 million in new, unrestricted funding for the university systems. Student fees were not increased at the California Community Colleges (CCC).

|

Figure 6 Higher Education

Budget Summary |

||||

|

(Dollars in Millions) |

||||

|

|

|

|

Change |

|

|

|

2004-05 |

2005-06 |

Amount |

Percent |

|

University of California |

$2,715.1 |

$2,844.9a |

$129.8 |

4.8% |

|

California State University |

2,481.1 |

2,616.8a |

135.8 |

5.5 |

|

California Community Colleges |

3,050.5 |

3,512.9b |

462.4 |

15.2 |

|

Student Aid Commission |

598.6 |

752.4 |

153.9 |

25.7 |

|

California Postsecondary |

2.1 |

2.1 |

— |

— |

|

Hastings College of the Law |

8.1 |

8.4 |

0.2 |

3.0 |

|

Totals |

$8,855.5 |

$9,737.5 |

$882.0 |

10.0% |

|

|

||||

|

a Includes $1.7 million for master’s nursing programs, as described in text under “Enrollment Funding.” |

||||

|

b Includes $37.4 million vetoed by the Governor and "set aside" to be appropriated for career technical education. |

||||

UC and CSU

Overview. The budget provides $2.8 billion in General Fund support for UC in 2005-06. This is $130 million, or 4.8 percent, more than was provided in the prior year. For CSU, the budget provides $2.6 billion in General Fund support in 2005-06. This is an increase of $136 million, or 5.5 percent, from 2004-05. In addition to these General Fund appropriations, UC and CSU will receive $114 million and $76 million, respectively, in new revenue from student fee increases. The budget allows UC and CSU to determine how this additional fee revenue will be spent.

Student Fees. Consistent with the Governor’s January budget proposal, the UC Regents and the CSU Board of Trustees approved fee increases for their respective segments for the 2005-06 academic year. As shown in Figure 7, undergraduate fees at both segments would increase by 8 percent and graduate fees increase by 10 percent. Professional school fees and nonresident tuition also have increased for 2005-06.

|

Figure 7 Student Fees |

||||

|

Annual Systemwide Tuition and Fees for Full-Time Students |

||||

|

|

|

|

Change From 2004-05 |

|

|

|

2004-05 |

2005-06 |

Amount |

Percent |

|

University of California |

|

|

|

|

|

Resident Fees |

|

|

|

|

|

Undergraduate students |

$5,684 |

$6,141 |

$457 |

8% |

|

Graduate students |

6,269 |

6,897 |

628 |

10 |

|

Professional school students |

|

|

|

|

|

Public Health |

$6,269 |

$10,792 |

$4,523 |

72% |

|

Public Policy |

6,269 |

10,792 |

4,523 |

72 |

|

International Relations/Pacific Studies |

6,269 |

10,792 |

4,523 |

72 |

|

Nursing |

8,389 |

9,941 |

1,552 |

19 |

|

Theater, Film, and Television |

11,249 |

12,751 |

1,502 |

13 |

|

Optometry |

14,139 |

16,132 |

1,993 |

14 |

|

Pharmacy |

14,139 |

17,641 |

3,502 |

25 |

|

Veterinary Medicine |

16,029 |

17,674 |

1,645 |

10 |

|

Dentistry |

18,024 |

21,276a |

3,252 |

18 |

|

Medicine |

18,513 |

20,232 |

1,719 |

9 |

|

Law |

19,113 |

22,128a |

3,015 |

16 |

|

Business Administration |

19,324 |

22,422a |

3,098 |

16 |

|

Nonresident Tuition and Fees |

|

|

|

|

|

Undergraduate students |

$22,640 |

$23,961 |

$1,321 |

6% |

|

Graduate students |

21,208 |

21,858 |

650 |

3 |

|

California State University |

|

|

|

|

|

Resident Fees |

|

|

|

|

|

Undergraduate students |

$2,334 |

$2,520 |

$186 |

8% |

|

Teacher education students |

2,706 |

2,922 |

216 |

8 |

|

Graduate students |

2,820 |

3,102 |

282 |

10 |

|

Nonresident Tuition and Fees |

|

|

|

|

|

Undergraduate students |

$12,504 |

$12,690 |

$186 |

1% |

|

Graduate students |

12,990 |

13,272 |

282 |

2 |

|

|

||||

|

a Represents midpoint of fee range. |

||||

Enrollment Funding. The budget includes a total of $88.7 million to fund 2.5 percent enrollment growth at UC ($37.9 million) and CSU ($50.8 million). In addition, the enacted budget package makes a one-time reversion of $15.5 million from CSU’s prior-year enrollment funding because CSU did not use this money to enroll students. (The CSU’s 2004-05 enrollment was about 2,700 full-time equivalent [FTE] students less than budgeted.)

The Legislature also adopted language directing the Legislative Analyst’s Office and the Department of Finance to jointly convene a working group to review the current “marginal cost” methodology for funding new enrollment at the two segments and to provide recommendations that would be considered for the 2006-07 budget.

The 2005-06 budget also provides additional funding (above the standard marginal cost amount) for expanded enrollment in specified medical degree programs. Specifically, the budget includes $300,000 for 20 additional medical students in UC’s Program in Medical Education for the Latino Community (PRIME-LC). The PRIME-LC trains physicians specifically to serve in underrepresented communities. In addition, the Legislature added $4 million to expand enrollment in CSU’s entry-level master’s nursing programs, as authorized in Chapter 718, Statutes of 2004 (SB 1245, Kuehl). The Governor vetoed all but $560,000 of the CSU augmentation, and in his veto message called on the Legislature to appropriate the vetoed funds through separate legislation. The Legislature subsequently passed and sent to the Governor SB 73 (Committee on Budget and Fiscal Review), which appropriates $1.72 million to UC and $1.72 million to CSU for one-time costs to support master’s nursing programs.

Outreach Programs. In adopting the 2005-06 budget, the Legislature rejected the Governor’s proposal to reduce state support for UC and CSU’s outreach programs. Instead, the budget maintains funding for these programs at their 2004-05 levels. In signing the budget, the Governor expressed his expectation that UC and CSU would work with the administration to “fully evaluate the cost-effectiveness of each program and eliminate those that cannot demonstrate an adequate return on investment.”

Base Budget Increases. Both university systems received base budget increases of 3 percent. These increases amount to $76.1 million for UC and $71.7 million for CSU. These funds, which generally offset the impact of inflation, may be used for any purpose.

Other Features. For UC, the budget includes $14 million for the Merced campus, which opened in September 2005. The Legislature rejected the Governor’s proposal to eliminate funding for UC’s Labor Institute, and provided $3.8 million to fund the Institute at the prior-year’s level. The Governor vetoed this augmentation.

CCC

Unlike UC and CSU, the CCC receive substantial funding from local property taxes. These revenues, when combined with General Fund support, accounts for CCC’s funding under Proposition 98. The 2005-06 budget provides CCC with $5.2 billion in Proposition 98 support. This is $442 million, or 9.3 percent, more than was provided in 2004-05. The CCC’s share of total Proposition 98 support is 10.4 percent, which exceeds the 2004-05 level of 10.2 percent.

The General Fund portion of CCC’s funding totals $3.5 billion in 2005-06, which reflects an increase of $462 million, or 15.2 percent, from the revised 2004-05 level. The large General Fund increase is due in part to a one-time property tax adjustment in 2005-06.

Major features of CCC’s budget include:

$210 million for a COLA of 4.23 percent.

$142 million for enrollment growth of 3 percent, or about 34,000 FTE students.

$31.4 million to restore general apportionment funding vetoed in 2004-05.

$30 million for equalization.

$10 million in one-time funds to pay for state-mandated program costs incurred by community colleges in prior years.

Career Technical Programs. In the January budget proposal and the May Revision, the Governor proposed a total of $37.4 million in one-time Proposition 98 funding to align career technical (vocational) curricula between K-12 schools and CCC economic development programs. The Legislature approved $20 million of this proposal, but added provisional language that linked this funding to the same level of funding for instructional materials for K-12 English learners. The Governor vetoed the $20 million as well as $17.4 million of the amount that the Legislature had appropriated to backfill an anticipated shortfall in local property taxes. The Governor “set aside” these vetoed funds for anticipated legislation that would fund career technical education. (This funding is reflected in the community college General Fund total in Figure 6.) The Legislature subsequently passed and sent to the Governor SB 70 (Scott), which restores a portion of the vetoed funding.

Accountability. The 2005-06 budget package includes trailer legislation (Chapter 73, Statutes of 2005 [SB 63, Committee on Budget and Fiscal Review]), that creates a district-level accountability system for CCC. The legislation requires community college districts to report specified data to the CCC Chancellor’s Office, which in turn would submit an annual report to the Legislature and the Governor. The first report is due by March 1, 2007.

Nursing Programs. The 2005-06 budget includes $10 million in ongoing Proposition 98 funding to support an expansion of nursing programs at community colleges. This funding, coupled with $4 million in one-time funds, is intended to increase the capacity of nursing programs through recruiting new faculty and purchasing new equipment. This funding is part of a larger nursing initiative adopted by the Legislature, which also expands financial aid opportunities for nurses (described in the following section) and includes funding in the health and social services areas (described later in this report).

Student Fees. Student fee levels remain at $26 per unit, which is unchanged from 2004-05.

Financial Aid and California Student Aid Commission

The budget provides $816 million (all fund sources) for various financial aid programs administered by the Student Aid Commission. The Cal Grant programs will receive the bulk of this funding-$775 million, which is $61 million, or 8 percent, above the prior-year level. In 2005-06, the Cal Grant programs are estimated to serve approximately 191,500 students, which reflects an increase of 6,350 students. Of total Cal Grant funding, $51 million comes from the Student Loan Operating Fund. The budget also provides a $7 million General Fund augmentation, reflecting a 20 percent increase, for the Assumption Program of Loans for Education (APLE). The higher APLE costs are associated with prior-year warrants expected to be redeemed in 2005-06.

The budget also authorizes the commission to issue 100 warrants for the State Nursing Assumption Program of Loans for Education (SNAPLE). This is a new financial incentive program designed to encourage more individuals to become nursing faculty. After receiving their graduate degree and completing the equivalent of one year of full-time work as nursing faculty members, SNAPLE recipients will have up to $8,333 of their education loans forgiven. Additional loan forgiveness of the same amount is provided for up to two additional full-year equivalents of faculty work, for total potential loan forgiveness of $25,000.

Additionally, the Supplemental Report of the 2005-06 Budget Act includes two financial aid-related provisions. The first requires a working group of various state and segmental agencies to define the support documentation concerning UC and CSU’s institutional aid programs that should accompany future budget proposals. The second requires our office by December 31, 2005, to complete a study of the commission and EdFund’s governance, roles, and responsibilities.

The 2005-06 budget plan provides about $17.9 billion from the General Fund for health programs, which is an increase of about $1.8 billion, or 11.5 percent, compared to the revised prior-year level of spending as shown in Figure 8. Several key aspects of the budget package are discussed below and summarized in Figure 9.

|

Figure 8 Health Services

Programs |

||||

|

(Dollars in Millions) |

||||

|

|

|

|

Change |

|

|

|

2004-05 |

2005-06 |

Amount |

Percent |

|

Medi-Cal (local assistance only) |

$11,702 |

$12,984 |

$1,282 |

11.0% |

|

Department of Developmental Services |

2,133 |

2,284 |

152 |

7.1 |

|

Department of Mental Health |

984 |

1,295 |

312 |

31.7 |

|

Healthy Families Program (local assistance only) |

293 |

346 |

53 |

18.1 |

|

Department of Alcohol and Drug Programs |

237 |

243 |

6 |

2.5 |

|

All other health services |

676 |

708 |

32 |

4.7 |

|

Totalsa |

$16,024 |

$17,861 |

$1,836 |

11.5% |

|

|

||||

|

a Totals may not add due to rounding. |

||||

|

Figure 9 Major Changes—State Health Programs |

|

|

(In Millions) |

|

|

2005‑06 General Fund Effect |

|

|

Medi-Cal |

|

|

Adjust for net increase in base program costs |

$484 |

|

Increase rates for nursing homes |

404 |

|

Continue higher rates for Los Angeles County clinics |

30 |

|

Increase rates for two managed care plans |

11 |

|

Medicare Part D Drug Benefit |

|

|

Reflect "clawback" payments owed to federal government |

$511 |

|

Continue coverage of selected drugs not covered by Medicare |

47 |

|

Adjust for savings on Medi-Cal drug costs |

-760 |

|

Reduce payments to managed care plans |

-58 |

|

Public Health |

|

|

Provide local assistance to combat West Nile Virus outbreak |

$12 |

|

Augment AIDS prevention and education efforts |

6 |

|

Use Proposition 99 funds to offset costs of hospital rate increases |

-26 |

|

Prenatal Care Services |

|

|

Shift Medi-Cal and AIM prenatal services to federal fundsa |

-$192 |

|

Healthy Families Program |

|

|

Increase application assistance and enrollment activities |

$6 |

|

Implement increase in premiums for higher-income families |

-5 |

|

Emergency Medical Services Authority |

|

|

Provide grants to improve the operation of trauma care centers |

$10 |

|

Department of Developmental Services |

|

|

Adopt unallocated reductions, rate freeze, other temporary savings |

-$84 |

|

Department of Mental Health (DMH) |

|

|

Fund two state mandates for special education children |

$120 |

|

Activate beds at new state hospital in Coalinga |

66 |

|

Shift General Fund support for prison inmates to DMG |

61 |

|

Include lease-revenue bond payments for Coalinga State Hospital |

27 |

|

|

|

|

a Reflects combined savings for 2004 05 and 2005 06. |

|

Medi-Cal

The 2005-06 enacted budget provides about $13 billion from the General Fund ($34.9 billion all funds) for Medi-Cal local assistance expenditures. This amounts to about a $1.3 billion, or 11 percent, increase in General Fund support for Medi-Cal local assistance. The increase in expenditures reflects (1) ongoing growth in caseload; (2) increases in costs and utilization of medical services in the base program; (3) rate increases for nursing homes and certain other providers; and (4) a number of significant policy changes in Medi-Cal, including those described below.

Medi-Cal Redesign-Expansion of Managed Care. The budget plan expands Medi-Cal managed care to additional counties, but generally rejects an administration proposal to mandate the enrollment of aged and disabled beneficiaries in managed care. The exception would be aged and disabled beneficiaries who enroll in county organized health systems, consistent with the current practice. Funding to begin implementing these changes is provided in 2005-06. However, savings from these changes would not be realized for several years.

A proposal for long-term care integration of health and social services programs in three counties, which was a part of the original managed care expansion package, was not approved as part of the budget plan.

Medi-Cal Redesign-Other Proposals. The budget plan adopts a $1,800 annual limit on dental services provided to adults. In so doing, the Legislature modified an administration proposal for a dental cap in a way that will result in lower savings but also affect fewer Medi-Cal beneficiaries. However, the budget plan does not include some other components of an administration plan to redesign the Medi-Cal Program, including a proposal to require certain Medi-Cal beneficiaries to pay monthly premiums to participate in the program.

Restructuring Hospital Finances. No changes in the structure of state support for public and private hospitals were incorporated in the budget, but it assumes that a new federal hospital waiver will be implemented in the budget year. A recent agreement between the administration and federal authorities over such changes was approved by the Legislature in separate policy legislation. In a related matter, the budget plan continues payments to certain Los Angeles County health clinics at an enhanced reimbursement rate that would otherwise have been discontinued.

Managed Care Rate Increases. The budget provides rate increases to two Medi-Cal managed care plans-Cal Optima in Orange County and the San Diego Community Health Group-to improve their financial stability. Legislative augmentations to increase rates for two additional plans were vetoed by the Governor. These increases would have gone to the Alameda Alliance for Health and the Partnership Health Plan, which now operates in Solano, Napa, and Yolo Counties.

California Medical Assistance Commission